You might also like

- MIdland FInalDocument7 pagesMIdland FInalFarida100% (8)

- MidlandDocument9 pagesMidlandvenom_ftw100% (1)

- Marriott SolutionDocument3 pagesMarriott Solutiondlealsmes100% (1)

- Mariott Wacc Cost of Capital DivisionalDocument6 pagesMariott Wacc Cost of Capital DivisionalSuprabhat TiwariNo ratings yet

- Midland Energy Resources Inc SolutionDocument2 pagesMidland Energy Resources Inc SolutionAashna MehtaNo ratings yet

- Midland Energy Resources Cost of Capital AnalysisDocument8 pagesMidland Energy Resources Cost of Capital AnalysisAli Tariq Butt100% (2)

- Midland Energy Resources (Final)Document4 pagesMidland Energy Resources (Final)satherbd21100% (3)

- Marriott Solution FinalDocument20 pagesMarriott Solution FinalBharani Sai PrasanaNo ratings yet

- Ameritrade Case PDFDocument6 pagesAmeritrade Case PDFAnish Anish100% (1)

- MarriottDocument7 pagesMarriottHaritha PanyaramNo ratings yet

- Marriott financial strategy analysisDocument9 pagesMarriott financial strategy analysisZaim Zain100% (2)

- 01 - Midland AnalysisDocument7 pages01 - Midland AnalysisBadr Iftikhar100% (1)

- Midland Energy Case StudyDocument5 pagesMidland Energy Case Studyrun2win645100% (7)

- Traders Mag 2016JANDocument64 pagesTraders Mag 2016JANPrasanna Kalasekar100% (2)

- Midland WACCDocument2 pagesMidland WACCDeniz Minican100% (3)

- Midland Case CalculationsDocument24 pagesMidland Case CalculationsSharry_xxx60% (5)

- Midlands Case FinalDocument4 pagesMidlands Case FinalSourav Singh50% (2)

- Midland Energy A1Document30 pagesMidland Energy A1CarsonNo ratings yet

- Midland Energy Resources Case Study: FINS3625-Applied Corporate FinanceDocument11 pagesMidland Energy Resources Case Study: FINS3625-Applied Corporate FinanceCourse Hero100% (1)

- Midland Energy's Cost of Capital CalculationsDocument5 pagesMidland Energy's Cost of Capital CalculationsJessica Bill100% (3)

- Case Marriott A and Flinder ValvesDocument6 pagesCase Marriott A and Flinder ValvesGerardo FumagalNo ratings yet

- Case Study: Midland Energy Resources, IncDocument13 pagesCase Study: Midland Energy Resources, IncMikey MadRatNo ratings yet

- Midland Energy Group A5Document3 pagesMidland Energy Group A5Deepesh Moolchandani0% (1)

- Midland Energy Case StudyDocument5 pagesMidland Energy Case StudyLokesh GopalakrishnanNo ratings yet

- AmeriTrade Case StudyDocument3 pagesAmeriTrade Case StudyTracy PhanNo ratings yet

- Michael Fagan Slides RMC Asia 2015Document20 pagesMichael Fagan Slides RMC Asia 2015chuff6675No ratings yet

- Ameritrade's Cost of Capital AnalysisDocument7 pagesAmeritrade's Cost of Capital AnalysisTom Ziv100% (2)

- Facebook, Inc: The Initial Public OfferingDocument5 pagesFacebook, Inc: The Initial Public OfferingHanako Taniguchi PoncianoNo ratings yet

- AirThreads Valuation Case Study - Excel FileDocument18 pagesAirThreads Valuation Case Study - Excel FileRom Aure81% (16)

- LinearDocument6 pagesLinearjackedup211No ratings yet

- Facebook IPO Valuation AnalysisDocument13 pagesFacebook IPO Valuation AnalysisMegha BepariNo ratings yet

- AirThread G015Document6 pagesAirThread G015sahildharhakim83% (6)

