Professional Documents

Culture Documents

Industrial Enterprises of America (IEAM) First Amended Disclosure Statement

Uploaded by

ValueSearcher70Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Industrial Enterprises of America (IEAM) First Amended Disclosure Statement

Uploaded by

ValueSearcher70Copyright:

Available Formats

IN THE UNITED STATES BANKRUPTCY COURT

FOR THE DISTRICT OF DELAWARE

In re: ) CHAPTER 11

)

PITT PENN HOLDING CO., INC., et al.1, ) Case No. 09-11475 (BLS)

) (Jointly Administered)

Debtors. )

)

Important Dates

Date by which ballots must be received: _________________, 2010

Date by which objections to confirmation of the _________________, 2010

plan must be filed and served:

Hearing on confirmation of the Plan: _________________, 2010

DEBTORS’ FIRST AMENDED DISCLOSURE STATEMENT

DATED: May 26, 2010

Christopher D. Loizides (No. 3968)

LOIZIDES, P.A.

1225 King Street, Suite 800

Wilmington, DE 19801

Telephone: (302) 654-0248

Facsimile: (302) 654-0728

E-mail: loizides@loizides.com

- and -

Pace Reich

Benjamin Reich

PACE REICH, PC

726 Meetinghouse Road

Elkins Park, PA 19027

Telephone: (215) 790-0100

Facsimile: (215) 790-7360

Email: pacereichpc@msn.com

Counsel for Debtors

1

The debtors are: Pitt Penn Holding Co. (Case No. 09-11475), Pitt Penn Oil Co. LLC (Case No. 09-11476), Industrial

Enterprises of America, Inc. (Case No. 09-11508), EMC Packaging, Inc. (Case No. 09-11524), Today’s Way

Manufacturing LLC (Case No. 09-11586), and Unifide Industries LLC (Case No. 09-11587), all of which have been jointly

administered.

FIRST AMENDED DISCLOSURE STATEMENT

TABLE OF CONTENTS

[TABLE OF CONTENTS HAS NOT BEEN CONFORMED TO REFLECT PROPOSED REVISIONS]

I. INTRODUCTION .............................................................................................................................................. 1

II. PURPOSE OF THE DISCLOSURE STATEMENT AND PROVISIONS FOR VOTING AND

CONFIRMATION ...................................................................................................................... 1

A. Purpose ................................................................................................................................................ 1

B. Voting Provisions ................................................................................................................................ 2

1. General ................................................................................................................................... 2

2. Claimants Not Entitled to Vote .............................................................................................. 2

a. Administrative and Priority Tax Claims .................................................................. 2

b. Unimpaired Claims .................................................................................................. 3

3. Claimants Entitled to Vote; Impaired Claims ........................................................................ 3

4. Acceptance of the Plan ........................................................................................................... 3

C. Confirmation ........................................................................................................................................ 4

1. Objections .............................................................................................................................. 4

2. Confirmation by Acceptance.................................................................................................. 4

3. Confirmation Without Acceptance......................................................................................... 4

D. Representation Limited ....................................................................................................................... 5

III. INQUIRIES ...................................................................................................................................................... 5

IV. THE DEBTORS ............................................................................................................................................... 5

A. Pre-Petition Background and History .................................................................................................. 6

B. Background – Formation and Maintenance of Corporate Records ...................................................... 6

C. Acquisitions ......................................................................................................................................... 8

D. Private Placements - July 2005 through March 2006 .......................................................................... 9

E. John D. Mazzuto’s Personal Bankruptcy is Disclosed to the Board .................................................. 11

F. Indecent Disclosure: The Use of Press Releases, Investor Meetings, and “Promoters” .................... 12

G. February 2008 - John D. Mazzuto Resigns and James W. Margulies Becomes CEO and CFO ....... 15

H. April 2008 - Mr. Margulies Discusses the Company’s Cash Requirements with a Number of

Significant Investors ................................................................................................... 15

I. April 2009 - All Prior Financials, Stock Issuances, and Disclosures Are Under Review By

Current Management .................................................................................................. 16

1. The Chaotic State of the Corporate Records Has Created a Major Problem for

New Management ......................................................................................... 17

2. State of IEAM Accounting Books and Records ................................................................... 18

3. Class Action Lawsuit and SEC Inquiries Result in the Formation of a Governance

Committee - October 2008 ........................................................................... 21

4. Capital Structure .................................................................................................................. 22

5. Government Regulation ....................................................................................................... 37

6. Employees ............................................................................................................................ 37

J. Events that Lead to the Bankruptcy Filing.......................................................................................... 38

