You might also like

- 16-029Document60 pages16-029govindmanianNo ratings yet

- Hints 170 FullDocument101 pagesHints 170 FullgovindmanianNo ratings yet

- Dynamicland 501c3 NarrativeDocument5 pagesDynamicland 501c3 NarrativegovindmanianNo ratings yet

- 05 01 AccDocument15 pages05 01 AccgovindmanianNo ratings yet

- The Design and Implementation of XiaoIce, An Empathetic Social ChatbotDocument26 pagesThe Design and Implementation of XiaoIce, An Empathetic Social ChatbotgovindmanianNo ratings yet

- Sounding Board: A User-Centric and Content-Driven Social ChatbotDocument5 pagesSounding Board: A User-Centric and Content-Driven Social ChatbotgovindmanianNo ratings yet

- Neural Approaches To Conversational AIDocument95 pagesNeural Approaches To Conversational AIgovindmanianNo ratings yet

- Evaluation Methods For Unsupervised Word EmbeddingsDocument10 pagesEvaluation Methods For Unsupervised Word Embeddingskatema9No ratings yet

- Sounding Board TalkDocument53 pagesSounding Board TalkgovindmanianNo ratings yet

- 2017 02 01-21 15 12-Simons-Nlp-TutorialDocument248 pages2017 02 01-21 15 12-Simons-Nlp-TutorialgovindmanianNo ratings yet

- Conceptual Pacts and Lexical Choice in Conversation: Susan E. Brennan Herbert H. ClarkDocument12 pagesConceptual Pacts and Lexical Choice in Conversation: Susan E. Brennan Herbert H. ClarkgovindmanianNo ratings yet

- History 2007Document8 pagesHistory 2007govindmanianNo ratings yet

- Evaluating The Stability of Embedding-Based Word SimilaritiesDocument14 pagesEvaluating The Stability of Embedding-Based Word SimilaritiesgovindmanianNo ratings yet

- Scott Page - Path Dependence EnssayDocument30 pagesScott Page - Path Dependence EnssayLuis Gonzalo Trigo SotoNo ratings yet

- American Economic AssociationDocument19 pagesAmerican Economic AssociationgovindmanianNo ratings yet

- Anthropology of CapitalismDocument6 pagesAnthropology of Capitalismgovindmanian100% (1)

- Annurev Soc 081715 074206 PDFDocument33 pagesAnnurev Soc 081715 074206 PDFgovindmanianNo ratings yet

- KurtzDocument22 pagesKurtzBoubaker JaziriNo ratings yet

- 0900 ChandosDocument18 pages0900 ChandosgovindmanianNo ratings yet

- NLP Analysis Provides Insights into Effective Counseling StrategiesDocument14 pagesNLP Analysis Provides Insights into Effective Counseling StrategiesgovindmanianNo ratings yet

- Ego Is The Enemy - Full BibliographyDocument17 pagesEgo Is The Enemy - Full Bibliographygovindmanian50% (2)

- History of Institutional Theory PDFDocument22 pagesHistory of Institutional Theory PDFgovindmanian0% (1)

- Annurev Soc 081715 074206Document33 pagesAnnurev Soc 081715 074206govindmanianNo ratings yet

- Physica A: Michael J. Bommarito II, Daniel Martin Katz, Jonathan L. Zelner, James H. FowlerDocument8 pagesPhysica A: Michael J. Bommarito II, Daniel Martin Katz, Jonathan L. Zelner, James H. FowlergovindmanianNo ratings yet

- EGO Is The ENEMY - Take Care of Yourself - Bonus ChapterDocument5 pagesEGO Is The ENEMY - Take Care of Yourself - Bonus ChaptergovindmanianNo ratings yet

- Pset 3Document3 pagesPset 3govindmanianNo ratings yet

- Fea Grothendieck Part2Document17 pagesFea Grothendieck Part2RemymainNo ratings yet

- Mumford AMS PDFDocument22 pagesMumford AMS PDFgovindmanianNo ratings yet

- Ajph 58 2 274Document15 pagesAjph 58 2 274govindmanianNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- A Project Report On NSEDocument49 pagesA Project Report On NSEViren SehgalNo ratings yet

