You might also like

- MS 3404 Standard Costing and Variance AnalysisDocument6 pagesMS 3404 Standard Costing and Variance AnalysisMonica GarciaNo ratings yet

- TEST 1 TRUE/FALSE Write TRUE If The Statement Is Correct and FALSE If It Is Wrong. Avoid ErasuresDocument30 pagesTEST 1 TRUE/FALSE Write TRUE If The Statement Is Correct and FALSE If It Is Wrong. Avoid ErasuresSuga kpopNo ratings yet

- Cost Accounting (1) AnswersDocument5 pagesCost Accounting (1) AnswersMelissa Kayla ManiulitNo ratings yet

- 209384Document14 pages209384Jayson HoangNo ratings yet

- Standard Costing and Variance AnalysisDocument6 pagesStandard Costing and Variance AnalysisCeacer Julio SsekatawaNo ratings yet

- Chapter 8 Standard Cost Accounting CompressDocument13 pagesChapter 8 Standard Cost Accounting CompressJohn Kenneth Jarce CaminoNo ratings yet

- Chapter 7: Standard Costing and Variance AnalysisDocument110 pagesChapter 7: Standard Costing and Variance Analysishertzberg 1No ratings yet

- Chapter7 3 PDF FreeDocument115 pagesChapter7 3 PDF FreeAnne Thea AtienzaNo ratings yet

- Lecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument6 pagesLecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoClouie Anne TogleNo ratings yet

- Mas 9403 Standard Costs and Variance AnalysisDocument21 pagesMas 9403 Standard Costs and Variance AnalysisBanna SplitNo ratings yet

- Chapter Eleven: Standard Costs and Variance AnalysisDocument43 pagesChapter Eleven: Standard Costs and Variance AnalysisnnonscribdNo ratings yet

- FA Answer KeyDocument9 pagesFA Answer Keyimsana minatozakiNo ratings yet

- Standard Costing and Variance AnalysisDocument7 pagesStandard Costing and Variance AnalysisNicko CrisoloNo ratings yet

- MAS - Flexible Budget & Variance AnalysisDocument10 pagesMAS - Flexible Budget & Variance AnalysisKristian ArdoñaNo ratings yet

- Material Labour Overhead Cost VarianceDocument15 pagesMaterial Labour Overhead Cost VarianceSandhya RajNo ratings yet

- Chapter 10 5eDocument31 pagesChapter 10 5eChrissa Marie VienteNo ratings yet

- Variance AnalysisDocument31 pagesVariance AnalysisGift ChaliNo ratings yet

- Mas 9303 - Standard Costs and Variance AnalysisDocument21 pagesMas 9303 - Standard Costs and Variance AnalysisJowel BernabeNo ratings yet

- Study Material: Management Accounting Bba Sem ViDocument42 pagesStudy Material: Management Accounting Bba Sem ViAman MallNo ratings yet

- Standard Costing: A Functional-Based Control Approach: Questions For Writing and DiscussionDocument40 pagesStandard Costing: A Functional-Based Control Approach: Questions For Writing and DiscussionKeith Alison Arellano100% (1)

- Mas 9203 - Standard Costs and Variance AnalysisDocument20 pagesMas 9203 - Standard Costs and Variance AnalysisShefannie PaynanteNo ratings yet

- Hansen AISE IM Ch09Document57 pagesHansen AISE IM Ch09AimanNo ratings yet

- Chapter 12 - Lecture NotesDocument4 pagesChapter 12 - Lecture NotesShane MoynihanNo ratings yet

- MODULE 4 - Standard Costing and Variance AnalysisDocument7 pagesMODULE 4 - Standard Costing and Variance AnalysissampdnimNo ratings yet

- Chapter 10 SolutionsDocument68 pagesChapter 10 SolutionsMasha LankNo ratings yet

- Hca14 SM Ch08Document55 pagesHca14 SM Ch08DrellyNo ratings yet

- BLACKBOOK (Standard Costing and Variance Analysis)Document15 pagesBLACKBOOK (Standard Costing and Variance Analysis)Rashi Desai100% (1)

- Variance Analysis - Patubo, Ma. Angelli M.Document21 pagesVariance Analysis - Patubo, Ma. Angelli M.Ma Angelli PatuboNo ratings yet

- Standard Costing SWDocument2 pagesStandard Costing SWJanelleNo ratings yet

- CMA CAF-8 Important TheoryDocument14 pagesCMA CAF-8 Important TheoryShehrozSTNo ratings yet

- Mas 1304Document5 pagesMas 1304Vel JuneNo ratings yet

- Cost Accounting Raiborn and Kinney Solman Chapter 07 CompressDocument35 pagesCost Accounting Raiborn and Kinney Solman Chapter 07 CompressMa. Paula JabunganNo ratings yet

- HorngrenIMA14eTIF ch08Document42 pagesHorngrenIMA14eTIF ch08sayed7777No ratings yet

- Standard Costing and Variance AnalysisDocument64 pagesStandard Costing and Variance AnalysisPooja Grover ShandilyaNo ratings yet

