You might also like

- Sps Buffe Vs Sec GonzalesDocument1 pageSps Buffe Vs Sec GonzalesHiroshi CarlosNo ratings yet

- Case Digest 1 10Document23 pagesCase Digest 1 10louis jansenNo ratings yet

- Material Master-Approval ProcessDocument7 pagesMaterial Master-Approval ProcessHiroshi CarlosNo ratings yet

- BCCFI Vs CA and SIHI (1994) - Holder Who Presented Crossed Checks Payable To Another Person Is Not A Holder in Due Course. Holder Not in Due Course May Collect From The Named Payee.Document3 pagesBCCFI Vs CA and SIHI (1994) - Holder Who Presented Crossed Checks Payable To Another Person Is Not A Holder in Due Course. Holder Not in Due Course May Collect From The Named Payee.Hiroshi CarlosNo ratings yet

- Sps Villuga Et Al Vs KellyDocument5 pagesSps Villuga Et Al Vs KellyHiroshi CarlosNo ratings yet

- 11 The Holy See Vs Rosario Jr.Document2 pages11 The Holy See Vs Rosario Jr.Hiroshi CarlosNo ratings yet

- Supreme Court upholds constitutionality of Retail Trade Liberalization Act (2010Document3 pagesSupreme Court upholds constitutionality of Retail Trade Liberalization Act (2010Hiroshi CarlosNo ratings yet

- 49 NAPOCOR Vs Province of QuezonDocument1 page49 NAPOCOR Vs Province of QuezonHiroshi CarlosNo ratings yet

- Social Legislation Bar QuestionsDocument17 pagesSocial Legislation Bar QuestionsHiroshi Carlos100% (1)

- 11 The Holy See Vs Rosario Jr.Document2 pages11 The Holy See Vs Rosario Jr.Hiroshi CarlosNo ratings yet

- Dolores Natanuan Vs Atty TolentinoDocument1 pageDolores Natanuan Vs Atty TolentinoHiroshi CarlosNo ratings yet

- Fortunata Vs CADocument4 pagesFortunata Vs CAHiroshi CarlosNo ratings yet

- Service Manager Policy Investigation Confession UsedDocument1 pageService Manager Policy Investigation Confession UsedHiroshi CarlosNo ratings yet

- 02 Sison Vs Board of AccountancyDocument3 pages02 Sison Vs Board of AccountancyHiroshi CarlosNo ratings yet

- Case Digest 1 10Document23 pagesCase Digest 1 10louis jansenNo ratings yet

- Gonzales Vs ComelecDocument2 pagesGonzales Vs ComelecMaria Cherrylen Castor QuijadaNo ratings yet

- Fortunata Vs CADocument4 pagesFortunata Vs CAHiroshi CarlosNo ratings yet

- 11 The Holy See Vs Rosario Jr.Document2 pages11 The Holy See Vs Rosario Jr.Hiroshi CarlosNo ratings yet

- 07 Maloles II Vs PhillipsDocument5 pages07 Maloles II Vs PhillipsHiroshi CarlosNo ratings yet

- 03 Northwest Orient Airlines Vs CA 2Document3 pages03 Northwest Orient Airlines Vs CA 2Hiroshi CarlosNo ratings yet

- 21 Fort Vs CIR DigestDocument3 pages21 Fort Vs CIR DigestHiroshi CarlosNo ratings yet

- 19 Mindanao Vs CIR DigestedDocument2 pages19 Mindanao Vs CIR DigestedHiroshi CarlosNo ratings yet

- Banco Do Brasil Vs CADocument2 pagesBanco Do Brasil Vs CAHiroshi CarlosNo ratings yet

- Banares Vs BalisingDocument5 pagesBanares Vs BalisingHiroshi Carlos100% (1)

- Ecumenical Prayer For The CourtsDocument1 pageEcumenical Prayer For The CourtsChristel Allena-Geronimo100% (3)

- Carcia Vs DrilonDocument36 pagesCarcia Vs DrilonHiroshi CarlosNo ratings yet

- Abangan Will Probate RequirementsDocument1 pageAbangan Will Probate RequirementsHiroshi CarlosNo ratings yet

- Credit ReviewerDocument1 pageCredit ReviewerHiroshi CarlosNo ratings yet

- 03 Tolentino Vs VillanuevaDocument2 pages03 Tolentino Vs VillanuevaHiroshi CarlosNo ratings yet

- 13 People V Hayag DigestedDocument1 page13 People V Hayag DigestedHiroshi CarlosNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 2nd Merit ListDocument4 pages2nd Merit ListberkkesahabiaNo ratings yet

- Who bears loss before deliveryDocument2 pagesWho bears loss before deliverykelo100% (2)

