You might also like

- Notes On Inventory ValuationDocument7 pagesNotes On Inventory ValuationNouman Mujahid100% (2)

- Assignment On DepreciationDocument4 pagesAssignment On DepreciationNouman MujahidNo ratings yet

- Depreciation and Carrying AmountDocument12 pagesDepreciation and Carrying AmountNouman MujahidNo ratings yet

- Notes On Working Capital ManagementDocument11 pagesNotes On Working Capital ManagementNouman MujahidNo ratings yet

- Dividends: Factors Affecting Dividend PolicyDocument7 pagesDividends: Factors Affecting Dividend PolicyNouman MujahidNo ratings yet

- Merger: Acquiring CompanyDocument3 pagesMerger: Acquiring CompanyNouman MujahidNo ratings yet

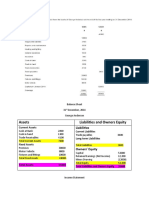

- Assets Liabilities and Owners EquityDocument9 pagesAssets Liabilities and Owners EquityNouman MujahidNo ratings yet

- Accounts Payable ManagementDocument3 pagesAccounts Payable ManagementNouman MujahidNo ratings yet

- Quiz of DividendDocument1 pageQuiz of DividendNouman Mujahid0% (1)

- Averageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Document1 pageAverageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Nouman MujahidNo ratings yet

- What Is Behavioral FinanceDocument4 pagesWhat Is Behavioral FinanceNouman MujahidNo ratings yet

- Breakeven Analysis: EBIT $0Document5 pagesBreakeven Analysis: EBIT $0Nouman MujahidNo ratings yet

- Ebit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCDocument6 pagesEbit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCNouman MujahidNo ratings yet

- Bahvioral FinanceDocument14 pagesBahvioral FinanceNouman MujahidNo ratings yet

- How To Write Effective Introduction of An ArticleDocument14 pagesHow To Write Effective Introduction of An ArticleNouman MujahidNo ratings yet

- Madina Medical StoreDocument29 pagesMadina Medical StoreNouman MujahidNo ratings yet

- Finance Interview Questions: Carey CompassDocument2 pagesFinance Interview Questions: Carey CompassNouman MujahidNo ratings yet

- Initial Cash FlowDocument3 pagesInitial Cash FlowNouman Mujahid50% (2)

- Gupta Macroeconomic (2013)Document22 pagesGupta Macroeconomic (2013)Nouman MujahidNo ratings yet

- Beta Levered and UnleveredDocument3 pagesBeta Levered and UnleveredNouman MujahidNo ratings yet

- Org 4Document34 pagesOrg 4Nouman MujahidNo ratings yet

- Cross - Iyears Companbs BI Dualitman - O Roa ROE SizeDocument8 pagesCross - Iyears Companbs BI Dualitman - O Roa ROE SizeNouman MujahidNo ratings yet

- Arbitrage Pricing TheoryDocument5 pagesArbitrage Pricing TheoryNouman MujahidNo ratings yet

- Bundling Human Capital With Organizational Context: The Impact of International Assignment Experience On Multinational Firm Performance and Ceo PayDocument20 pagesBundling Human Capital With Organizational Context: The Impact of International Assignment Experience On Multinational Firm Performance and Ceo PayNouman MujahidNo ratings yet

- Corporate Performance and Stakeholder Management: Balancing Shareholder and Customer Interests in The U.K. Privatized Water IndustryDocument14 pagesCorporate Performance and Stakeholder Management: Balancing Shareholder and Customer Interests in The U.K. Privatized Water IndustryNouman MujahidNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Pronoun and Antecedent AgreementDocument31 pagesPronoun and Antecedent AgreementJC Chavez100% (1)

- PHD Thesis On Development EconomicsDocument6 pagesPHD Thesis On Development Economicsleslylockwoodpasadena100% (2)

- Kristine Jane T. Zipagan Assignment: 1. Parts of InfographicsDocument2 pagesKristine Jane T. Zipagan Assignment: 1. Parts of InfographicsChristyNo ratings yet

