You might also like

- Enron Case StudyDocument5 pagesEnron Case StudyIris Grace Culata0% (1)

- Enron Scandal PresentationDocument11 pagesEnron Scandal PresentationYujia JinNo ratings yet

- EnronDocument34 pagesEnronNikhil RajNo ratings yet

- Sythesis 8Document7 pagesSythesis 8Jhonerl YbañezNo ratings yet

- Group 2 EnronDocument27 pagesGroup 2 EnronWillowNo ratings yet

- Audit CaseDocument30 pagesAudit CaseAnnisa Kurnia100% (1)

- Enron Scandal: The Fall of A Wall Street Darling: "America's Most Innovative Company"Document19 pagesEnron Scandal: The Fall of A Wall Street Darling: "America's Most Innovative Company"Jamielyn Dy DimaanoNo ratings yet

- Enron Case StudyDocument7 pagesEnron Case Studynaila khanNo ratings yet

- Enron Collaspe Case StudyDocument5 pagesEnron Collaspe Case StudyKai Yin100% (1)

- Group 3 Midterm Case Studies EnronDocument14 pagesGroup 3 Midterm Case Studies EnronWiln Jinelyn NovecioNo ratings yet

- EnronDocument26 pagesEnronAnoop KularNo ratings yet

- Enron Case StudyDocument3 pagesEnron Case StudyDavid Wijaya100% (1)

- The Fall of EnronDocument3 pagesThe Fall of Enrondonjony7No ratings yet

- EnronDocument6 pagesEnronfredeksdiiNo ratings yet

- ENRON Case StudyDocument8 pagesENRON Case StudyHARSHA B.N63% (8)

- The Enron ScandalDocument14 pagesThe Enron ScandalAnup MohapatraNo ratings yet

- Case Study: The Rise and Fall of EnronDocument4 pagesCase Study: The Rise and Fall of EnronAndrew HernandezNo ratings yet

- Enron ScandalDocument9 pagesEnron ScandalRohith MohanNo ratings yet

- Enron Reaction PaperDocument3 pagesEnron Reaction PaperJohn JasperNo ratings yet

- Enron Scandal BackgroundDocument4 pagesEnron Scandal Backgroundeveell100% (3)

- Enron Case StudyDocument3 pagesEnron Case StudycharleejaiNo ratings yet

- Enron ScandalDocument24 pagesEnron Scandalmano102100% (1)

- Case Study Enron Questionable Accounting Leads To CollapseDocument7 pagesCase Study Enron Questionable Accounting Leads To CollapseAvlean TorralbaNo ratings yet

- The Enron ScandalDocument20 pagesThe Enron ScandalQueenie Gallardo AngelesNo ratings yet

- Compilation of Accounting ScandalsDocument7 pagesCompilation of Accounting ScandalsYelyah HipolitoNo ratings yet

- Enron Case Study QuestionsDocument6 pagesEnron Case Study QuestionsJiageng LiuNo ratings yet

- ENRONDocument24 pagesENRONanju_jangidNo ratings yet

- Enron and WorldCom ScandalDocument5 pagesEnron and WorldCom ScandalMarc Eric RedondoNo ratings yet

- Case Study of EnronDocument16 pagesCase Study of Enronapi-619489263No ratings yet

- Corp. Gov. Lessons From Enron PDFDocument6 pagesCorp. Gov. Lessons From Enron PDFRatnesh SinghNo ratings yet

- Enron Fraud Case SummaryDocument5 pagesEnron Fraud Case Summaryamara cheema100% (3)

- The Case Analysis of The Scandal of EnronDocument4 pagesThe Case Analysis of The Scandal of EnronKhadija AkterNo ratings yet

- Enron Corporation: A Case StudyDocument18 pagesEnron Corporation: A Case StudylaleenmehtaNo ratings yet

- Arthur AndersenDocument9 pagesArthur AndersenSheraz HasanNo ratings yet

- The Enron Scandal - AssignmentDocument12 pagesThe Enron Scandal - AssignmentArasen அரசன் பழனியாண்டி100% (1)

- Question 1: How Did The Corporate Culture at Enron Contribute To Its Bankruptcy?Document8 pagesQuestion 1: How Did The Corporate Culture at Enron Contribute To Its Bankruptcy?maraki93No ratings yet

- Enron PaperDocument24 pagesEnron PaperJoshy_29100% (1)

- An ENRON Scandal SummaryDocument2 pagesAn ENRON Scandal SummarySafwan Munda75% (4)

