You might also like

- Income Taxation - Chapter 1 DefinitionDocument3 pagesIncome Taxation - Chapter 1 DefinitionAntonioGloriaComiqueNo ratings yet

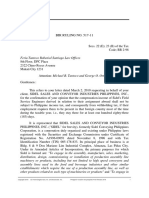

- Sidel RulingDocument6 pagesSidel RulingMarc Exequiel TeodoroNo ratings yet

- Obligations and contracts: Payment rules and currency valuesDocument23 pagesObligations and contracts: Payment rules and currency valuesLouisa Andrea O. PielagoNo ratings yet

- De Minimis and FringeDocument1 pageDe Minimis and FringeAlicia Jane NavarroNo ratings yet

- Customer Manual On BOI ServicesDocument63 pagesCustomer Manual On BOI ServicesscrewthebooksNo ratings yet

- #15 Notes in Allowable DeductionsDocument15 pages#15 Notes in Allowable DeductionsJaypee Palcis100% (1)

- FYCE BM1804 - Income Taxation HandoutDocument17 pagesFYCE BM1804 - Income Taxation HandoutLisanna DragneelNo ratings yet

- Bir Ruling (Da 013 08)Document5 pagesBir Ruling (Da 013 08)Jake PeraltaNo ratings yet

- ACCTBA1 - Exercises On Adjusting EntriesDocument5 pagesACCTBA1 - Exercises On Adjusting EntriesRichard Leighton100% (1)

- Philippine Framework For Assurance EngagementsDocument15 pagesPhilippine Framework For Assurance EngagementsAnonymous LC5kFdtcNo ratings yet

- Deductions From Gross IncomeDocument23 pagesDeductions From Gross IncomeAidyl PerezNo ratings yet

- Conditions foreign CPAs practice accountancy PhilippinesDocument3 pagesConditions foreign CPAs practice accountancy PhilippinesANGELU RANE BAGARES INTOLNo ratings yet

- Pledge Mortgage Agency NotesDocument4 pagesPledge Mortgage Agency NotesYoshi BalasiNo ratings yet

- Jeter Advanced Accounting 4eDocument14 pagesJeter Advanced Accounting 4eMinh NguyễnNo ratings yet

- LAW ON NEGOTIABLE INSTRUMENTSDocument13 pagesLAW ON NEGOTIABLE INSTRUMENTSDae JosecoNo ratings yet

- UPRevised Banking ReviewerDocument76 pagesUPRevised Banking ReviewerRomel TorresNo ratings yet

- CORP POWERSDocument37 pagesCORP POWERSKelvin CulajaráNo ratings yet

- Agabon DoctrineDocument7 pagesAgabon DoctrineLudica OjaNo ratings yet

- CHAPTER 8 - DepreciationDocument12 pagesCHAPTER 8 - DepreciationMuhammad AdibNo ratings yet

- 8 TAX 1 Group 8 - Fringe Benefits Tax, 13th Month Pay and Other Benefits Excluded From GIDocument60 pages8 TAX 1 Group 8 - Fringe Benefits Tax, 13th Month Pay and Other Benefits Excluded From GIFC EstoestaNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDocument76 pagesBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledFrancis Coronel Jr.No ratings yet

- Tax Reviewer (UP)Document163 pagesTax Reviewer (UP)Rap ReyesNo ratings yet

- PDIC Illustrative ProblemsDocument5 pagesPDIC Illustrative ProblemsDiscord HowNo ratings yet

- FBT Quiz TitleDocument7 pagesFBT Quiz TitleNicole Daphne FigueroaNo ratings yet

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 pagesIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarNo ratings yet

- Exclusions To Gross IncomeDocument8 pagesExclusions To Gross IncomeNishikata MaseoNo ratings yet

- SEC 34 (Deductions From Gross Income)Document111 pagesSEC 34 (Deductions From Gross Income)Joseph James JimenezNo ratings yet

- PHILIPPINE INCOME TAX REVIEWERDocument99 pagesPHILIPPINE INCOME TAX REVIEWERquedan_socotNo ratings yet

- PDF Sales Midterm Reviewer by Article 1530 1593pdfDocument43 pagesPDF Sales Midterm Reviewer by Article 1530 1593pdfsoyoung kimNo ratings yet

- Labor Code provisions on working hours, rest days, holidays, leaves and chargesDocument36 pagesLabor Code provisions on working hours, rest days, holidays, leaves and chargesPearl Angeli Quisido CanadaNo ratings yet