- SCM Discussion 6Document10 pagesSCM Discussion 6M4ZONSK1E OfficialNo ratings yet

- Sol14 4eDocument103 pagesSol14 4eKiều Thảo Anh100% (1)

- InstructionsDocument36 pagesInstructionsjhouvan50% (6)

- Standard Costing and The Balance ScorecardDocument76 pagesStandard Costing and The Balance ScorecardSaifurKomolNo ratings yet

- Performance Evaluation Using Variances From Standard CostsDocument3 pagesPerformance Evaluation Using Variances From Standard CostsJhoylie BesinNo ratings yet

- Unit 4Document7 pagesUnit 4Manojkumar MohanasundramNo ratings yet

- SC-Chapter 10-STD COSTING-A MANAGERIAL TOOLDocument31 pagesSC-Chapter 10-STD COSTING-A MANAGERIAL TOOLDaniel John Cañares LegaspiNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Chapter 16 - AnswerDocument14 pagesChapter 16 - AnswerMarlon A. RodriguezNo ratings yet

- AEC 108 (MA) Semifinal Learning Materials 1Document5 pagesAEC 108 (MA) Semifinal Learning Materials 1Dave Shem DivinoNo ratings yet

- Managerial Accounting CHPTR 9Document7 pagesManagerial Accounting CHPTR 9Rifqi Dhia RamadhanNo ratings yet

- COST of DeathDocument267 pagesCOST of DeathQwerty TyuNo ratings yet

- Standard Costing PDFDocument36 pagesStandard Costing PDFRamesh ShriNo ratings yet

- Mas 2605Document6 pagesMas 2605John Philip CastroNo ratings yet

- Summary Accounting Management Chapter 9Document3 pagesSummary Accounting Management Chapter 9Fathinus SyafrizalNo ratings yet

- Standard Costing Summary For CA Inter, CMA Inter, CS ExecutiveDocument5 pagesStandard Costing Summary For CA Inter, CMA Inter, CS Executivecd classes100% (1)

- Distinguish Between Marginal Costing and Absorption CostingDocument10 pagesDistinguish Between Marginal Costing and Absorption Costingmohamed Suhuraab50% (2)

- Break Even AnalysisDocument6 pagesBreak Even AnalysisTria Putri NoviasariNo ratings yet

- Finance for Non-Financiers 2: Professional FinancesFrom EverandFinance for Non-Financiers 2: Professional FinancesNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- Accounting, Maths and Computing Principles for Business Studies V11From EverandAccounting, Maths and Computing Principles for Business Studies V11No ratings yet

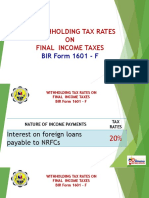

- Ii. Withholding Tax Rates ON Final Income Taxes: BIR Form 1601 - FDocument28 pagesIi. Withholding Tax Rates ON Final Income Taxes: BIR Form 1601 - FAustin Viel Lagman MedinaNo ratings yet

- FAR Preboard SolutionsDocument6 pagesFAR Preboard SolutionsHikariNo ratings yet

- Intellectual Property Law (R.A. No. 8293 A.K.A. Intellectual Property Code of The Philippines)Document5 pagesIntellectual Property Law (R.A. No. 8293 A.K.A. Intellectual Property Code of The Philippines)HikariNo ratings yet

- Reorganization of DOHDocument9 pagesReorganization of DOHHikariNo ratings yet

- FAR Preboard SolutionsDocument4 pagesFAR Preboard SolutionsHikariNo ratings yet

- MethodsDocument6 pagesMethodsHikariNo ratings yet

- Basic Concepts (Cost Accounting)Document9 pagesBasic Concepts (Cost Accounting)alexandro_novora6396No ratings yet

- Securities Regulation CodeDocument11 pagesSecurities Regulation CodeHikariNo ratings yet

- Management AccountingDocument3 pagesManagement AccountingHikariNo ratings yet

- P2 105 Agency Home Office and Branch Accounting Key AnswersDocument6 pagesP2 105 Agency Home Office and Branch Accounting Key AnswersHikari100% (1)

- Biological MoleculesDocument61 pagesBiological MoleculesHikariNo ratings yet

- PFRS Adopted by SEC As of December 31, 2011 PDFDocument27 pagesPFRS Adopted by SEC As of December 31, 2011 PDFJennybabe PetaNo ratings yet

- Cell TransportDocument37 pagesCell TransportHikariNo ratings yet

- Tff3e Chapsumm ch05Document3 pagesTff3e Chapsumm ch05Collins CheruiyotNo ratings yet

- Analysis of Variances From Standard Costs - Solutions PDFDocument39 pagesAnalysis of Variances From Standard Costs - Solutions PDFHikariNo ratings yet

- Chap 005Document32 pagesChap 005HikariNo ratings yet

- The Audit Process: Health Research & Informat Ion Division, ESRI, Dublin, July 2008Document36 pagesThe Audit Process: Health Research & Informat Ion Division, ESRI, Dublin, July 2008HikariNo ratings yet