- Enron Case StudyDocument5 pagesEnron Case StudyIris Grace Culata100% (1)

- 1Document3 pages1Mehadi100% (4)

- About Enron Scandal 2Document6 pagesAbout Enron Scandal 2Mark AguinaldoNo ratings yet

- Assignment EnronDocument4 pagesAssignment EnronMuhammad Umer100% (2)

- Enron CaseDocument5 pagesEnron CasemurielNo ratings yet

- Enron ScandalDocument16 pagesEnron ScandalboldfaceaxisNo ratings yet

- Case 13 - 6 Quality Furniture CompanyDocument4 pagesCase 13 - 6 Quality Furniture CompanyGina Davidson67% (3)

- Case 1.1 Enron CorporationDocument13 pagesCase 1.1 Enron CorporationAlexa RodriguezNo ratings yet

- CASE 1 Enron IndependenceDocument3 pagesCASE 1 Enron IndependenceFatiha Yusof0% (2)

- Enron Company ScandalDocument16 pagesEnron Company ScandalAbaynesh ShiferawNo ratings yet

- Enrone Case Study FindingsDocument6 pagesEnrone Case Study Findingszubair attariNo ratings yet

- Case Study (Ethical Issues)Document10 pagesCase Study (Ethical Issues)Abelle Rina Villacencio GallardoNo ratings yet

- Enron Case StudyDocument23 pagesEnron Case StudyJayesh Dubey100% (1)

- Case 4.1 EnronDocument11 pagesCase 4.1 EnronCrystalNo ratings yet

- Enron - Reaction Paper # 2Document3 pagesEnron - Reaction Paper # 2delo8563% (8)

- Arthur Andersen CaseDocument10 pagesArthur Andersen CaseHarsha ShivannaNo ratings yet

- Enron CorporationDocument8 pagesEnron CorporationNadine Clare FloresNo ratings yet

- Enron ScandalDocument7 pagesEnron ScandalMirdual JhaNo ratings yet

- Enron Scandal - 2001Document14 pagesEnron Scandal - 2001DISHA SHAHNo ratings yet

- Enron CompanyDocument3 pagesEnron Companyjayvee OrfanoNo ratings yet

- What Was EnronDocument8 pagesWhat Was EnronJenny May GodallaNo ratings yet

- Scandal: Created By: Mufassil HaqueDocument15 pagesScandal: Created By: Mufassil HaqueMufassil HaqueNo ratings yet

- FMDocument4 pagesFMafeeraNo ratings yet

- Iran Nuclear Crisis in 300 WordsDocument4 pagesIran Nuclear Crisis in 300 WordsafeeraNo ratings yet

- SyllabusDocument3 pagesSyllabusafeeraNo ratings yet

- Auditing Pak MCQSDocument27 pagesAuditing Pak MCQSAHADNo ratings yet

- Survey Instrument PDFDocument3 pagesSurvey Instrument PDFDigonto ChowdhuryNo ratings yet

- Government Owned Firms in PakistanDocument2 pagesGovernment Owned Firms in PakistanafeeraNo ratings yet

- Ciit Laptop Merit List 2015 PDFDocument184 pagesCiit Laptop Merit List 2015 PDFafeeraNo ratings yet

- English P&C 11 Subjective 2017Document2 pagesEnglish P&C 11 Subjective 2017ImranRazaBozdarNo ratings yet

- Maths McqsDocument10 pagesMaths McqsafeeraNo ratings yet

- Scholarship Form Ahmed PDFDocument1 pageScholarship Form Ahmed PDFafeeraNo ratings yet

- Battles of Islam MCQS PDFDocument2 pagesBattles of Islam MCQS PDFafeeraNo ratings yet

- Quiz 3Document131 pagesQuiz 3afeeraNo ratings yet

- PRESENTATIONDocument18 pagesPRESENTATIONafeeraNo ratings yet

- Leadership 8 Theories PDFDocument2 pagesLeadership 8 Theories PDFVi JayNo ratings yet

- Intermediate Accounting 2008 SolutionDocument6 pagesIntermediate Accounting 2008 Solutionchin leaNo ratings yet

- Philippine Trust Company. FinalDocument3 pagesPhilippine Trust Company. FinalmaxregerNo ratings yet

- Instant Download Ebook PDF Fundamentals of Financial Accounting 4th Canadian Edition by Fred Phillips PDF ScribdDocument41 pagesInstant Download Ebook PDF Fundamentals of Financial Accounting 4th Canadian Edition by Fred Phillips PDF Scribdfrances.conley899100% (41)

