You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- SOM Postgrad BrochureDocument2 pagesSOM Postgrad BrochurePatrick MugoNo ratings yet

- Project Work Plan For Project: Valuation of Risk Premium Using Emprical Bayes ModelsDocument2 pagesProject Work Plan For Project: Valuation of Risk Premium Using Emprical Bayes ModelsPatrick MugoNo ratings yet

- Model Selection and Claim Frequency For Workers' Compensation InsuranceDocument30 pagesModel Selection and Claim Frequency For Workers' Compensation InsurancePatrick MugoNo ratings yet

- ADVERT - 18th December 2017Document116 pagesADVERT - 18th December 2017Patrick MugoNo ratings yet

- Data Request Icea LionDocument1 pageData Request Icea LionPatrick MugoNo ratings yet

- st42010 2014Document198 pagesst42010 2014Patrick MugoNo ratings yet

- 406 Mark SchemeDocument4 pages406 Mark SchemePatrick MugoNo ratings yet

- Howard PittmanDocument15 pagesHoward PittmanPatrick Mugo100% (1)

- Examination: Subject ST4 Pensions and Other Benefits Specialist TechnicalDocument185 pagesExamination: Subject ST4 Pensions and Other Benefits Specialist TechnicalPatrick MugoNo ratings yet

- Obimbo Moses CV Feb 2016Document14 pagesObimbo Moses CV Feb 2016Patrick MugoNo ratings yet

- The Life of F.F. Bosworth by Roberts Liardon - HopeFaithPrayerDocument43 pagesThe Life of F.F. Bosworth by Roberts Liardon - HopeFaithPrayerPatrick MugoNo ratings yet

- Scriptures Against Depression - HopeFaithPrayerDocument14 pagesScriptures Against Depression - HopeFaithPrayerPatrick MugoNo ratings yet

- Report For Practical Placement From 16th Jan To 3rd March 2017Document20 pagesReport For Practical Placement From 16th Jan To 3rd March 2017Patrick MugoNo ratings yet

- Gig 98 PMDocument1 pageGig 98 PMPatrick MugoNo ratings yet

- Examination: Subject CT1 Financial Mathematics Core TechnicalDocument282 pagesExamination: Subject CT1 Financial Mathematics Core TechnicalPatrick MugoNo ratings yet

- IandF CT6 201509 ExaminersReport v4Document14 pagesIandF CT6 201509 ExaminersReport v4Patrick MugoNo ratings yet

- IandF CT5 201604 ExaminersReportDocument16 pagesIandF CT5 201604 ExaminersReportPatrick MugoNo ratings yet

- Institute and Faculty of Actuaries: Subject CT6 - Statistical Methods Core TechnicalDocument16 pagesInstitute and Faculty of Actuaries: Subject CT6 - Statistical Methods Core TechnicalPatrick MugoNo ratings yet

- Institute and Faculty of Actuaries: Subject CT7 - Business Economics Core TechnicalDocument13 pagesInstitute and Faculty of Actuaries: Subject CT7 - Business Economics Core TechnicalPatrick MugoNo ratings yet

- FandI Subj304 199904 ExampaperDocument5 pagesFandI Subj304 199904 ExampaperPatrick MugoNo ratings yet

- IandF CT4 201604 ExamDocument9 pagesIandF CT4 201604 ExamPatrick MugoNo ratings yet

- IandF CT7 201509 ExaminersReportDocument13 pagesIandF CT7 201509 ExaminersReportPatrick MugoNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- PGBP Complete TheoryDocument21 pagesPGBP Complete TheoryNirbheek Doyal100% (4)

- Bike Insurance PDFDocument3 pagesBike Insurance PDFSenthil KumarNo ratings yet

- CoachUp Evidence of InsuranceDocument2 pagesCoachUp Evidence of InsurancecoachupNo ratings yet

- What Is Business Risk?Document6 pagesWhat Is Business Risk?Jcee JulyNo ratings yet

