You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 12 Angry Men AnalysisDocument9 pages12 Angry Men AnalysisShubhpreet Singh100% (1)

- SARFAESI Act in Layman WordsDocument2 pagesSARFAESI Act in Layman WordsAsim Javed100% (1)

- Jpqr9l104xgdt5lvxacedw IV GP PyslpDocument1 pageJpqr9l104xgdt5lvxacedw IV GP PyslpAsim JavedNo ratings yet

- Manual GPS Trimble Portugues CFX-750 / FM-750Document246 pagesManual GPS Trimble Portugues CFX-750 / FM-750José Luis Mailkut Pires100% (5)

- Lipoproteins in Diabetes Mellitus: Alicia J. Jenkins Peter P. Toth Timothy J. Lyons EditorsDocument468 pagesLipoproteins in Diabetes Mellitus: Alicia J. Jenkins Peter P. Toth Timothy J. Lyons EditorsFELELNo ratings yet

- Doanh Nghiep Viet Nam Quang CaoDocument1 pageDoanh Nghiep Viet Nam Quang Caodoanhnghiep100% (1)

- Saif Ullah Khan: ObjectiveDocument3 pagesSaif Ullah Khan: ObjectiveAsim JavedNo ratings yet

- Ordinary PostDocument1 pageOrdinary PostAsim JavedNo ratings yet

- Form 1 PDFDocument1 pageForm 1 PDFAsim JavedNo ratings yet

- ) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GDocument1 page) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GAsim JavedNo ratings yet

- AS400 Job Scheduler PDFDocument183 pagesAS400 Job Scheduler PDFAsim JavedNo ratings yet

- Resume - CA7 SchedulerDocument5 pagesResume - CA7 SchedulerAsim JavedNo ratings yet

- Microsoft Word - Practice Paper Advanced Auditing Mock Test November 2016Document4 pagesMicrosoft Word - Practice Paper Advanced Auditing Mock Test November 2016Asim JavedNo ratings yet

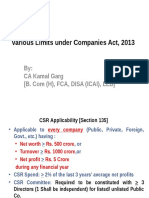

- Various Limits Under Companies Act, 2013 (CA Final)Document61 pagesVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedNo ratings yet

- FEMA Notes Comprehensive Summary For November 2016Document7 pagesFEMA Notes Comprehensive Summary For November 2016Asim JavedNo ratings yet

- Important Company Law Case Laws ListDocument3 pagesImportant Company Law Case Laws ListAsim JavedNo ratings yet

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDocument2 pagesNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNo ratings yet

- Annual 2005Document128 pagesAnnual 2005KarredeLeonNo ratings yet

- Pechay Camote Buchi - Aug7Document36 pagesPechay Camote Buchi - Aug7Rockie Alibio JuanicoNo ratings yet

- Old Book Buy or SellDocument41 pagesOld Book Buy or SellPallavi Pallu50% (4)

- QinQ Configuration PDFDocument76 pagesQinQ Configuration PDF_kochalo_100% (1)

- Birhane, E. 2014. Agroforestry Governance in Ethiopa Report WP 5Document50 pagesBirhane, E. 2014. Agroforestry Governance in Ethiopa Report WP 5woubshetNo ratings yet

- Farewell Address WorksheetDocument3 pagesFarewell Address Worksheetapi-261464658No ratings yet

- EARTH SCIENCE NotesDocument8 pagesEARTH SCIENCE NotesAlthea Zen AyengNo ratings yet

- Fruit LeathersDocument4 pagesFruit LeathersAmmon FelixNo ratings yet

- RJSC - Form VII PDFDocument4 pagesRJSC - Form VII PDFKamruzzaman SheikhNo ratings yet

- ERF 2019 0128 H160 Noise CertificationDocument10 pagesERF 2019 0128 H160 Noise CertificationHelimanualNo ratings yet

- DS ClozapineDocument3 pagesDS ClozapineMiggsNo ratings yet

- Car Radiator AssignmentDocument25 pagesCar Radiator AssignmentKamran ZafarNo ratings yet

- BA 238. Berita Acara XCMGDocument3 pagesBA 238. Berita Acara XCMGRizkiRamadhanNo ratings yet

- Out To Lunch: © This Worksheet Is FromDocument1 pageOut To Lunch: © This Worksheet Is FromResian Garalde BiscoNo ratings yet

- Student's Lab Pack: Preteens 02 11 Weeks CourseDocument30 pagesStudent's Lab Pack: Preteens 02 11 Weeks CourseMi KaNo ratings yet

- Missions ETC 2020 SchemesOfWarDocument10 pagesMissions ETC 2020 SchemesOfWarDanieleBisignanoNo ratings yet

- Students' Rights: Atty. Mabelyn A. Palukpok Commission On Human Rights-CarDocument15 pagesStudents' Rights: Atty. Mabelyn A. Palukpok Commission On Human Rights-Cardhuno teeNo ratings yet

- IHE ITI Suppl XDS Metadata UpdateDocument76 pagesIHE ITI Suppl XDS Metadata UpdateamNo ratings yet

- Lecture 1. Introducing Second Language AcquisitionDocument18 pagesLecture 1. Introducing Second Language AcquisitionДиляра КаримоваNo ratings yet

- The SPIN Model CheckerDocument45 pagesThe SPIN Model CheckerchaitucvsNo ratings yet

- City Marketing: Pengelolaan Kota Dan WilayahDocument21 pagesCity Marketing: Pengelolaan Kota Dan WilayahDwi RahmawatiNo ratings yet

- 1416490317Document2 pages1416490317Anonymous sRkitXNo ratings yet

- 2-Port Antenna Frequency Range Dual Polarization HPBW Adjust. Electr. DTDocument5 pages2-Port Antenna Frequency Range Dual Polarization HPBW Adjust. Electr. DTIbrahim JaberNo ratings yet

- Case DigestsDocument12 pagesCase DigestsHusni B. SaripNo ratings yet

- James Burt HistoryDocument9 pagesJames Burt HistoryJan GarbettNo ratings yet