- Financial Accounting: Tools For Business Decision Making: Chapter OutlineDocument218 pagesFinancial Accounting: Tools For Business Decision Making: Chapter Outline20073201 Nguyễn Thị Ngọc LanNo ratings yet

- Introduction To Accounting (FABM 1)Document15 pagesIntroduction To Accounting (FABM 1)Jill Alexandra Faye FerrerNo ratings yet

- Project On Working Capital (OPTCL)Document66 pagesProject On Working Capital (OPTCL)Prateek Anand33% (3)

- The Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyDocument5 pagesThe Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyJel SanNo ratings yet

- Central Depository Company OF Pakistan Limited: An OverviewDocument22 pagesCentral Depository Company OF Pakistan Limited: An OverviewFa De-qNo ratings yet

- Sino-Environment Technology Group Limited: Board Advisory To ShareholdersDocument2 pagesSino-Environment Technology Group Limited: Board Advisory To ShareholderslaksacktNo ratings yet

- 9.3 Debt InvestmentsDocument7 pages9.3 Debt InvestmentsJorufel PapasinNo ratings yet

- P6-Capital Taxes - IHT & CGTDocument9 pagesP6-Capital Taxes - IHT & CGTAnonymous rePT5rCrNo ratings yet

- Principal Notification Letter For E-CashDocument2 pagesPrincipal Notification Letter For E-CashAizat HermanNo ratings yet

- PDF Abm 11 Famb1 q1 w4 Mod5 DDDocument18 pagesPDF Abm 11 Famb1 q1 w4 Mod5 DDMargie Sorquiano Abad QuitonNo ratings yet

- 1st Exam Theory PpeDocument4 pages1st Exam Theory PpeRonna Mae ColminasNo ratings yet

- Book Keeping AccountancyDocument8 pagesBook Keeping AccountancyNarra JanardhanNo ratings yet

- ResearchDocument4 pagesResearchIv YuhanNo ratings yet

- Gambit Corporation Purchased A New Plant Asset On April 1Document1 pageGambit Corporation Purchased A New Plant Asset On April 1Freelance WorkerNo ratings yet

- The Financial Reporting Council: A Policy Review: DR Javed Siddiqui Associate Professor of AccountingDocument37 pagesThe Financial Reporting Council: A Policy Review: DR Javed Siddiqui Associate Professor of AccountingDipto Kumar BiswasNo ratings yet

- Tugas Ke 5 Ade Hidayat Kelas 1a MMDocument4 pagesTugas Ke 5 Ade Hidayat Kelas 1a MMadeNo ratings yet

- Investment BankingDocument24 pagesInvestment BankingLakshmiNo ratings yet

- Cost Accountancy: Bba - Ii Semester - IiiDocument19 pagesCost Accountancy: Bba - Ii Semester - IiiNishikant RayanadeNo ratings yet

- Credit CreationDocument7 pagesCredit CreationwubeNo ratings yet

- ABM 11 Fundamentals-Of-ABM1 q3 CLAS4 Statement-Of-Financial-Position v1Document22 pagesABM 11 Fundamentals-Of-ABM1 q3 CLAS4 Statement-Of-Financial-Position v1Kim Yessamin Madarcos100% (1)

- MSQ-10 - Cost of CapitalDocument11 pagesMSQ-10 - Cost of CapitalMIKHAELALOUISSE MARIANONo ratings yet

- PPE QuestionsDocument9 pagesPPE QuestionsMel BayhiNo ratings yet

- Questions On Preparation of Financial Statements 1-4Document4 pagesQuestions On Preparation of Financial Statements 1-4LaoneNo ratings yet

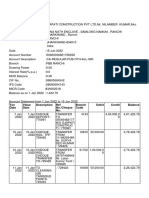

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument14 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceRishav AnandNo ratings yet

- Income Tax Payment Challan: PSID #: 42730325Document1 pageIncome Tax Payment Challan: PSID #: 42730325Muhammad Qaisar LatifNo ratings yet

- Securities and Exchange Commission: Department of Trade and Industry SEC Bldg. EDSA, Greenhills, Mandaluyong CityDocument3 pagesSecurities and Exchange Commission: Department of Trade and Industry SEC Bldg. EDSA, Greenhills, Mandaluyong CityJakko MalutaoNo ratings yet

- CA Notes Sale of Goods On Approval or Return Basis PDFDocument14 pagesCA Notes Sale of Goods On Approval or Return Basis PDFBijay Aryan Dhakal100% (1)