You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MNO Financial Policies and Procedures Updated 2021Document61 pagesMNO Financial Policies and Procedures Updated 2021Mohamed ElbariNo ratings yet

- Chase Bank Statement BankStatements - Net JulyDocument4 pagesChase Bank Statement BankStatements - Net JulyJoe SF0% (1)

- Government AccountingDocument17 pagesGovernment AccountingMC ExtNo ratings yet

- Ang Tek Lian Vs CADocument2 pagesAng Tek Lian Vs CALee Somar100% (1)

- Araneta V PaternoDocument5 pagesAraneta V PaternopurplebasketNo ratings yet

- Chapter 3 Accounting For Revenue Other ReceiptsDocument15 pagesChapter 3 Accounting For Revenue Other ReceiptsSuzanne SenadreNo ratings yet

- Osds Position and Competency ProfileDocument45 pagesOsds Position and Competency ProfileAnnaliza Garcia Esperanza100% (1)

- FIN WI 001 Image Marked PDFDocument10 pagesFIN WI 001 Image Marked PDFGregurius DaniswaraNo ratings yet

- Auditing and Assurance Test Bank PDFDocument35 pagesAuditing and Assurance Test Bank PDFWhinalindo L. Benologa100% (1)

- 1.cebu International V. Ca 316 SCRA 488Document9 pages1.cebu International V. Ca 316 SCRA 488Rhena SaranzaNo ratings yet

- Working Capital Finance Trade Credit, Bank Finance and Commercial PaperDocument105 pagesWorking Capital Finance Trade Credit, Bank Finance and Commercial PaperNishkushNo ratings yet

- Chapter 3 MCQDocument4 pagesChapter 3 MCQLương Vân Trang50% (2)

- Sweden - How Cash Became More Trouble Than It's Worth - Upper IntermediateDocument5 pagesSweden - How Cash Became More Trouble Than It's Worth - Upper Intermediatec_a_tabetNo ratings yet

- ICT IGCSE Theory - Revision Presentation: 2015 - 2016 Questions (New Syllabus)Document13 pagesICT IGCSE Theory - Revision Presentation: 2015 - 2016 Questions (New Syllabus)Aditya ShindeNo ratings yet

- As Man Engine PartsDocument2 pagesAs Man Engine PartsRAVEENDRA OFFICENo ratings yet

- Shaping The ICT Banking Inovations For The FutureDocument27 pagesShaping The ICT Banking Inovations For The FutureK T A Priam KasturiratnaNo ratings yet

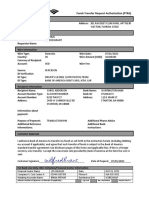

- Funds Transfer Request AuthorizationDocument1 pageFunds Transfer Request AuthorizationSaqib RodriguezNo ratings yet

- Bank Cashier ResponsibilitiesDocument5 pagesBank Cashier ResponsibilitiesG.Amarnath ReddyNo ratings yet

- Lecture Notes On Bank Reconciliation - 000Document3 pagesLecture Notes On Bank Reconciliation - 000judel ArielNo ratings yet

- Treasury Pay-In-Slip SB Form No 4Document2 pagesTreasury Pay-In-Slip SB Form No 4Rose KatharineNo ratings yet

- Audit of Acquisition and Payment Cycle PDFDocument36 pagesAudit of Acquisition and Payment Cycle PDFZi VillarNo ratings yet

- ForeclosureDocument3 pagesForeclosuremohammadafreed223No ratings yet

- Books of Prime Entry NotesDocument25 pagesBooks of Prime Entry NotesNur AiniNo ratings yet

- IOCL Tender - Spent CatalystDocument25 pagesIOCL Tender - Spent CatalystShailendra UpadhyayNo ratings yet

- CT Cre MemoDocument20 pagesCT Cre MemoChetan MitraNo ratings yet

- Multiple Choice Questions ITDocument3 pagesMultiple Choice Questions ITKim CarpioNo ratings yet

- Cash Management of HSBC Bank: Integrated Payment SolutionsDocument12 pagesCash Management of HSBC Bank: Integrated Payment SolutionsSatish Singh ॐNo ratings yet

- Program On Finacle 10Document95 pagesProgram On Finacle 10Mudit100% (1)

- My - Bill - 21 May, 2023 - 20 Jun, 2023Document10 pagesMy - Bill - 21 May, 2023 - 20 Jun, 2023Mohak JainNo ratings yet