1. Litigation .............................................................................................................................. 41

a. Zyskind Action....................................................................................................... 41

b. Goldknopf Action .................................................................................................. 41

c. Margulis Action ..................................................................................................... 42

2. Contested Litigation ............................................................................................................. 42

a. Trinity Bui Action .................................................................................................. 42

b. Black Nickel Actions ............................................................................................. 42

c. EMC New Jersey Litigation ................................................................................... 43

d. Securities Class Action .......................................................................................... 43

e. Bankruptcy Litigation ............................................................................................ 44

3. Cooperation with Regulatory Authority/Law Enforcement ................................................. 44

K. Chapter 11 Cases ............................................................................................................................... 45

1. Initial Events in Bankruptcy................................................................................................. 45

2. Events Occurring in the Bankruptcy Case – DIP Financing, Avoiding

Conversion, Plan Filing .................................................................. 45

a. Bankruptcy Litigation ............................................................................................ 45

V. THE PLAN OF REORGANIZATION ........................................................................................................... 47

A. Plan Summary ................................................................................................................................... 47

FIRST AMENDED DISCLOSURE STATEMENT i

1.

Class A – Claims of Professionals ....................................................................................... 48

2.

Other Administrative Claims ............................................................................................... 48

3.

Class B ................................................................................................................................. 48

4.

Classes C, D, and E .............................................................................................................. 48

5.

Class F .................................................................................................................................. 48

6.

Class G – the Debtor-in-Possession Loan by Omtammot LLC............................................ 49

7.

Class H ................................................................................................................................. 49

8.

Class I – Shareholders Equity .............................................................................................. 50

9.

Class K – Any Claim for Damages for the Purchase or Sale of Any of the Securities

of Any of the Debtors ................................................................................... 50

B. General Provision Applicable to All Classes ..................................................................................... 50

C. Treatment of Contested Claims Arising Under Section 502(c) ......................................................... 50

VI. PAYMENTS UNDER THE PLAN .............................................................................................................. 51

A. Transfers of the Stock ........................................................................................................................ 52

B. Ownership of Shares After Distribution Under the Plan ................................................................... 52

VII. REJECTION AND ASSUMPTION OF EXECUTORY CONTRACTS AND UNEXPIRED LEASES .... 52

VIII. ALLOWED AMOUNT OF CLAIMS .......................................................................................................... 52

IX. VOIDABLE TRANSFERS .......................................................................................................................... 53

X. TAX CONSEQUENCES .............................................................................................................................. 53

XI. DISCHARGE OF DEBTOR ........................................................................................................................ 53

XII. JURISDICTION OF BANKRUPTCY COURT AFTER CONFIRMATION ............................................. 53

XIII. LIQUIDATION ANALYSIS AND DISCUSSION...................................................................................... 53

A. Liquidation Analysis/Miscellaneous Bankruptcy Provisions ............................................................ 54

XIV. OPERATING PROJECTIONS .................................................................................................................... 56

XV. CONCLUSION ............................................................................................................................................. 56

FIRST AMENDED DISCLOSURE STATEMENT ii

Industrial Enterprises of America, Inc., (“IEAM” or “the Company”), Pitt Penn Holding

Co., Inc, (“PPH”), Pitt Penn Oil Co., LLC, (“PPO”), EMC Packaging, Inc., (“EMC”), Today’s

Way Manufacturing LLC, (“Today’s Way”), and Unifide Industries LLC, (“Unifide”)

collectively the debtors in possession (the "Debtors"), submit this First Amended Disclosure

Statement (the "Disclosure Statement") in connection with the Debtors’ First Amended

Consolidated Plan of Reorganization (the "Plan"), pursuant to Chapter 11 of Title 11 of the

United States Code (the "Bankruptcy Code"). Capitalized terms used and not otherwise defined

herein shall have the same meanings as are ascribed to them in the Plan.

I. INTRODUCTION.

On April 30, 2009 through May 6, 2009 (the "Petition Dates"), the Debtors filed with the

United States Bankruptcy Court for the District of Delaware (the "Bankruptcy Court") Voluntary

Petitions (the "Petitions") under Chapter 11 of the Bankruptcy Code. Since the Petition Dates,

the Debtors have continued in the management and limited operation of their property as debtors

in possession pursuant to sections 1107 and 1108 of the Bankruptcy Code.

II. PURPOSE OF THE DISCLOSURE STATEMENT AND PROVISIONS FOR

VOTING AND CONFIRMATION.