- Individual Income TaxationDocument50 pagesIndividual Income TaxationGab RielNo ratings yet

- Tax 1 FinalsDocument16 pagesTax 1 FinalsDenise DuriasNo ratings yet

- Taxation Reviewer: Taxation in Act and Inherent Provide Money To Pay)Document5 pagesTaxation Reviewer: Taxation in Act and Inherent Provide Money To Pay)Maria Elena AquinoNo ratings yet

- Accounting ModuleDocument104 pagesAccounting ModuleMa Fe PunzalanNo ratings yet

- TAX - Corporations With Special RatesDocument16 pagesTAX - Corporations With Special RatesZaaavnn Vannnnn100% (1)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document33 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- What Is PledgeDocument5 pagesWhat Is PledgerabiatussalehaNo ratings yet

- Tax Rev Prelim ExaminationDocument91 pagesTax Rev Prelim ExaminationshanksNo ratings yet

- Introduction to Taxation Concepts & RulesDocument1 pageIntroduction to Taxation Concepts & Rulesdannavillafuente0% (1)

- Rights of Unpaid Seller and Buyer in Sales ContractsDocument21 pagesRights of Unpaid Seller and Buyer in Sales ContractsAmie Jane MirandaNo ratings yet

- Kinds of WarrantyDocument10 pagesKinds of WarrantyJodie Ann PajacNo ratings yet

- General Banking Law of 2000Document25 pagesGeneral Banking Law of 2000John Rey Bantay RodriguezNo ratings yet

- Tax 1 ReviewerDocument16 pagesTax 1 ReviewerverkieNo ratings yet

- Module in General Banking Law of 2000Document9 pagesModule in General Banking Law of 2000Nieves GalvezNo ratings yet

- Chapter 5 Statement of Changes in EquityDocument6 pagesChapter 5 Statement of Changes in EquitylcNo ratings yet

- Constitutional LimitationsDocument66 pagesConstitutional LimitationsDev LitaNo ratings yet

- Chapter 2 Taxes Tax Law and Tax AdministrationDocument37 pagesChapter 2 Taxes Tax Law and Tax AdministrationJohn Galleno100% (1)

- 3m Philippines, Inc. v. Lauro D. YusecoDocument1 page3m Philippines, Inc. v. Lauro D. YusecoMark Anthony ReyesNo ratings yet

- Module 1 - Fundamental Principles - Lecture NotesDocument25 pagesModule 1 - Fundamental Principles - Lecture NotesRina Bico AdvinculaNo ratings yet

- 11-T-11 Admin & Judicial ProceduresDocument22 pages11-T-11 Admin & Judicial ProceduresCherrylyn CaliwanNo ratings yet

- Cost Accounting Questions and AnswersDocument1 pageCost Accounting Questions and AnswersKyo TieNo ratings yet

- Chapter 9Document10 pagesChapter 9Caleb John SenadosNo ratings yet

- CONTRACTS Chapter 1 General ProvisionsDocument2 pagesCONTRACTS Chapter 1 General ProvisionsShanelle MacajilosNo ratings yet

- Manual On Financial Manager of Barangays Module 3Document11 pagesManual On Financial Manager of Barangays Module 3vicsNo ratings yet

- REHABILITATION OR LIQUIDATION OF FINANCIALLY DISTRESSED ENTERPRISESDocument19 pagesREHABILITATION OR LIQUIDATION OF FINANCIALLY DISTRESSED ENTERPRISESJAMAL ALINo ratings yet

- Law On Sales ReviewerDocument1 pageLaw On Sales ReviewerNath BongalonNo ratings yet

- Tax Reviewer - Train Law - Rates and ComputationsDocument5 pagesTax Reviewer - Train Law - Rates and ComputationsCelestiaNo ratings yet

- Chapter 3 Fringe & de Minimis BenefitsDocument6 pagesChapter 3 Fringe & de Minimis BenefitsNovelyn Hiso-anNo ratings yet

- De-Minimis-Benefits-2024Document1 pageDe-Minimis-Benefits-2024Love Heart BantilesNo ratings yet

- Fringe Benefits TaxDocument3 pagesFringe Benefits TaxGrace EspirituNo ratings yet

- A.C. No. 7022 June 18, 2008 MARJORIE F. SAMANIEGO, Complainant, ATTY. ANDREW V. FERRER, Respondent. Resolution Quisumbing, J.Document4 pagesA.C. No. 7022 June 18, 2008 MARJORIE F. SAMANIEGO, Complainant, ATTY. ANDREW V. FERRER, Respondent. Resolution Quisumbing, J.lossesaboundNo ratings yet