- Secretarial Audit Compliance CheckDocument30 pagesSecretarial Audit Compliance CheckSiddhart GuptaNo ratings yet

- Lex Service PLC Cost of Capital AnalysisDocument8 pagesLex Service PLC Cost of Capital AnalysisAjith SudhakaranNo ratings yet

- Americanhomeproductscorporation Copy 120509004239 Phpapp02Document6 pagesAmericanhomeproductscorporation Copy 120509004239 Phpapp02Tanmay Mehta100% (1)

- DC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsDocument4 pagesDC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsTunzala ImanovaNo ratings yet

- Lex Service PLCDocument3 pagesLex Service PLCMinu RoyNo ratings yet

- Midland's Cost of Capital Calculations for DivisionsDocument8 pagesMidland's Cost of Capital Calculations for DivisionsDevansh RaiNo ratings yet

- Case 48 Sun MicrosystemsDocument25 pagesCase 48 Sun MicrosystemsChittisa Charoenpanich40% (5)

- Marriott Corporation Case SolutionDocument4 pagesMarriott Corporation Case SolutionccfieldNo ratings yet

- Lex Service PLCDocument11 pagesLex Service PLCArup Dey0% (1)

- Ocean Carries HBS Case StudyDocument4 pagesOcean Carries HBS Case StudyRatul EsrarNo ratings yet

- AirThread Valuation MethodsDocument21 pagesAirThread Valuation MethodsSon NguyenNo ratings yet

- Sealed Air Co Case Study Queestions Why Did Sealed Air Undertake A LeveragDocument9 pagesSealed Air Co Case Study Queestions Why Did Sealed Air Undertake A Leveragvichenyu100% (1)

- Marriott Case AnalysisDocument3 pagesMarriott Case AnalysisNikhil ThaparNo ratings yet

- Business Plan Bolt & Nuts - Financial AspectsDocument14 pagesBusiness Plan Bolt & Nuts - Financial AspectsgboobalanNo ratings yet

- Midland FinalDocument8 pagesMidland Finalkasboo6No ratings yet

- Example MidlandDocument5 pagesExample Midlandtdavis1234No ratings yet

- Midland Energy ResourcesDocument2 pagesMidland Energy Resourcesambreen khalidNo ratings yet

- Case 5 Midland Energy Case ProjectDocument7 pagesCase 5 Midland Energy Case ProjectCourse HeroNo ratings yet

- Midland Energy Resources FinalDocument5 pagesMidland Energy Resources FinalpradeepNo ratings yet

- Midland Energy Resources Group Project Cost of Capital AnalysisDocument6 pagesMidland Energy Resources Group Project Cost of Capital AnalysisAnshul SehgalNo ratings yet

- Midland Energy ResourcesDocument21 pagesMidland Energy ResourcesSavageNo ratings yet

- Hertz IPO CaseDocument6 pagesHertz IPO CaseHamid S. Parwani100% (1)

- Marriott Case WACC AnalysisDocument3 pagesMarriott Case WACC AnalysisNaman SharmaNo ratings yet

- R CF E NPV CF E: Historic RF On LTBDocument2 pagesR CF E NPV CF E: Historic RF On LTBBhawna Khosla100% (2)

- Midland EnergyDocument9 pagesMidland EnergyPrashant MishraNo ratings yet

- Midland Energy Resources Inc.: Andrew Picone Will Mcdermott Taylor Appel Liam JoyDocument13 pagesMidland Energy Resources Inc.: Andrew Picone Will Mcdermott Taylor Appel Liam JoymariliamonfardineNo ratings yet

- Midland Energy Cost of Capital Analysis for 3 DivisionsDocument2 pagesMidland Energy Cost of Capital Analysis for 3 Divisionsambreen khalidNo ratings yet

- Midland Energy WACC AnalysisDocument7 pagesMidland Energy WACC AnalysisYagil HadriNo ratings yet

