You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MarketIntegration 3Document11 pagesMarketIntegration 3Franz Althea BasabeNo ratings yet

- CPG Analytics - MarketelligentDocument2 pagesCPG Analytics - MarketelligentMarketelligent100% (3)

- How To Plan India Entry Strategy PDFDocument6 pagesHow To Plan India Entry Strategy PDFSHIVAM KUMAR SINGHNo ratings yet

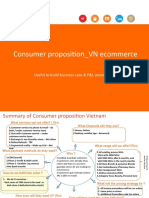

- Consumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsDocument3 pagesConsumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsvuquyhaiNo ratings yet

- Kotler Mktman 11ce Ch04Document34 pagesKotler Mktman 11ce Ch04Murtaza MoizNo ratings yet

- 1201 NguyenThuyTrang 2121007554Document37 pages1201 NguyenThuyTrang 2121007554Nguyễn Thùy TrangNo ratings yet

- Citi 201205Document10 pagesCiti 201205sinnlosNo ratings yet

- AccountStatement01-10-2022 To 24-02-2023Document27 pagesAccountStatement01-10-2022 To 24-02-2023Amit KumarNo ratings yet

- Material AnalysisDocument7 pagesMaterial AnalysisNiña Grace Rita MangleNo ratings yet

- Methodology To Approve Maximum Prices For Piped GasDocument42 pagesMethodology To Approve Maximum Prices For Piped GassizwehNo ratings yet

- Payment 380 490413BDocument2 pagesPayment 380 490413BJohanny SantosNo ratings yet

- Strategies For Mature and Declining MarketsDocument31 pagesStrategies For Mature and Declining MarketskarolinNo ratings yet

- Financial Analysis of Power SectorDocument19 pagesFinancial Analysis of Power SectorPKNo ratings yet

- Motohashi (2015) - Global Business Strategy - Chapter 9 - Marketing Theory in Global Business Context (18p)Document18 pagesMotohashi (2015) - Global Business Strategy - Chapter 9 - Marketing Theory in Global Business Context (18p)TaynaNo ratings yet

- 5th Term - Operations ManagementDocument58 pages5th Term - Operations ManagementShreedharNo ratings yet

- Recommend Market Entry Strategy For Wildgood Into The Mexico MarketDocument25 pagesRecommend Market Entry Strategy For Wildgood Into The Mexico MarketThiên Phong Trần100% (1)

- Research 2002Document67 pagesResearch 2002West AfricaNo ratings yet

- Nithin ProjectDocument33 pagesNithin ProjectMuhammed Althaf VK0% (1)

- Unit 8 PromotionDocument34 pagesUnit 8 PromotionBHAKT Raj BhagatNo ratings yet

- Mangliya Plant, Indore (M.P.) : BY: Gloria Dsouza Mba MDocument29 pagesMangliya Plant, Indore (M.P.) : BY: Gloria Dsouza Mba MGloria DsouzaNo ratings yet

- MODULE 4 Group 6Document17 pagesMODULE 4 Group 6Denisse Nicole SerutNo ratings yet

- Strategic Retail Management Text and International Cases PDFDocument469 pagesStrategic Retail Management Text and International Cases PDFthanhvan34No ratings yet

- Experiments Reading List With Abstracts - April 6 2020Document63 pagesExperiments Reading List With Abstracts - April 6 2020jshen5No ratings yet

- Submitted To: Shailee Parmar: Nikita Punera Student Id:Iuu19Bba061Document15 pagesSubmitted To: Shailee Parmar: Nikita Punera Student Id:Iuu19Bba061nikitaNo ratings yet

- Market Timing Via Monthly and Holiday PatternsDocument10 pagesMarket Timing Via Monthly and Holiday PatternsSteven KimNo ratings yet

- Anagene - Final Case AssignmentDocument19 pagesAnagene - Final Case AssignmentSantiago Fernandez Moreno100% (1)

- Private LabelsDocument12 pagesPrivate LabelsSanil YadavNo ratings yet

- Business Plan: Introductory PageDocument7 pagesBusiness Plan: Introductory PageRahil AnwarmemonNo ratings yet

- Marketing Management 6e: Chapter 3: SegmentationDocument63 pagesMarketing Management 6e: Chapter 3: Segmentation11 CNo ratings yet

- EEFCDocument2 pagesEEFCmithilesh tabhaneNo ratings yet