You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- MS Project Step by Step GuideDocument180 pagesMS Project Step by Step GuideMaryam Alqasimy50% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Transmission Tower Installation ProcessDocument50 pagesTransmission Tower Installation ProcessManoranjan Dash100% (8)

- PHD Initial Research Proposal TemplateDocument24 pagesPHD Initial Research Proposal TemplateIrina100% (2)

- 2001 EPRI International Maintenance Conference Maintaining Reliable Electric Generation PDFDocument448 pages2001 EPRI International Maintenance Conference Maintaining Reliable Electric Generation PDFEuNo ratings yet

- Standard Procedure For Hotel Sales Team Incentives PlanDocument2 pagesStandard Procedure For Hotel Sales Team Incentives PlanImee S. Yu0% (1)

- Sample HSC Business Report For Section III HSC Business Studies ExaminationDocument11 pagesSample HSC Business Report For Section III HSC Business Studies Examinationchloe100% (1)

- HRSG PBP - Vital Group ProposalDocument49 pagesHRSG PBP - Vital Group ProposalFatima AhmedNo ratings yet

- Dessler HRM12e PPT 7bDocument41 pagesDessler HRM12e PPT 7bMirul AzimiNo ratings yet

- Central Banking: I. Role of Central BankDocument14 pagesCentral Banking: I. Role of Central BankManuNo ratings yet

- Ifa Bbe 16oct2016Document2 pagesIfa Bbe 16oct2016ManuNo ratings yet

- Milestones in India's Institutionalisation of Financial ServicesDocument6 pagesMilestones in India's Institutionalisation of Financial ServicesManuNo ratings yet

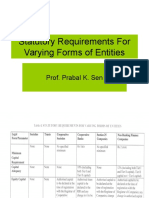

- Statutory Requirements For Varying Forms of Entities: Prof. Prabal K. SenDocument4 pagesStatutory Requirements For Varying Forms of Entities: Prof. Prabal K. SenManuNo ratings yet

- Pertmaster Project Risk - 2 Day Session: CourselevelDocument1 pagePertmaster Project Risk - 2 Day Session: CourselevelManuNo ratings yet

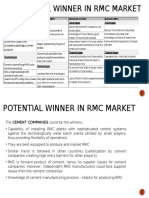

- Potential Winner in RMC MarketDocument2 pagesPotential Winner in RMC MarketManuNo ratings yet

- How To Use As Management Tool ?: AsanaDocument12 pagesHow To Use As Management Tool ?: AsanaSabin LalNo ratings yet

- DC Setup PDFDocument3 pagesDC Setup PDFManuNo ratings yet

- Checklist For EnrolmentDocument1 pageChecklist For EnrolmentManuNo ratings yet

- The Horizontal Corporation: Flattening The OrganizationDocument2 pagesThe Horizontal Corporation: Flattening The OrganizationManuNo ratings yet

- Kabaddi Case Study - StarInsipire2015Document8 pagesKabaddi Case Study - StarInsipire2015abishakekoulNo ratings yet

- BPCL FaqDocument3 pagesBPCL FaqManuNo ratings yet

- BHEL RecruitmentDocument9 pagesBHEL RecruitmentDasika SunderNo ratings yet

- Literature Review of Financial Reporting EnvironmentDocument48 pagesLiterature Review of Financial Reporting Environmentmert0723No ratings yet

- Management Process and Organizational Behaviour (MPOB) - Code-101 - BBA (Gen.) - Sem. IDocument131 pagesManagement Process and Organizational Behaviour (MPOB) - Code-101 - BBA (Gen.) - Sem. Isambhav jindalNo ratings yet

- Compensation Management Unit 1Document38 pagesCompensation Management Unit 1NI TE SHNo ratings yet

- Working Environment and Its Impact of On Employees Motivation (The Case of Arba Minch University)Document50 pagesWorking Environment and Its Impact of On Employees Motivation (The Case of Arba Minch University)sabit hussenNo ratings yet

- Buckley 2009Document12 pagesBuckley 2009AnnNo ratings yet

- ICM Tutorial Day 5Document4 pagesICM Tutorial Day 5Himanshu JauhariNo ratings yet

- Examining The Role of Transfer Pricing As A StrategyDocument19 pagesExamining The Role of Transfer Pricing As A StrategyNiketa JaiswalNo ratings yet

- Aligning Compensation Strategy With Business Strategy: A Case Study of A Company Within The Service IndustryDocument62 pagesAligning Compensation Strategy With Business Strategy: A Case Study of A Company Within The Service IndustryJerome Formalejo,No ratings yet

- Registration of Small Scale IndustriesDocument8 pagesRegistration of Small Scale IndustriesMohitraheja007No ratings yet

- Civil Service: Pensions and BenefitsDocument2 pagesCivil Service: Pensions and Benefitsshala blackNo ratings yet

- Management ScienceDocument93 pagesManagement ScienceDinesh ManikantaNo ratings yet

- Human Resource Management SolutionsDocument14 pagesHuman Resource Management Solutionskeerthi kNo ratings yet

- U6 - Extra Reading - PDF NoteDocument2 pagesU6 - Extra Reading - PDF Note21- Hải YếnNo ratings yet

- Case Study November 2010 Marks Plan ICAEWDocument38 pagesCase Study November 2010 Marks Plan ICAEWmanofhonourNo ratings yet

- Strategic Human Resource ManagementDocument59 pagesStrategic Human Resource ManagementFrancisquete BNo ratings yet

- Wage and Salary ManagementDocument35 pagesWage and Salary ManagementSuresh DewasiNo ratings yet

- R8323 ProceedingsDocument468 pagesR8323 ProceedingsChirdchai ChantaratNo ratings yet

- Executive Compensation, Incentives, and RiskDocument40 pagesExecutive Compensation, Incentives, and RiskElaina GravesNo ratings yet

- Chapter 10Document4 pagesChapter 10suitup666No ratings yet

- How Decoupling Creates Win-Win For Power Companies and CustomersDocument11 pagesHow Decoupling Creates Win-Win For Power Companies and CustomersClutha Mata-Au River Parkway GroupNo ratings yet

- Compensation Management StrategiesDocument139 pagesCompensation Management StrategiesBarbie BorahNo ratings yet

- Assignment 6 DTM3701Document6 pagesAssignment 6 DTM3701Phumlani MhlengiNo ratings yet

- Sop & QuestionnaireDocument2 pagesSop & Questionnairemikee franciscoNo ratings yet

- HOR Accrep 2007Document18 pagesHOR Accrep 2007Rudolf DeyinNo ratings yet

- Employee incentives and productivity at Harmo TechnologyDocument7 pagesEmployee incentives and productivity at Harmo TechnologyRhyzlyn De OcampoNo ratings yet