A. Purpose.

The Debtors provide this Disclosure Statement, pursuant to the requirements of

section 1125 of the Bankruptcy Code, in order to provide to the holders of all Claims against and

Interests in the Debtors adequate information about the Debtors and the Plan, so that they may

make an informed judgment with respect to the merits of the Plan for purposes of voting on the

Plan. By Order dated ____________, 2010, the Disclosure Statement was approved by the

Bankruptcy Court as containing "adequate information", which is defined in section 1125(a)(1)

of the Bankruptcy Code as "information of a kind, and in sufficient detail, as far as is reasonably

practical in light of the nature and history of the debtor and the condition of the debtor’s books

and records, including a discussion of the potential material Federal tax consequences of the plan

to the debtor, any successor to the debtor, and a hypothetical investor typical of the holders of

claims or interests in the case, that would enable a hypothetical reasonable investor, typical of

holders of the relevant class to make an informed judgment about the Plan . . . ." This Disclosure

Statement does not purport to be a complete description of the Plan, the financial status of the

Debtors, the applicable provisions of the Bankruptcy Code, or other matters that may be deemed

significant by certain creditors and parties-in-interest. This Disclosure Statement is an attempt to

set forth, in reasonable detail, information that will enable a creditor to make an informed

judgment with respect to the Plan for voting purposes. The Disclosure Statement necessarily

involves a series of compromises between "raw data", the legal language in documents or

statutes, and the considerations of readability and usefulness. For further information, you

should examine the Plan directly (a copy of which accompanies this Disclosure Statement),

and/or consult with your legal and financial advisors. The description of the Plan herein is

provided only as a summary and it is recommended that all creditors and parties-in-interest

review the Plan, the balance of this Disclosure Statement, and the other documents and

FIRST AMENDED DISCLOSURE STATEMENT 1

information referenced herein, in order to obtain more complete information. Approval by the

Bankruptcy Court of the Disclosure Statement does not constitute an approval of the Plan.

Other than as set forth in this Disclosure Statement, no representations concerning the

Debtors, their assets, their financial condition, management or future operations are authorized

by the Debtors. Any representations or inducements made to secure acceptance of the Plan other

than as contained in the Plan and described in this Disclosure Statement are not authorized by the

Debtors and accordingly should not be relied upon by the holder of any Claim or Interest in

reaching a decision whether or not to vote to accept or reject the Plan.

Enclosed with this Disclosure Statement are the following:

(1) a copy of the Plan;

(2) a ballot for accepting or rejecting the Plan (if applicable); and

(3) a copy of the Order of the Bankruptcy Court approving the Disclosure

Statement setting forth: the time period and the manner by which to vote

to accept or reject the Plan, the time period for objecting to Confirmation

of the Plan, and fixing the time for the hearing on the Confirmation of the

Plan.

B. Voting Provisions.

1. General.

Every holder of a Claim or Interest in an Impaired Class that is entitled to receive a

distribution under the Plan is entitled to vote to accept or reject the Plan. As such, all holders of

Claims or Interests in Classes C, D, E and F may vote on the Plan by filling out the enclosed

Ballot and mailing it to counsel for the Debtors.

2. Classes of Claims and Interests Not Entitled to Vote.

a. DIP Claims

Pursuant to the compromise and settlement between and among the

Debtors, OMTAMMOT, LLC and OMTAMMOT II, L.P., with respect to the DIP Loan Claims

(the “DIP Loan Settlement”), OMTAMMOT, LLC and OMTAMMOT II, L.P. (together, the

“DIP Lenders”) have agreed to accept the distributions set forth in Article 3.1 of the Plan in full

satisfaction, settlement, release and discharge of, and in exchange for, their Allowed DIP Loan

Claims, and to the extent that such distributions may be deemed inadequate to pay the Allowed

DIP Loan Claims in full, the DIP Lenders have further agreed to waive any resulting deficiency

Claim in accordance with the DIP Loan Settlement.

FIRST AMENDED DISCLOSURE STATEMENT 2

b. Administrative and Priority Tax Claims.

Claimants holding only Administrative Claims and/or Priority Tax Claims

are not entitled to vote on the Plan because Section 1123(a)(1) of the Bankruptcy Code does not

require that such Claims be designated in a Class and because the Plan provides for the payment

of such Claimants under terms which not only satisfy, but are more favorable to such Claimants

than the requirements set forth by Sections 1129(a)(9)(A) and (C) of the Bankruptcy Code.

c. Unimpaired Claims.

Claimants holding Claims in a Class which is not impaired (as discussed

below) are not entitled to vote on the Plan because pursuant to Section 1126 of the Bankruptcy

Code, a Class, and each Claimant in such Class, that is not impaired under the Plan is

conclusively presumed to have accepted the Plan. As a general matter, under Section 1124 of the

Bankruptcy Code, a class of claims is impaired unless the legal, equitable and contractual rights

of the claimants in such class are not altered by the Plan (with exception of certain rights of

claimants to receive accelerated payment of their claims and certain rights of a debtor to cure

defaults) or unless the plan provides, that, on the effective date, each claimant in such class shall

receive, on account of its claim, cash equal to the allowed amount of such claim.