- 01 - Home Finance BookletDocument72 pages01 - Home Finance BookletWeedrowNo ratings yet

- Private Car Package Policy: Certificate of Insurance Cum Policy ScheduleDocument2 pagesPrivate Car Package Policy: Certificate of Insurance Cum Policy ScheduleBhuvanesh WaranNo ratings yet

- MyShield N MyHealthPlus Brochure April2016Document24 pagesMyShield N MyHealthPlus Brochure April2016CaddyTanNo ratings yet

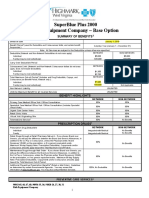

- Rish Equipment Base Plan Option Eff. 1.1.2019Document4 pagesRish Equipment Base Plan Option Eff. 1.1.2019michala anthonyNo ratings yet

- SwissCare Sum PolicyDocument16 pagesSwissCare Sum PolicyFrancesca SartiniNo ratings yet

- 2006 BIR - Ruling - DA 745 06 - 20180405 1159 SdfparDocument7 pages2006 BIR - Ruling - DA 745 06 - 20180405 1159 Sdfpar--No ratings yet

- 48 2020 2430 PDFDocument3 pages48 2020 2430 PDFRamya PatelNo ratings yet

- Aetna DMO Dental Benefits - May 2019Document6 pagesAetna DMO Dental Benefits - May 2019saksham23No ratings yet

- 03 - Mental Accounting - HANDOUTDocument8 pages03 - Mental Accounting - HANDOUTtkkt1015No ratings yet

- PDF&Rendition Converted SignedDocument71 pagesPDF&Rendition Converted Signedmanwanimuki12No ratings yet

- Aspire - Rate Cards - v3Document83 pagesAspire - Rate Cards - v3Ronak RanaNo ratings yet

- Policy PrintDocument6 pagesPolicy PrintDivakar BNo ratings yet

- Kareo Payment Posting GuideDocument45 pagesKareo Payment Posting Guidejasri012412No ratings yet

- Sydnor2010 - Overinsuring Modest RisksDocument24 pagesSydnor2010 - Overinsuring Modest RisksRoberto PaezNo ratings yet

- QAP-16 Subcontracting ProcedureDocument49 pagesQAP-16 Subcontracting Procedurenaseema1100% (5)

- McGraw Hill Personal Finance Chapter 9Document2 pagesMcGraw Hill Personal Finance Chapter 9Kathleen0% (1)

- 5) Zenith Insurance Corporation vs. Court of Appeals, 185 SCRA 398, G.R. No. 85296 May 14, 1990Document6 pages5) Zenith Insurance Corporation vs. Court of Appeals, 185 SCRA 398, G.R. No. 85296 May 14, 1990Alexiss Mace JuradoNo ratings yet

- Personal Auto: Direct General Insurance CompanyDocument2 pagesPersonal Auto: Direct General Insurance Companyrosmel fernandezNo ratings yet

- Schedule INDM202200111963 0.HomeLiteDocument51 pagesSchedule INDM202200111963 0.HomeLiteZeeshan HasanNo ratings yet

- Cms 1500Document2 pagesCms 1500api-295063762No ratings yet

- Certificate Cum Policy Schedule: Gccv-Public Carriers Other Than Three Wheelers Package Policy - Zone CDocument1 pageCertificate Cum Policy Schedule: Gccv-Public Carriers Other Than Three Wheelers Package Policy - Zone CAnand SNo ratings yet

- Sales LiteratureDocument15 pagesSales Literaturehimanshu200k5154No ratings yet

- Practice Problem Set 6Document7 pagesPractice Problem Set 6AkshayNo ratings yet

- CH 01 Au 4920 - 221121 - 125359Document1 pageCH 01 Au 4920 - 221121 - 125359Mallika GhoshNo ratings yet

- Religare Report Print PDFDocument50 pagesReligare Report Print PDFumeshtyagi011233% (3)

- Appendix To Tender V0Document3 pagesAppendix To Tender V0nifrasNo ratings yet