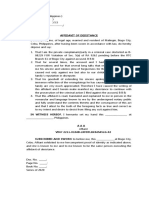

- Affidavit of DesistanceDocument1 pageAffidavit of DesistancelossesaboundNo ratings yet

- Case 3 MemorandumDocument4 pagesCase 3 MemorandumlossesaboundNo ratings yet

- St. Louis University Laboratory High School (Slu-Lhs) Faculty and Staff, A.C. No. 6010Document9 pagesSt. Louis University Laboratory High School (Slu-Lhs) Faculty and Staff, A.C. No. 6010lossesaboundNo ratings yet

- Affidavit of DesistanceDocument1 pageAffidavit of DesistancelossesaboundNo ratings yet

- Tacloban City Mayor Romualdez EO 2020-03-016Document3 pagesTacloban City Mayor Romualdez EO 2020-03-016lossesaboundNo ratings yet

- Affidavit of Desistance SampleDocument2 pagesAffidavit of Desistance Sampleusjrlaw201175% (4)

- Application Form For The National Bureau of InvestigationDocument8 pagesApplication Form For The National Bureau of InvestigationlossesaboundNo ratings yet

- ANTONIO A. ALCANTARA, Complainant, vs. ATTY. MARIANO PEFIANCO, RespondentDocument2 pagesANTONIO A. ALCANTARA, Complainant, vs. ATTY. MARIANO PEFIANCO, RespondentlossesaboundNo ratings yet

- Court Forms ListDocument3 pagesCourt Forms ListEuodia HodeshNo ratings yet

- Rebecca B. Arnobit, A.C. No. 1481: Per CuriamDocument6 pagesRebecca B. Arnobit, A.C. No. 1481: Per CuriamlossesaboundNo ratings yet

- Emplyment BackgroundDocument1 pageEmplyment BackgroundlossesaboundNo ratings yet

- MTAP Reviewer Grade 4 - 2Document2 pagesMTAP Reviewer Grade 4 - 2lossesaboundNo ratings yet

- Commercial Law CasesDocument8 pagesCommercial Law CaseslossesaboundNo ratings yet

- Tax Review Case DigestsDocument11 pagesTax Review Case DigestslossesaboundNo ratings yet

- Administrative Order No 07Document10 pagesAdministrative Order No 07Anonymous zuizPMNo ratings yet

- St. Scholastica's College Tacloban: Week 4Document2 pagesSt. Scholastica's College Tacloban: Week 4lossesaboundNo ratings yet

- Office of The ProsecutorDocument4 pagesOffice of The ProsecutorlossesaboundNo ratings yet

- REMEDIESDocument10 pagesREMEDIESlossesaboundNo ratings yet

- Complaint AffidavitDocument10 pagesComplaint AffidavitMaimai Molina82% (11)

- Jurisprudence and Law For Administrative CaseDocument7 pagesJurisprudence and Law For Administrative CaselossesaboundNo ratings yet

- MTAP Reviewer Grade 4Document2 pagesMTAP Reviewer Grade 4lossesaboundNo ratings yet

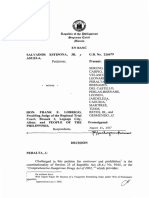

- Estipona V Lobrigo GR 226679 - 2017Document11 pagesEstipona V Lobrigo GR 226679 - 2017lossesaboundNo ratings yet

- Information: Republic of The Philippines Regional Trial Court 8 Judicial Region Branch VIDocument2 pagesInformation: Republic of The Philippines Regional Trial Court 8 Judicial Region Branch VIlossesaboundNo ratings yet

- Form F18: Affidavit of Next of Kin: City State Day MonthDocument1 pageForm F18: Affidavit of Next of Kin: City State Day MonthShiena Rose Pactoranan ServillonNo ratings yet

- 226679Document21 pages226679Trishia Fernandez Garcia100% (3)

- G.R. No. 93695 Lee vs. CADocument19 pagesG.R. No. 93695 Lee vs. CAlossesaboundNo ratings yet

- Post-Midterms Sales HandoutDocument52 pagesPost-Midterms Sales HandoutlossesaboundNo ratings yet

- Coffee and Doughnuts - Complaint For Unlawful Detainer Sample PDFDocument3 pagesCoffee and Doughnuts - Complaint For Unlawful Detainer Sample PDFlossesaboundNo ratings yet