- Latest DLL Math 4 WK 8Document2 pagesLatest DLL Math 4 WK 8Sheryl David PanganNo ratings yet

- Practical Research I - Stem 11 EditedDocument22 pagesPractical Research I - Stem 11 EditedRenzo MellizaNo ratings yet

- 01 - Welcome To ML4TDocument15 pages01 - Welcome To ML4Themant kurmiNo ratings yet

- Mass Culture - Mass CommunicationDocument54 pagesMass Culture - Mass Communicationatomyk_kyttenNo ratings yet

- Gayong - Gayong Sur, City of Ilagan, Isabela Senior High SchoolDocument6 pagesGayong - Gayong Sur, City of Ilagan, Isabela Senior High SchoolRS Dulay100% (1)

- Session 1 - Nature of ReadingDocument9 pagesSession 1 - Nature of ReadingAřčhäńgël Käśtïel100% (2)

- Confrontation MeetingDocument5 pagesConfrontation MeetingcalligullaNo ratings yet

- Lester Choi'sDocument1 pageLester Choi'sca5lester12No ratings yet

- Personality TheoriesDocument10 pagesPersonality Theorieskebede desalegnNo ratings yet

- English 1112E: Technical Report Writing: Gefen Bar-On Santor Carmela Coccimiglio Kja IsaacsonDocument69 pagesEnglish 1112E: Technical Report Writing: Gefen Bar-On Santor Carmela Coccimiglio Kja IsaacsonRem HniangNo ratings yet

- Guía de Aprendizaje: English Level 5Document10 pagesGuía de Aprendizaje: English Level 5Christian PardoNo ratings yet

- Action Plan in English ResDocument3 pagesAction Plan in English ResKarmela VeluzNo ratings yet

- Sagot Sa What's More NG Oral ComDocument2 pagesSagot Sa What's More NG Oral ComMhariane MabborangNo ratings yet

- Grade 4 Q2 2022-2023 Budgeted Lesson MAPEH 4 - MGA - 1Document8 pagesGrade 4 Q2 2022-2023 Budgeted Lesson MAPEH 4 - MGA - 1Dian G. MateoNo ratings yet

- Lesson Plan Beowulf Prelude-Ch 2Document2 pagesLesson Plan Beowulf Prelude-Ch 2api-381150267No ratings yet

- Clarifying The Research Question Through Secondary Data and ExplorationDocument33 pagesClarifying The Research Question Through Secondary Data and ExplorationSyed MunawarNo ratings yet

- Practical Research 1 11 q2 m1Document14 pagesPractical Research 1 11 q2 m1Kaye Flores100% (1)

- DLL For CotDocument3 pagesDLL For CotLeizel Jane Lj100% (2)

- Behavioural Event InterviewDocument12 pagesBehavioural Event Interviewwgcdrvenky100% (1)

- Q1 - Performance Task No. 1Document1 pageQ1 - Performance Task No. 1keanguidesNo ratings yet

- Employability SkillsDocument19 pagesEmployability SkillsRonaldo HertezNo ratings yet

- 2nd Lesson 1 Types of Speeches and Speech StyleDocument23 pages2nd Lesson 1 Types of Speeches and Speech Styletzuyu lomlNo ratings yet

- Silabus: Jurusan Pendidikan Bahasa InggrisDocument3 pagesSilabus: Jurusan Pendidikan Bahasa InggrisRusdin SurflakeyNo ratings yet

- Universiti Teknologi Mara Final Examination: Course Organizational Behaviour SMG501 JUNE 2018 3 HoursDocument3 pagesUniversiti Teknologi Mara Final Examination: Course Organizational Behaviour SMG501 JUNE 2018 3 HoursMohd AlzairuddinNo ratings yet

- PSYCH 101 Motivation, Values and Purpose AssignDocument4 pagesPSYCH 101 Motivation, Values and Purpose AssignLINDA HAVENSNo ratings yet

- Answers Handout 3Document2 pagesAnswers Handout 3Дианка МотыкаNo ratings yet

- Design Thinking Toolkit PDFDocument32 pagesDesign Thinking Toolkit PDFDaniela DumulescuNo ratings yet