You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Assignment 1 - Financial Accounting 1A Introduction To Accounting Financial Accounting 1Document4 pagesAssignment 1 - Financial Accounting 1A Introduction To Accounting Financial Accounting 1aldrid100% (1)

- ACCT233 Midterm Exam Multichoice QuestionsDocument7 pagesACCT233 Midterm Exam Multichoice QuestionsDominic Robinson0% (1)

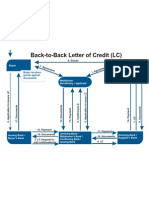

- Back To Back LCDocument1 pageBack To Back LCJayant Nair0% (1)

- Russia Enterprise Survey - World Bank - 2012Document15 pagesRussia Enterprise Survey - World Bank - 2012The Russia MonitorNo ratings yet

- 2012 Year in Review - Russia-Eurasia SectionDocument18 pages2012 Year in Review - Russia-Eurasia SectionThe Russia MonitorNo ratings yet

- US-Russia Cooperation - Law EnforcementDocument1 pageUS-Russia Cooperation - Law EnforcementThe Russia MonitorNo ratings yet

- GLOBE Project - E. European ClusterDocument12 pagesGLOBE Project - E. European ClusterThe Russia MonitorNo ratings yet

- OECD RussiaDocument34 pagesOECD RussiacorruptioncurrentsNo ratings yet

- Magnitsky Federation Council ReportDocument19 pagesMagnitsky Federation Council ReportThe Russia Monitor100% (2)

- 2012 - GRECO Theme I Eval On IncriminationsDocument30 pages2012 - GRECO Theme I Eval On IncriminationsThe Russia MonitorNo ratings yet

- SSL Amendments - Changes 1st To 2nd ReadingDocument9 pagesSSL Amendments - Changes 1st To 2nd ReadingThe Russia MonitorNo ratings yet

- Link Between Bureaucracy and CorruptionDocument46 pagesLink Between Bureaucracy and CorruptionThe Russia MonitorNo ratings yet

- 2012 - Russia Economic Report - WBDocument43 pages2012 - Russia Economic Report - WBThe Russia MonitorNo ratings yet

- Usa v. Kaushansky - IndictmentDocument51 pagesUsa v. Kaushansky - IndictmentThe Russia MonitorNo ratings yet

- Usa v. Kaushansky - OpinionDocument27 pagesUsa v. Kaushansky - OpinionThe Russia MonitorNo ratings yet

- 2012 - Forecast For Russia 2012-14 - BOFITDocument6 pages2012 - Forecast For Russia 2012-14 - BOFITThe Russia MonitorNo ratings yet

- 2011 - Russia Competitiveness Report - WEFDocument237 pages2011 - Russia Competitiveness Report - WEFThe Russia MonitorNo ratings yet

- SWGI Growth Fund - 2009 Annual ReportDocument51 pagesSWGI Growth Fund - 2009 Annual ReportThe Russia MonitorNo ratings yet

- GRECO - Russia Compliance Report - Dec. 2010Document30 pagesGRECO - Russia Compliance Report - Dec. 2010The Russia MonitorNo ratings yet

- GRECO - Russia Compliance Report - Dec. 2008Document79 pagesGRECO - Russia Compliance Report - Dec. 2008The Russia MonitorNo ratings yet

- Unwritten - Rules - How Russia Really WorksDocument52 pagesUnwritten - Rules - How Russia Really WorksThe Russia MonitorNo ratings yet

- Yandex F-1 Filing With SEC - 04.28Document436 pagesYandex F-1 Filing With SEC - 04.28The Russia MonitorNo ratings yet

- 2011 - Corruption and RoL - RADDocument17 pages2011 - Corruption and RoL - RADThe Russia MonitorNo ratings yet

- Rizopoulos Sergakis - Corruption and Ecoonomic NationalismDocument19 pagesRizopoulos Sergakis - Corruption and Ecoonomic NationalismThe Russia MonitorNo ratings yet

- Yakovlev - Black Cash Tax Evasion in Russia - 1999Document44 pagesYakovlev - Black Cash Tax Evasion in Russia - 1999The Russia MonitorNo ratings yet

- Ledeneva - Informal Practices in Changing SocietiesDocument31 pagesLedeneva - Informal Practices in Changing SocietiesThe Russia Monitor100% (1)

- Procurement Tool Guidance DoccumentDocument2 pagesProcurement Tool Guidance DoccumentThe Russia MonitorNo ratings yet

- Oecd - Public Procurement Reducing CorruptionDocument501 pagesOecd - Public Procurement Reducing CorruptionThe Russia MonitorNo ratings yet

- OECD Fighting Bid RiggingDocument18 pagesOECD Fighting Bid RiggingAlberto LucioNo ratings yet