- Pre Planning PDFDocument5 pagesPre Planning PDFHikariNo ratings yet

- Auditing Theory Solution Manual by Salosagcol (Posted)Document4 pagesAuditing Theory Solution Manual by Salosagcol (Posted)HikariNo ratings yet

- ResearchDocument1 pageResearchHikariNo ratings yet

- Strategik 8Document64 pagesStrategik 8HikariNo ratings yet

- RMYC ScheduleDocument12 pagesRMYC ScheduleHikariNo ratings yet

- Owl ApaformatDocument38 pagesOwl Apaformatapi-268267969No ratings yet

- At PreboardDocument12 pagesAt PreboardKevin Ryan EscobarNo ratings yet

- Basic Accounting Test Questions1Document4 pagesBasic Accounting Test Questions1Ervin CabangalNo ratings yet

- Quick BooksDocument2 pagesQuick BooksHikariNo ratings yet

- Business Com Cni 16 18Document3 pagesBusiness Com Cni 16 18HikariNo ratings yet

- Chapter 01 - AnswerDocument18 pagesChapter 01 - AnswerTJ NgNo ratings yet

- Key Answer of Chapter 22 of Nonprofit Organization by GuereroDocument8 pagesKey Answer of Chapter 22 of Nonprofit Organization by GuereroArmia MarquezNo ratings yet

- Review Materials For DeptlDocument4 pagesReview Materials For DeptlSteffNo ratings yet

- Cin CustomizingDocument94 pagesCin CustomizingBiranchi MishraNo ratings yet

- BUS 475 Capstone Final Exam AnswersDocument16 pagesBUS 475 Capstone Final Exam AnswersangleefanslerNo ratings yet

- Final Talk - Luxury BrandsDocument58 pagesFinal Talk - Luxury BrandsDr. Firoze KhanNo ratings yet

- MaggiDocument8 pagesMaggiManisha SharmaNo ratings yet

- January 2008 Unit 3Document28 pagesJanuary 2008 Unit 3Stella GeorgiouNo ratings yet

- Marketing Strategy of Dabur ChwanprashDocument97 pagesMarketing Strategy of Dabur ChwanprashPalash Roy78% (9)

- Tourism SectorDocument52 pagesTourism SectorNikita Gavaskar0% (1)

- SAP SD Depot ProcessDocument47 pagesSAP SD Depot ProcessLu VanderhöffNo ratings yet

- Amadeus Reissue and Ticketing ManualDocument0 pagesAmadeus Reissue and Ticketing ManualAndrew SanchezNo ratings yet

- Vat 4Document4 pagesVat 4Allen KateNo ratings yet

- Entrepreneurship Sachin Bansal FlipkartDocument10 pagesEntrepreneurship Sachin Bansal FlipkartamitcmsNo ratings yet

- Materials ManagementDocument12 pagesMaterials ManagementJoginder GrewalNo ratings yet

- Joe Deklic - Final2Document1 pageJoe Deklic - Final2api-374894269No ratings yet

- Retail Planning ProcessDocument21 pagesRetail Planning ProcessRohan KumarNo ratings yet

- SWOT Analysis of SHG's Nurtured by Nirmaan-GoaDocument4 pagesSWOT Analysis of SHG's Nurtured by Nirmaan-Goachandrahas1993No ratings yet

- Chesbrough - Business Model Innovation - Opportunities and BarriersDocument10 pagesChesbrough - Business Model Innovation - Opportunities and BarriersDanielrosa1No ratings yet

- Ebook EcommerceDocument330 pagesEbook EcommerceIvett A. Yapias Avilez100% (1)

- Coordination in A Supply Chain by K L N REDDYDocument32 pagesCoordination in A Supply Chain by K L N REDDYjayamsecNo ratings yet

- Sample Set 1Document10 pagesSample Set 1Rajeev SharmaNo ratings yet

- Katalyst Wealth - A Free Guide To Grow Your Wealth by 190 TimesDocument21 pagesKatalyst Wealth - A Free Guide To Grow Your Wealth by 190 TimesKatalyst WealthNo ratings yet

- Test 1Document4 pagesTest 1phlupoNo ratings yet

- Entrepreneur Lesson 7 ForecastingDocument33 pagesEntrepreneur Lesson 7 ForecastingMelvin AlarillaNo ratings yet

- Customer Pyramid - Homa Hi-LitesDocument7 pagesCustomer Pyramid - Homa Hi-Liteseric_biswasNo ratings yet

- Ewing v. Buttercup Margarine Company, Limited (1917)Document9 pagesEwing v. Buttercup Margarine Company, Limited (1917)Mohammad Adil Khushi0% (1)

- OREODocument15 pagesOREOPRIYA KUMARINo ratings yet

- ContempDocument3 pagesContempCecilia AgathaNo ratings yet

- Hul SwotDocument17 pagesHul SwotAbhishek KanodiaNo ratings yet

- Business PlanDocument16 pagesBusiness PlanLisa B Arnold100% (1)

- Product Decision and FormulationDocument7 pagesProduct Decision and FormulationLeena Avhad KhadeNo ratings yet

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-1-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)