You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- PWC Basics of Mining Accounting UsDocument133 pagesPWC Basics of Mining Accounting Ussharanabasappa baliger100% (1)

- 7-11 Franchising Paper PROPOSAL ONLYDocument42 pages7-11 Franchising Paper PROPOSAL ONLYYara AB100% (1)

- Financial AnalysisDocument9 pagesFinancial Analysisgem paolo lagranaNo ratings yet

- LCM Grade 3 Italian WordsDocument3 pagesLCM Grade 3 Italian WordsChantal MangionNo ratings yet

- 08.10.19 Access To FinanceDocument62 pages08.10.19 Access To FinanceChantal MangionNo ratings yet

- 08.10.19 Business PlanningDocument18 pages08.10.19 Business PlanningChantal MangionNo ratings yet

- Chromatic Scale WorksheetDocument2 pagesChromatic Scale WorksheetChantal MangionNo ratings yet

- Grade 2 Theory Test: DynamicsDocument2 pagesGrade 2 Theory Test: DynamicsChantal MangionNo ratings yet

- Dynamics: Grade 1 Theory Italian Sign EnglishDocument2 pagesDynamics: Grade 1 Theory Italian Sign EnglishChantal MangionNo ratings yet

- Commercial Law For AccountantsDocument19 pagesCommercial Law For AccountantsChantal MangionNo ratings yet

- Finger Number: Game Idea From Becki LewisDocument2 pagesFinger Number: Game Idea From Becki LewisChantal MangionNo ratings yet

- Timetable-DraftDocument2 pagesTimetable-DraftChantal MangionNo ratings yet

- Management in A Dynamic EnvironmentDocument21 pagesManagement in A Dynamic EnvironmentChantal MangionNo ratings yet

- Timetable-DraftDocument2 pagesTimetable-DraftChantal MangionNo ratings yet

- The Environment - Values and ChoicesDocument2 pagesThe Environment - Values and ChoicesChantal MangionNo ratings yet

- 3.technology As A ProcessDocument3 pages3.technology As A ProcessChantal MangionNo ratings yet

- Sidney Sheldon ChecklistDocument1 pageSidney Sheldon ChecklistChantal MangionNo ratings yet

- HkfrspeDocument340 pagesHkfrspeTommy KoNo ratings yet

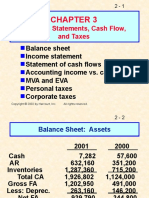

- Financial Statements, Cash Flow, and TaxesDocument40 pagesFinancial Statements, Cash Flow, and Taxessalma fitriaNo ratings yet

- Eyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsDocument5 pagesEyedropper Clinic: Accounting Equation: Current Assets Non Current AssetsSofía MargaritaNo ratings yet

- Finance Case Competition Team 8 Executive Report PDFDocument11 pagesFinance Case Competition Team 8 Executive Report PDFRyan TeichmannNo ratings yet

- Form AOC-4-11122019 - SignedDocument16 pagesForm AOC-4-11122019 - SignedNi007ckNo ratings yet

- Lecture 2 Depreciation, Accruals and CashflowDocument30 pagesLecture 2 Depreciation, Accruals and CashflowSalahuddin KhanNo ratings yet

- Financial Statements Year Ended December 31, 20X5: ABC CompanyDocument11 pagesFinancial Statements Year Ended December 31, 20X5: ABC CompanysaraNo ratings yet

- Corporate Finance Mini CaseDocument6 pagesCorporate Finance Mini CaseMashaal FNo ratings yet

- TerotechnologyDocument1 pageTerotechnologyLuciano RibeiroNo ratings yet

- Profit Center AccountingDocument55 pagesProfit Center AccountingBala RanganathNo ratings yet

- Caterpillar IndicadoresDocument24 pagesCaterpillar IndicadoresChris Fernandes De Matos BarbosaNo ratings yet

- 20 - Muhammad Greyfan SetyadiDocument15 pages20 - Muhammad Greyfan SetyadigreyfanNo ratings yet

- (Xii) 2023 Solved Sample Target Paper C.G, PST, Acc, Stats by Sir IrfanDocument30 pages(Xii) 2023 Solved Sample Target Paper C.G, PST, Acc, Stats by Sir IrfanSaira ShahaniNo ratings yet

- Inflation Accounting: Presented ByDocument24 pagesInflation Accounting: Presented ByjasminerathodNo ratings yet

- BAFM6102 - Prelim Quiz 1 - Attempt ReviewDocument4 pagesBAFM6102 - Prelim Quiz 1 - Attempt ReviewKinglaw PilandeNo ratings yet

- 1 20180905052123Document194 pages1 20180905052123Gupllo Kin'emonJrNo ratings yet

- December 2021 Financial Acocunting and Reporting UK GAAPDocument11 pagesDecember 2021 Financial Acocunting and Reporting UK GAAPChoo LeeNo ratings yet

- Ranbaxy Laboratories LTD.: Accounting For Managers ProjectDocument7 pagesRanbaxy Laboratories LTD.: Accounting For Managers ProjectAnmol SinghviNo ratings yet

- Week 6 Assignment FNCE UCWDocument1 pageWeek 6 Assignment FNCE UCWamyna abhavaniNo ratings yet

- FI AIAB JPN Create Settlement RulesDocument18 pagesFI AIAB JPN Create Settlement RulesnguyencaohuyNo ratings yet

- Commonwealth Bank Financial AnalysisDocument11 pagesCommonwealth Bank Financial AnalysisMuhammad MubeenNo ratings yet

- #1-Illustrative ProblemDocument19 pages#1-Illustrative ProblemNisharie AbanNo ratings yet

- Partnership and Piecemeal DistributionDocument46 pagesPartnership and Piecemeal DistributionPadmalochan NayakNo ratings yet

- On IFRS, US GAAP and Indian GAAPDocument64 pagesOn IFRS, US GAAP and Indian GAAPrishipath100% (1)

- Unit II Lesson 5 and 6 ADJUSTING ENTRIES and FSDocument25 pagesUnit II Lesson 5 and 6 ADJUSTING ENTRIES and FSAlezandra SantelicesNo ratings yet

- 2607y Maliyyə Hesabatı SABAH (En)Document34 pages2607y Maliyyə Hesabatı SABAH (En)leylaNo ratings yet