Claimants in Classes A and B (as described below) are Unimpaired and,

therefore, are not entitled to vote on the Plan. Code.

d. Deemed Rejecting Class.

Holders of Impaired Non-IEAM Interests in Class G are deemed to reject

the Plan because such holders will not receive a distribution under the Plan on account of their

Interests. Interest holders in Class G are accordingly not entitled to vote on the Plan.

3. Claimants Entitled to Vote; Impaired Claims.

Certain classes are Impaired under the Plan and Claimants in such Classes, therefore, are

entitled to vote on the Plan. Claimants in Classes C, D, E and F are entitled to vote on the Plan

since such classes are impaired.

4. Acceptance of the Plan.

Please note that the Plan is deemed accepted by a Class of Claims or Interests when it is

approved by holders of Claims and Interests who hold at least two-thirds of the dollar amount,

and who comprise more than one-half in number of, the Allowed Claims or Interests of such

Class that actually vote. An abstention by a Claim or Interest holder will not count toward either

acceptance or rejection of the Plan.

The Debtors recommend that each holder of a Claim or Interest that is entitled to vote to

vote to ACCEPT the Plan. IN ORDER FOR YOUR VOTE TO COUNT, YOUR BALLOT

FIRST AMENDED DISCLOSURE STATEMENT 3

MUST BE COMPLETED AND RECEIVED AT THE ADDRESS STATED ON THE BALLOT

(WHICH IS ALSO SET FORTH BELOW) ON OR BEFORE , 2010:

Pace Reich, PC

726 Meetinghouse Road

Elkins Park, PA 19027

Even though a Claim or Interest holder may choose not to vote or may vote against the

Plan, such Claim or Interest holder will nevertheless be bound by the terms and treatment set

forth in the Plan if the Plan is accepted by the requisite majorities in each Class entitled to vote

and is confirmed by the Court. Allowance of a Claim or Interest for voting purposes does not

necessarily mean that the Claim or Interest will be Allowed for purposes of distribution under the

terms of the Plan. Any Claim or Interest to which an objection has been or will be filed will be

Allowed for purposes of distribution only after determination by the Court. Such determination

may be made after the Plan is Confirmed.

C. Confirmation.

1. Objections.

Should you have an objection to Confirmation of the Plan, it must be filed, in writing,

with the Bankruptcy Court and served on counsel for the Debtors, on or before , 2010.

A hearing to consider confirmation of the Plan will be held on , 2010,

beginning at ______ before the Honorable Brendan L. Shannon in the United States Bankruptcy

Court for the District of Delaware, 824 Market Street, 6th Floor, Courtroom 1, Wilmington,

Delaware 19801.

2. Confirmation by Acceptance.

The Debtors are seeking Confirmation of the Plan under Section 1129(a) of the

Bankruptcy Code. Confirmation under Section 1129(a) is dependent upon a finding of the

Bankruptcy Court that a number of requirements have been met. One of these requirements is

that each Impaired Class of Claims and Interests entitled to vote on the Plan must accept the

Plan. Accordingly, the Plan cannot be Confirmed under Section 1129(a) unless accepted by each

Impaired Class of Claims and Interests.

3. Confirmation Without Acceptance.

Under Section 1129(b)(1) of the Code, the Court may confirm the Plan even if it has not

been accepted by one or more Impaired Classes of Claims and Interests, provided that the Plan

does not discriminate unfairly and it is fair and equitable with respect to each Impaired Class of

Claims or Interests that has not accepted the Plan.

In order for the Plan to be fair and equitable with respect to an Impaired Class of Secured

Claims, Section 1129(b)(2)(A) of the Code requires that the Plan provide for each Claimant in

such Class: (a) to receive payments over time which, in the aggregate, total at least the Allowed

FIRST AMENDED DISCLOSURE STATEMENT 4

amount of such Claimant's Claim, and which have a present value, as of the Effective Date of the

Plan, at least equal to the value of such Claimant's interest in the Debtor's property encumbered

by such Claimant's lien(s); and (b) the Secured Claimant shall retain such lien(s) in order to

secure such payments.