- Taxation of Submarine CablesDocument26 pagesTaxation of Submarine CableslossesaboundNo ratings yet

- Project Report On TaxationDocument51 pagesProject Report On Taxationanuragmishra211276% (38)

- Income Tax CalculationDocument2 pagesIncome Tax CalculationSiddharth DasNo ratings yet

- VRLDocument164 pagesVRLGeebeeNo ratings yet

- WWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enDocument17 pagesWWW - Humanservices.gov - Au SPW Customer Forms Resources Modjy-1211enLeslie BrownNo ratings yet

- MS 27dec09Document6 pagesMS 27dec09Richa ShrivasravaNo ratings yet

- Cosmos International LTD.: Personal Particulars FormDocument4 pagesCosmos International LTD.: Personal Particulars FormMonu KashyapNo ratings yet

- 2018 Salary Guide: For Administrative ProfessionalsDocument29 pages2018 Salary Guide: For Administrative ProfessionalsMazen Al-RefaeiNo ratings yet

- Return of Organization Exempt From Income TaxDocument11 pagesReturn of Organization Exempt From Income TaxEnvironmental Working GroupNo ratings yet

- Draft - Withholding of Income Tax On Compensation and Other ConcernsDocument33 pagesDraft - Withholding of Income Tax On Compensation and Other Concernsgmangalo93% (14)

- ERP Evaluation TemplateDocument5 pagesERP Evaluation Templatejancukjancuk50% (2)

- Employees Perception Towards Compensatio PDFDocument71 pagesEmployees Perception Towards Compensatio PDFnihithNo ratings yet

- Paper 7 New Book 83 152 SalaryDocument70 pagesPaper 7 New Book 83 152 SalaryHridya PrasadNo ratings yet

- Human Resource Management of Four Season Hotels and ResortsDocument9 pagesHuman Resource Management of Four Season Hotels and Resortsleeagabu100% (1)

- Sick Vacation Leave Authorization LetterDocument3 pagesSick Vacation Leave Authorization LetterAd ElouNo ratings yet

- Fringe Benefit ExercisesDocument6 pagesFringe Benefit ExercisesGet BurnNo ratings yet

- Syed Zubair Ali Khan Offer LetterDocument3 pagesSyed Zubair Ali Khan Offer LetterExodia Switch2No ratings yet

- Employees' Rights Under The Malaysian Social Security OrganisationDocument21 pagesEmployees' Rights Under The Malaysian Social Security Organisationterry_lai_2No ratings yet

- Adam Smith's Canons of TaxationDocument23 pagesAdam Smith's Canons of TaxationPriscilla AdebolaNo ratings yet

- Us Dol Gina FaqsDocument5 pagesUs Dol Gina FaqsMolly DiBiancaNo ratings yet

- Benefits at A Glance: The Quick Benefits, Perks and Policies Guide To Being A Googler in IndiaDocument8 pagesBenefits at A Glance: The Quick Benefits, Perks and Policies Guide To Being A Googler in Indiashrutam100% (2)

- ECMDocument - BPP NOTES PDFDocument50 pagesECMDocument - BPP NOTES PDFpatriciadouceNo ratings yet

- Q.1) Define Human Resource Development? Roles Responsibility and Functions inDocument36 pagesQ.1) Define Human Resource Development? Roles Responsibility and Functions inkaramyi97% (31)

- MRC Employee Benefits UpdateDocument3 pagesMRC Employee Benefits UpdatenishantNo ratings yet

- State Investigative Report On UNTDocument5 pagesState Investigative Report On UNTThe Dallas Morning NewsNo ratings yet

- Income Tax Principles and Types in the PhilippinesDocument36 pagesIncome Tax Principles and Types in the PhilippinesPascua PeejayNo ratings yet

- HR Manager KPIDocument4 pagesHR Manager KPIAyman MotenNo ratings yet

- MCOM-I: Introduction to Life Insurance in IndiaDocument40 pagesMCOM-I: Introduction to Life Insurance in Indiakrittika03No ratings yet

- Income From Salaries - ProblemsDocument25 pagesIncome From Salaries - ProblemsAbishek SharmaNo ratings yet

- 2 - Establishing Strategic Pay PlansDocument13 pages2 - Establishing Strategic Pay PlansFaisal MalekNo ratings yet

- AIA SOLITAIRE PERSONAL ACCIDENTDocument16 pagesAIA SOLITAIRE PERSONAL ACCIDENTmailer68650% (2)