- Law of Property and Security ADocument32 pagesLaw of Property and Security ALipton NcubeNo ratings yet

- Summary of The Berne Convention For The Protection of Literary and Artistic WorksDocument3 pagesSummary of The Berne Convention For The Protection of Literary and Artistic Workssweetlunacy00100% (2)

- Republic vs. HidalgoDocument2 pagesRepublic vs. HidalgoAngelo Raphael B. Delmundo100% (1)

- Yao Ka Sin Vs CADocument2 pagesYao Ka Sin Vs CAMasterboleroNo ratings yet

- Mallion Vs AlcantaraDocument4 pagesMallion Vs AlcantaraAngelie ManingasNo ratings yet

- Mountain Top Timber Products BankruptcyDocument4 pagesMountain Top Timber Products BankruptcyAnonymous ROc32R1gNo ratings yet

- VL Order Judge Jonathan Karesh Against Michelle Fotinos: San Mateo County Superior Court - The Conservatorship of the Person and Estate of Esther R. Boyes - Vexatious Litigant Proceeding San Mateo Superior Court - Presiding Judge John GrandsaertDocument7 pagesVL Order Judge Jonathan Karesh Against Michelle Fotinos: San Mateo County Superior Court - The Conservatorship of the Person and Estate of Esther R. Boyes - Vexatious Litigant Proceeding San Mateo Superior Court - Presiding Judge John GrandsaertCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story IdeasNo ratings yet

- Abid RazaDocument1 pageAbid RazaLaura WilkersonNo ratings yet

- TRIPS AgreementDocument32 pagesTRIPS AgreementVineet JainNo ratings yet

- Closure of Business Representative Office RequirementsDocument2 pagesClosure of Business Representative Office RequirementsSalvador Andrew TugadeNo ratings yet

- Societies Registration ChecklistDocument16 pagesSocieties Registration ChecklistAbhijit BobadeNo ratings yet

- Barnhizer Contractsi 1Document12 pagesBarnhizer Contractsi 1piddes1234No ratings yet

- RFBT2Document4 pagesRFBT2Arianne AbonalesNo ratings yet

- Guidelines For Preparation of DPRDocument1 pageGuidelines For Preparation of DPRSabhaya ChiragNo ratings yet

- 0096 0467 - Property Crossing Agreement Kseb in Stamp PaperDocument2 pages0096 0467 - Property Crossing Agreement Kseb in Stamp PaperSreedharanPN67% (6)

- Registration of TrademarkDocument24 pagesRegistration of TrademarkAnirudh AroraNo ratings yet

- Sample Manufacturing AgreementDocument4 pagesSample Manufacturing AgreementAditya LakhaniNo ratings yet

- Ken Dandar v. Scientology: State Appeal 2014Document63 pagesKen Dandar v. Scientology: State Appeal 2014Tony OrtegaNo ratings yet

- 2018 Sigma Rho Fraternity Bar Operations CIVIL LAW Bar QA 1996 2017 PDFDocument105 pages2018 Sigma Rho Fraternity Bar Operations CIVIL LAW Bar QA 1996 2017 PDFMa-an Soriano100% (1)

- Tenancy Agreement 1Document3 pagesTenancy Agreement 1Teoh Wen DeeNo ratings yet

- Affidavit of Acknowledgment of PaternityDocument14 pagesAffidavit of Acknowledgment of PaternityPedro SiloNo ratings yet

- PAL v. RamosDocument2 pagesPAL v. Ramoskim_santos_20No ratings yet

- The Lindsay Petroleum Company Appellants AnDocument18 pagesThe Lindsay Petroleum Company Appellants AnChin Kuen YeiNo ratings yet

- Kolin Electronics Co., Inc. v. Kolin Phils. International, Inc., G.R. No. 228165, Feb. 9, 202Document28 pagesKolin Electronics Co., Inc. v. Kolin Phils. International, Inc., G.R. No. 228165, Feb. 9, 202Christopher ArellanoNo ratings yet

- Law of Contract II Assignment IIDocument10 pagesLaw of Contract II Assignment IIFrancis BandaNo ratings yet

- Filipinas Life Assurance Vs NavaDocument5 pagesFilipinas Life Assurance Vs NavaJohn Michael BabasNo ratings yet

- CHAPTER 5 Sales Obligations of The VendeeDocument3 pagesCHAPTER 5 Sales Obligations of The VendeeErra PeñafloridaNo ratings yet

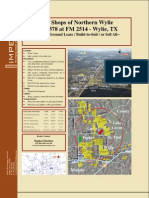

- Shops of Northern Wylie (Imperium Holdings)Document3 pagesShops of Northern Wylie (Imperium Holdings)Imperium Holdings, LPNo ratings yet