You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fundamentals AnswerDocument12 pagesFundamentals AnswerRienalyn Dumlao Duldulao-DaligconNo ratings yet

- Capsa UnitedDocument12 pagesCapsa Unitedvenkat rajNo ratings yet

- NDA All Mcqs 2024Document4 pagesNDA All Mcqs 2024Shailesh PandeyNo ratings yet

- Substantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Document38 pagesSubstantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Mej AgaoNo ratings yet

- Signed Off Entrepreneurship12q2 Mod10 Bookkeeping v4Document75 pagesSigned Off Entrepreneurship12q2 Mod10 Bookkeeping v4Felipe BalinasNo ratings yet

- Santos Pays 80,000 For 1/2 Share of Hernandez InterestDocument9 pagesSantos Pays 80,000 For 1/2 Share of Hernandez InterestGvm Joy MagalingNo ratings yet

- Accounting Equation Chapter SummaryDocument6 pagesAccounting Equation Chapter SummaryRamainne Ronquillo100% (1)

- International School Taxation Exam GuideDocument5 pagesInternational School Taxation Exam GuideROMAR A. PIGANo ratings yet

- Capital Budgeting Exercise1Document14 pagesCapital Budgeting Exercise1rohini jha0% (1)

- Nuvoco Vistas Corporation Limited Draft Red Herring ProspectusDocument518 pagesNuvoco Vistas Corporation Limited Draft Red Herring ProspectusShree TisaiNo ratings yet

- Articles of Incorporation and By-Laws - Non Stock CorporationDocument30 pagesArticles of Incorporation and By-Laws - Non Stock CorporationneneNo ratings yet

- Financial Transaction (Evelyn Tria)Document2 pagesFinancial Transaction (Evelyn Tria)Mika CunananNo ratings yet

- Fnce 3300 HW1Document13 pagesFnce 3300 HW1Yuru LINo ratings yet

- Income statement and financial position documents solutionsDocument59 pagesIncome statement and financial position documents solutionsNam PhươngNo ratings yet

- ENTREPRENEURSHIPDocument22 pagesENTREPRENEURSHIPR ApigoNo ratings yet

- ACCT 100, Fall Semester 2020-21 Quiz 2Document48 pagesACCT 100, Fall Semester 2020-21 Quiz 2Ali Zain ParharNo ratings yet

- Chamber Challenges Minimum Corporate Income Tax, Withholding Tax RulesDocument13 pagesChamber Challenges Minimum Corporate Income Tax, Withholding Tax RulesAngelie Fei CuirNo ratings yet

- IFRS vs USGAAP DifferencesDocument7 pagesIFRS vs USGAAP DifferencesRahul AgarwalNo ratings yet

- ReillyBrown IAPM 11e PPT Ch08Document97 pagesReillyBrown IAPM 11e PPT Ch08rocky wongNo ratings yet

- MQE Cost Acctg Session 1Document78 pagesMQE Cost Acctg Session 1Frances Monique Alburo0% (1)

- BSP Circ - No. 781 RbcarDocument37 pagesBSP Circ - No. 781 RbcarKesca GutierrezNo ratings yet

- Introduction and Overview of IBCDocument3 pagesIntroduction and Overview of IBCArushi JindalNo ratings yet

- Analysis and Interpretation of Financial StatementsDocument16 pagesAnalysis and Interpretation of Financial StatementsKimberly FloresNo ratings yet

- The Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeDocument6 pagesThe Manufacturers Life Insurance Co., Plaintiff-Internal Revenue, Defendant-AppelleeJade ClementeNo ratings yet

- Cooperate Governance and Fraud Management The Role of External Auditor Public Quoted Company in NigeriaDocument81 pagesCooperate Governance and Fraud Management The Role of External Auditor Public Quoted Company in NigeriaIgbokoyi QuadriNo ratings yet

- Answers To True or False, Relating To SFP, With ExplanationsDocument3 pagesAnswers To True or False, Relating To SFP, With ExplanationsPATRICIA SANTOS100% (1)

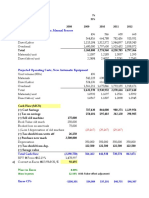

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Document4 pagesProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyNo ratings yet

- ICICI - Piramal PharmaDocument4 pagesICICI - Piramal PharmasehgalgauravNo ratings yet

- 19BACT602 - Accounting For Managers: Unit III - Introduction To Cost AccountingDocument12 pages19BACT602 - Accounting For Managers: Unit III - Introduction To Cost AccountingReetaNo ratings yet

- Revised Standard Chart of Accounts for Cooperatives (CDA MC No. 2016-06Document1 pageRevised Standard Chart of Accounts for Cooperatives (CDA MC No. 2016-06GuineaMaeEugarolf0% (1)