You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Will Global Warming Wipe Out Tibet's Glaciers?Document3 pagesWill Global Warming Wipe Out Tibet's Glaciers?Cha-am JamalNo ratings yet

- Deep Hot Biosphere - DR Thomas Gold-PNASDocument5 pagesDeep Hot Biosphere - DR Thomas Gold-PNASzaroia100% (1)

- Corruption in State Owned UtilitiesDocument8 pagesCorruption in State Owned UtilitiesCha-am JamalNo ratings yet

- The Risk Return Structure of The Credit Card IndustryDocument17 pagesThe Risk Return Structure of The Credit Card IndustryCha-am JamalNo ratings yet

- History of The Global Warming Scare Chapter 5: 2000-2005Document5 pagesHistory of The Global Warming Scare Chapter 5: 2000-2005Cha-am JamalNo ratings yet

- The Arbitrage Pricing Model in FinanceDocument5 pagesThe Arbitrage Pricing Model in FinanceCha-am JamalNo ratings yet

- Employment Public Aid RenewableDocument53 pagesEmployment Public Aid RenewablethierrydebelsNo ratings yet

- Gap Management 101Document6 pagesGap Management 101Cha-am JamalNo ratings yet

- Corruption Case StudyDocument7 pagesCorruption Case StudyCha-am JamalNo ratings yet

- History of The Global Warming Scare: Chapter 4: 1995 - 2000Document6 pagesHistory of The Global Warming Scare: Chapter 4: 1995 - 2000Cha-am JamalNo ratings yet

- Portfolio Theory Lecture NotesDocument2 pagesPortfolio Theory Lecture NotesCha-am Jamal100% (1)

- The Montreal ProtocolDocument2 pagesThe Montreal ProtocolCha-am JamalNo ratings yet

- Enterprise Reform in ChinaDocument3 pagesEnterprise Reform in ChinaCha-am JamalNo ratings yet

- Dupont AnalysisDocument4 pagesDupont AnalysisCha-am JamalNo ratings yet

- Database NormalizationDocument2 pagesDatabase NormalizationCha-am JamalNo ratings yet

- History of The Global Warming Scare. Chapter 2, 1985-1990Document3 pagesHistory of The Global Warming Scare. Chapter 2, 1985-1990Cha-am JamalNo ratings yet

- History of The Global Warming Scare: Chapter 3: 1990-1995Document5 pagesHistory of The Global Warming Scare: Chapter 3: 1990-1995Cha-am Jamal100% (1)

- On The Alleged Fractal Nature of MarketsDocument5 pagesOn The Alleged Fractal Nature of MarketsCha-am JamalNo ratings yet

- Stock Exchange AutomationDocument2 pagesStock Exchange AutomationCha-am JamalNo ratings yet

- Institutional Reforms For Capital Markets in ChinaDocument9 pagesInstitutional Reforms For Capital Markets in ChinaCha-am JamalNo ratings yet

- A Method For Constructing Likert ScalesDocument12 pagesA Method For Constructing Likert ScalesCha-am JamalNo ratings yet

- The Kyoto ProtocolDocument2 pagesThe Kyoto ProtocolCha-am Jamal100% (1)

- A Framework For MIS Effectiveness ResearchDocument8 pagesA Framework For MIS Effectiveness ResearchCha-am JamalNo ratings yet

- History of The Global Warming Scare: Chapter 1: 1980 - 1985Document3 pagesHistory of The Global Warming Scare: Chapter 1: 1980 - 1985Cha-am JamalNo ratings yet

- The Re-Unification of IndiaDocument2 pagesThe Re-Unification of IndiaCha-am JamalNo ratings yet

- Village Life in BangladeshDocument3 pagesVillage Life in BangladeshCha-am Jamal0% (1)

- Moderate MuslimsDocument1 pageModerate MuslimsCha-am JamalNo ratings yet

- Ozone Hole News Archive: 1987 To 2005Document3 pagesOzone Hole News Archive: 1987 To 2005Cha-am JamalNo ratings yet

- The International Aid BusinessDocument1 pageThe International Aid BusinessCha-am JamalNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bucksbaum SuitDocument28 pagesBucksbaum SuitChicago Tribune100% (1)