- Strategic Protectionism? National Security and Foreign Investment in The Russian FederationDocument38 pagesStrategic Protectionism? National Security and Foreign Investment in The Russian FederationThe Russia MonitorNo ratings yet

- Procurement Tool Risk Assessment DocumentDocument4 pagesProcurement Tool Risk Assessment DocumentThe Russia MonitorNo ratings yet

- Procurement Tool Procedure DocumentDocument5 pagesProcurement Tool Procedure DocumentThe Russia MonitorNo ratings yet

- OECD - Bribery in Public ProcurementDocument107 pagesOECD - Bribery in Public ProcurementThe Russia MonitorNo ratings yet

- Manual XiiDocument868 pagesManual XiiyogeshdagaurNo ratings yet

- Volume XV - Issue 3 - SEPTEMBER 2019: I. Internal Working Group To Review The Liquidity Management FrameworkDocument4 pagesVolume XV - Issue 3 - SEPTEMBER 2019: I. Internal Working Group To Review The Liquidity Management FrameworkAnonymous Ax5bwAHvNo ratings yet

- Internship Report On Customer Satisfaction and General Operations of Rupali BankDocument43 pagesInternship Report On Customer Satisfaction and General Operations of Rupali BankjaiontyNo ratings yet

- AEF3 - Unit 2ADocument7 pagesAEF3 - Unit 2Asouzalimagustavo2005No ratings yet

- Analyzing The Consumer Level of Satisfaction of Al-Arafah Islami Bank Limited. (AIBL)Document52 pagesAnalyzing The Consumer Level of Satisfaction of Al-Arafah Islami Bank Limited. (AIBL)Tariqul IslamNo ratings yet

- Busifin Final Period 2021 2022Document46 pagesBusifin Final Period 2021 2022Glenn Mark NochefrancaNo ratings yet

- Case Digest - IntroductionDocument10 pagesCase Digest - IntroductionAnonymous b4ycWuoIcNo ratings yet

- TODAY at BULLET Chapter 2 TVM ContinuedDocument8 pagesTODAY at BULLET Chapter 2 TVM ContinuedThùy LêNo ratings yet

- Examiners' Commentaries 2016: FN1024 Principles of Banking and FinanceDocument25 pagesExaminers' Commentaries 2016: FN1024 Principles of Banking and FinancekashmiraNo ratings yet

- Confidential Background Screening Report : Orderid - 1806237104Document9 pagesConfidential Background Screening Report : Orderid - 1806237104Nitish KumarNo ratings yet

- 10000003617Document231 pages10000003617Chapter 11 DocketsNo ratings yet

- Affidavit of Assets, Income and ExpenditureDocument28 pagesAffidavit of Assets, Income and ExpenditureAnubhav KathuriaNo ratings yet

- Moody's Methodology Re CTL TransactionsDocument14 pagesMoody's Methodology Re CTL TransactionsChris BamfordNo ratings yet

- General Ordinary AnnuitiesDocument3 pagesGeneral Ordinary Annuitiesstudent.devyankgosainNo ratings yet

- Ethiopia SMEs Close Market HelloopayDocument10 pagesEthiopia SMEs Close Market Helloopayetebark h/michaleNo ratings yet

- Bulk Upload Template v3.1Document38 pagesBulk Upload Template v3.1satishNo ratings yet

- TAFE Ag Nit OVRDocument73 pagesTAFE Ag Nit OVR2562923No ratings yet

- Anshul Kirti: 839 N Marshall STDocument1 pageAnshul Kirti: 839 N Marshall STAnshul KirtiNo ratings yet

- 186 2020 Codification Valuation and Registration of Movable Properties As Collateral For Credit DirectiveDocument22 pages186 2020 Codification Valuation and Registration of Movable Properties As Collateral For Credit DirectiveAfework AtnafsegedNo ratings yet

- DOCUNUV2030 Lav3456Document75 pagesDOCUNUV2030 Lav3456Eloy BornazNo ratings yet

- ALM - SBI - PPT FinalDocument54 pagesALM - SBI - PPT FinalaanchaliyaNo ratings yet

- SOF DL en Brand V15 - tcm41 180545 PDFDocument11 pagesSOF DL en Brand V15 - tcm41 180545 PDFAnkur GargNo ratings yet

- Homework #1: Nguyen Xuan Thanh Strategy division-TCBDocument2 pagesHomework #1: Nguyen Xuan Thanh Strategy division-TCBThanh NguyenNo ratings yet

- Gin BilogDocument14 pagesGin BilogHans Pierre AlfonsoNo ratings yet

- CommoditiesDemystified Section C en PDFDocument16 pagesCommoditiesDemystified Section C en PDFkitty2604No ratings yet

- Ifr 1510Document76 pagesIfr 1510Alekey HaselNo ratings yet

- Types of SwapsDocument25 pagesTypes of SwapsBinal JasaniNo ratings yet