- Midland Energy's Cost of Capital CalculationsDocument5 pagesMidland Energy's Cost of Capital CalculationsOmar ChaudhryNo ratings yet

- Capital Budgeting OverviewDocument31 pagesCapital Budgeting OverviewJomarTianesCorunoNo ratings yet

- MidlandDocument4 pagesMidlandsophieNo ratings yet

- Project Finance and Infrastructure: Case Study AnalysisDocument4 pagesProject Finance and Infrastructure: Case Study AnalysisAbhisek SarkarNo ratings yet

- PAnelDocument11 pagesPAnelkiller dramaNo ratings yet

- SDDocument1 pageSDkiller dramaNo ratings yet

- Looper Height TagsDocument1 pageLooper Height Tagskiller dramaNo ratings yet

- Combined SPSS in Excel 456Document89 pagesCombined SPSS in Excel 456killer dramaNo ratings yet

- Paper More-Excel SheetDocument133 pagesPaper More-Excel Sheetkiller dramaNo ratings yet

- Boeing 777 ADocument3 pagesBoeing 777 Akiller dramaNo ratings yet

- Key Takeaways From E&Y WebinarDocument2 pagesKey Takeaways From E&Y Webinarkiller dramaNo ratings yet

- P&G's Organizational EvolutionDocument6 pagesP&G's Organizational Evolutionkiller dramaNo ratings yet

- Syntax GG PlotDocument3 pagesSyntax GG Plotkiller dramaNo ratings yet

- Nedbank Case Study - FinalDocument2 pagesNedbank Case Study - Finalkiller dramaNo ratings yet

- Ucalgary 2013 Kano LienaDocument349 pagesUcalgary 2013 Kano Lienakiller dramaNo ratings yet

- Oep SCMP A5 Minibrochure WebDocument8 pagesOep SCMP A5 Minibrochure Webkiller dramaNo ratings yet

- Scale For EFA For Resilience ModelDocument9 pagesScale For EFA For Resilience Modelkiller dramaNo ratings yet

- Doe PracticeDocument237 pagesDoe Practicekiller dramaNo ratings yet

- Specification For - OGPCS008 (Online Grading System)Document1 pageSpecification For - OGPCS008 (Online Grading System)killer dramaNo ratings yet

- Type I and Type II Errror in ACCDocument3 pagesType I and Type II Errror in ACCkiller dramaNo ratings yet

- Sqms QueryDocument2 pagesSqms Querykiller dramaNo ratings yet

- Research Papers Ref 30th JanDocument33 pagesResearch Papers Ref 30th Jankiller dramaNo ratings yet

- Executive Summary:: Sl. No. Areas Implications Under GSTDocument2 pagesExecutive Summary:: Sl. No. Areas Implications Under GSTkiller dramaNo ratings yet

- LIC Zonal Grievance OfficersDocument1 pageLIC Zonal Grievance Officerskiller dramaNo ratings yet

- Manual For Building ANP Decision ModelsDocument84 pagesManual For Building ANP Decision Modelskiller dramaNo ratings yet

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocument6 pagesWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNo ratings yet

- PH Case Mexico BOPDocument6 pagesPH Case Mexico BOPkiller dramaNo ratings yet

- Reliance Trend Store ProjectDocument9 pagesReliance Trend Store Projectkiller dramaNo ratings yet

- Macro Note BookDocument56 pagesMacro Note Bookkiller dramaNo ratings yet

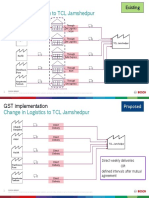

- Annexure 2 - Change in Logistics To TCL JamshedpurDocument2 pagesAnnexure 2 - Change in Logistics To TCL Jamshedpurkiller dramaNo ratings yet

- Incomplete Solutions Case StudyDocument6 pagesIncomplete Solutions Case Studykiller dramaNo ratings yet

- Randall's Advertising & Sales Promotion Case Study AnalysisDocument6 pagesRandall's Advertising & Sales Promotion Case Study Analysiskiller dramaNo ratings yet