- For Mba Student Summer Assignment IfsDocument17 pagesFor Mba Student Summer Assignment IfsRajan ShrivastavaNo ratings yet

- CIMB - DaybreakDocument10 pagesCIMB - DaybreakThomas Lau100% (3)

- Contoh Print Out Neraca Saldo Jan-Feb 2018 Accurate 5Document34 pagesContoh Print Out Neraca Saldo Jan-Feb 2018 Accurate 5Mohammad Fauzi Kushardia NovanNo ratings yet

- Sharpe's Ratio - Portfolio EvaluationDocument12 pagesSharpe's Ratio - Portfolio EvaluationVaidyanathan RavichandranNo ratings yet

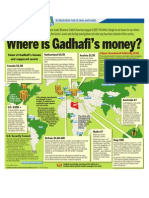

- Where Is Gadhafi's Money?Document1 pageWhere Is Gadhafi's Money?The London Free Press100% (2)

- Kavry Project MBA 2019Document87 pagesKavry Project MBA 2019Catherine Maria0% (1)

- Economics Project AbstractDocument3 pagesEconomics Project AbstractRahul KumarNo ratings yet

- Redback MiningDocument23 pagesRedback MiningOuedraogo AzouNo ratings yet

- Ugc Net EconomicsDocument17 pagesUgc Net EconomicsSachin SahooNo ratings yet

- Baupost GroupDocument7 pagesBaupost GroupValueWalk0% (1)

- Pe 3061 4Document1 pagePe 3061 4ALONSO SANCHEZ CARLOSNo ratings yet

- PEMI PSEiDocument1 pagePEMI PSEiVictor RamirezNo ratings yet

- Ias33 PDFDocument26 pagesIas33 PDFJorreyGarciaOplas100% (1)

- Financial Management MCQDocument31 pagesFinancial Management MCQR.ARULNo ratings yet

- Sample Financial Plan Arthayantra PDFDocument15 pagesSample Financial Plan Arthayantra PDFVamsi Pavan Kumar SankaNo ratings yet

- Alberta International Offices ReviewDocument20 pagesAlberta International Offices ReviewEdmonton SunNo ratings yet

- Batus - Price Will Tell (Entry)Document187 pagesBatus - Price Will Tell (Entry)Tengku DinNo ratings yet

- Candle Stick PatternDocument15 pagesCandle Stick Patterndisha_gupta_16No ratings yet

- Fera ActDocument28 pagesFera Actjuhi jainNo ratings yet

- ACY4001 Advanced Accounting 1 - Individual Assignment 2 - Ch17Document2 pagesACY4001 Advanced Accounting 1 - Individual Assignment 2 - Ch17Morris LoNo ratings yet

- Written Report in Ucsp: Title: Economic InstitutionsDocument10 pagesWritten Report in Ucsp: Title: Economic InstitutionsLizley CordovaNo ratings yet

- NGAS 2019 eBOOKDocument128 pagesNGAS 2019 eBOOKGabinu AngNo ratings yet

- Adjudication Order in Respect of Gulshan V Chopra in The Matter of M/s Niraj Cement Structurals LimitedDocument20 pagesAdjudication Order in Respect of Gulshan V Chopra in The Matter of M/s Niraj Cement Structurals LimitedShyam SunderNo ratings yet

- JPM Covered Bond Handbook 2010Document252 pagesJPM Covered Bond Handbook 2010Audrey LimNo ratings yet

- BCG MatrixDocument2 pagesBCG Matrixpallav86No ratings yet

- Tutorial Answers FDIDocument6 pagesTutorial Answers FDISong YeeNo ratings yet

- Prospectus BedmuthaIndustriesDocument380 pagesProspectus BedmuthaIndustriesMurali KrishnaNo ratings yet

- Functions of Stock ExchangeDocument2 pagesFunctions of Stock ExchangeGokulKarwaNo ratings yet

- Definedge Diwali NewsletterDocument10 pagesDefinedge Diwali NewsletterSubbarayudu PasupulaNo ratings yet