- ACI Dealing Certificate New Version Syllabus 27 Jul 2020Document15 pagesACI Dealing Certificate New Version Syllabus 27 Jul 2020Oluwatobiloba OlayinkaNo ratings yet

- Tokyo Stock ExhangeDocument265 pagesTokyo Stock ExhangeAlexis Gonzalez PerezNo ratings yet

- Finolex Cables LTDDocument6 pagesFinolex Cables LTDAditiNo ratings yet

- Developing Securities Markets in Ethiopia: Prospects, ChallengesDocument16 pagesDeveloping Securities Markets in Ethiopia: Prospects, ChallengesSinshaw Bekele100% (10)

- E-Receipt: Transaction Reference Number: 658741278Document2 pagesE-Receipt: Transaction Reference Number: 658741278Sanoj MaveliNo ratings yet

- PIDM08042011 BrochureDocument6 pagesPIDM08042011 BrochureZakwan Hensem ZainNo ratings yet

- Fibonacci Tool - How To UseDocument6 pagesFibonacci Tool - How To UseSaurabh DuaNo ratings yet

- Ep. 7 Pagpapalago NG PeraDocument2 pagesEp. 7 Pagpapalago NG PerakchnewmediaNo ratings yet

- Economic Calendar Economic CalendarDocument6 pagesEconomic Calendar Economic CalendarAtulNo ratings yet

- Level III - Mnemonics - Acronyms - AnalystForum PDFDocument5 pagesLevel III - Mnemonics - Acronyms - AnalystForum PDFAnonymous jjwWoxKheGNo ratings yet

- Case Studies: Smyth Barry and Company First National BankDocument3 pagesCase Studies: Smyth Barry and Company First National BankMarlene RegaladoNo ratings yet

- Marginal CostingDocument17 pagesMarginal CostingsubhaniaqheelNo ratings yet

- Bionic Turtle FRM Practice Questions P1.T3. Financial Markets and Products Chapter 3. Fund ManagementDocument9 pagesBionic Turtle FRM Practice Questions P1.T3. Financial Markets and Products Chapter 3. Fund ManagementChristian Rey Magtibay100% (1)

- Depriciation and AccountingDocument3 pagesDepriciation and AccountingGurkirat TiwanaNo ratings yet

- Assignment RathnayakeDocument3 pagesAssignment RathnayakePrasanna WickramasekaraNo ratings yet

- Demonetisation 422Document14 pagesDemonetisation 422swethabonthula vsNo ratings yet

- Country Currency ISO CodeDocument8 pagesCountry Currency ISO CodeSrinivasa Rao GangineniNo ratings yet

- 5 Minute Scalping SystemDocument10 pages5 Minute Scalping SystemEko Gatot IriantoNo ratings yet

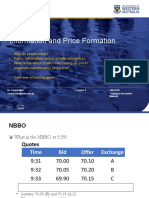

- Information and Price FormationDocument36 pagesInformation and Price FormationDylan AdrianNo ratings yet

- Capital Market - Chap 1Document3 pagesCapital Market - Chap 1Abc AudreyNo ratings yet

- Alphaex Capital Candlestick Pattern Cheat Sheet InfographDocument1 pageAlphaex Capital Candlestick Pattern Cheat Sheet InfographvinuthaNo ratings yet

- Portfolio Analysis and Zero-Beta CAPM Under Heterogenous BeliefsDocument32 pagesPortfolio Analysis and Zero-Beta CAPM Under Heterogenous BeliefsvesralNo ratings yet

- Behavioral FinanceDocument7 pagesBehavioral FinanceErfan KhanNo ratings yet

- Profiting With Ichimoku CloudsDocument46 pagesProfiting With Ichimoku Cloudsram100% (2)

- Syllabus International FinanceDocument1 pageSyllabus International FinanceRabin JoshiNo ratings yet

- W.D Gann RRR TechnicqueDocument28 pagesW.D Gann RRR TechnicqueYatharth Dass0% (1)

- Unit 4 Derivatives Part 1Document19 pagesUnit 4 Derivatives Part 1UnathiNo ratings yet

- Cards Schedule ChargesDocument1 pageCards Schedule ChargesRaju ReddyNo ratings yet

- Introduction to Derivatives Markets 232DDocument356 pagesIntroduction to Derivatives Markets 232DRewa ShankarNo ratings yet