- Mo Os Best Post GST PDFDocument60 pagesMo Os Best Post GST PDFkiller dramaNo ratings yet

- GST: A Metamorphic ReformDocument46 pagesGST: A Metamorphic Reformkiller dramaNo ratings yet

- 14 Financial Statement Analysis: Chapter SummaryDocument12 pages14 Financial Statement Analysis: Chapter SummaryGeoffrey Rainier CartagenaNo ratings yet

- Customer Satisfaction Regarding Products and Services Offered by Bank of BarodaDocument29 pagesCustomer Satisfaction Regarding Products and Services Offered by Bank of BarodaAnonymous D5g37JjpGBNo ratings yet

- Entrepreneurship MindsetDocument24 pagesEntrepreneurship MindsetChinoDanielNo ratings yet

- FDI-China AfricaDocument39 pagesFDI-China AfricaNadia BustosNo ratings yet

- Annual Report 2017 05 PDFDocument85 pagesAnnual Report 2017 05 PDFdewiNo ratings yet

- Class 11 Business Chapter 2Document14 pagesClass 11 Business Chapter 2Mahender RathorNo ratings yet

- Metlife Final ProjectDocument66 pagesMetlife Final ProjectHasan MehandiNo ratings yet

- Mclaran V CrescentDocument5 pagesMclaran V Crescentrgtan3No ratings yet

- DE3J 36 PFFpackDocument167 pagesDE3J 36 PFFpackDiana PinteaNo ratings yet

- Stores Ledger 20101012Document36 pagesStores Ledger 20101012Rafeek Shaikh0% (2)

- InvestAsian Investment Deck NewDocument14 pagesInvestAsian Investment Deck NewReidKirchenbauerNo ratings yet

- Agilent Technologies Singapore (PTE) LTD v. Integrated Silicon Technology Philippines CorporationDocument4 pagesAgilent Technologies Singapore (PTE) LTD v. Integrated Silicon Technology Philippines CorporationAnjNo ratings yet

- Financial Transactions Recordings ExplainedDocument8 pagesFinancial Transactions Recordings Explainedamir100% (3)

- National of A Country Under Whose Laws It Has Been Organized and RegisteredDocument133 pagesNational of A Country Under Whose Laws It Has Been Organized and RegisteredJeff BaronNo ratings yet

- RICS APC Requirements+Competencies 2016-17Document55 pagesRICS APC Requirements+Competencies 2016-17camelia_pirjan5776No ratings yet

- Dipifr Int 2010 Dec A PDFDocument11 pagesDipifr Int 2010 Dec A PDFPiyal HossainNo ratings yet

- PNB Sab HaiDocument6 pagesPNB Sab HaiRushadIraniNo ratings yet

- GulfDocument17 pagesGulfmastermind_2848154No ratings yet

- Pestel Analysis of Retail BankingDocument2 pagesPestel Analysis of Retail BankingShiv Shankar Chaudhary67% (3)

- Tax Bulletin by SGV As of Oct 2014Document18 pagesTax Bulletin by SGV As of Oct 2014adobopinikpikanNo ratings yet

- Financial Sector Master Plan Malaysia 2001Document12 pagesFinancial Sector Master Plan Malaysia 2001Junhuey ShanNo ratings yet

- PPCDocument21 pagesPPCJournalist ludhianaNo ratings yet

- Chapter 4 Investment Appraisal Methods 2Document62 pagesChapter 4 Investment Appraisal Methods 2JesterdanceNo ratings yet

- Jed S Rakoff Financial Disclosure Report For 2009Document7 pagesJed S Rakoff Financial Disclosure Report For 2009Judicial Watch, Inc.No ratings yet

- Return On Invested Capital and Profitability AnalysisDocument34 pagesReturn On Invested Capital and Profitability AnalysisshldhyNo ratings yet

- HSL ApplicationDocument7 pagesHSL ApplicationKOLD News 13No ratings yet