In order for the Plan to be fair and equitable with respect to an Impaired Class of

Unsecured Claims, Section 1129(b)(2)(B) of the Code requires that the Plan provide either: (a)

that each Claimant in such Class shall receive on account of its Claim property which has a

present value, as of the Effective Date of the Plan, equal to the Allowed amount of such Claim or

(b) that no Claimant or holder of an Interest in the Debtor that is junior to the Claims of such

Impaired Class will receive or retain under the Plan any property on account of such junior

Claim or Interest.

In order for the Plan to be fair and equitable with respect to an Impaired Class of

Interests, Section 1129(b)(2)(C) of the Code requires that the Plan provide either: (a) that each

Interest holder in such Class shall receive on account of its Interest property which has a present

value, as of the Effective Date of the Plan, equal to the value of such Interest or the Allowed

amount of any fixed liquidation preference or redemption price to which the holder of such

Interest is entitled or (b) that no holder of an Interest in the Debtor that is junior to the Interests

of such Impaired Class will receive or retain under the Plan any property on account of such

junior Interest.

D. Representation Limited.

THE ACCURACY OF THE INFORMATION, PARTICULARLY FINANCIAL

INFORMATION, SUBMITTED WITH THIS DISCLOSURE STATEMENT IS DEPENDENT

UPON AN ACCOUNTING PERFORMED BY THE DEBTORS. FURTHER, THE

FINANCIAL INFORMATION SET FORTH HEREIN CONTAINS FINANCIAL

PROJECTIONS OF FUTURE PERFORMANCE THAT NECESSARILY RELY ON THE

OUTCOME OF MANY VARIABLES OVER WHICH THE DEBTORS HAVE NO

CONTROL, AND THUS THE ACCURACY OF SUCH PROJECTIONS CANNOT BE

GUARANTEED.

THESE FINANCIAL PROJECTIONS PRESENT, TO THE BEST OF THE DEBTORS’

KNOWLEDGE AND BELIEF AS OF THE DATE OF THIS DISCLOSURE STATEMENT,

GIVEN ONE OR MORE HYPOTHETICAL ASSUMPTIONS, EACH DEBTOR ENTITY'S

EXPECTED FINANCIAL POSITION, RESULTS OF OPERATIONS, AND CHANGES IN

FINANCIAL POSITION OVER CERTAIN PROJECTED TIME PERIODS. A FINANCIAL

PROJECTION IS SOMETIMES PREPARED TO PRESENT FOR EVALUATION ONE OR

MORE HYPOTHETICAL COURSES OF ACTION IN LIGHT OF DIFFERENT SETS OF

VARIABLES. A FINANCIAL PROJECTION IS BASED ON THE RESPONSIBLE PARTY'S

ASSUMPTIONS REFLECTING RESULTS IT EXPECTS WOULD OCCUR, GIVEN ONE OR

MORE HYPOTHETICAL CONDITIONS. A PROJECTION MAY CONTAIN A RANGE OF

POSSIBLE OUTCOMES THAT COULD OCCUR UNDER A SET OF GIVEN

ASSUMPTIONS AND VARIABLES.

FIRST AMENDED DISCLOSURE STATEMENT 5

WHILE EVERY EFFORT HAS BEEN MADE TO ENSURE THAT THE

ASSUMPTIONS ARE VALID AND THAT THE PROJECTIONS ARE AS ACCURATE AS

CAN BE MADE UNDER THE CIRCUMSTANCES, THE DEBTORS CANNOT

UNDERTAKE TO CERTIFY OR WARRANT THE ABSOLUTE ACCURACY OF THE

FINANCIAL PROJECTIONS.

III. INQUIRIES.

Inquiries by holders of Claims or Interests or other parties in interest in these chapter 11

cases may be directed to counsel for the Debtors, Pace Reich, Esquire, Pace Reich PC, 726

Meetinghouse Road, Elkins Park, PA 19027, (215) 887-0130 (telephone) and (215) 887-5617

(facsimile); or to Robert L. Renck, Jr., Industrial Enterprises of America, 116 West 23rd Street,

5th Floor, New York, NY 10011, (212) 851-8434 (telephone) and rlrenck@renck.com (e-mail).

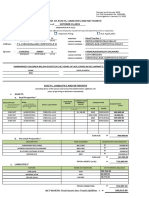

TREATMENT AND ESTIMATED DISTRIBUTIONS UNDER THE PLAN

The chart below summarizes the treatment of each class of claims and of unclassified

claims under the Plan. Please note, however:

The chart is only a general summary and the actual treatment of each class and of

unclassified claims is governed by the terms and provisions of the Plan.

The estimated allowed amounts in each category and the estimated percentage

recoveries are merely estimates. The actual amounts may vary considerable from

these estimates.

Debtors reserve the right, at any time provided for pursuant to bankruptcy law, to

object to any proof of claim which exceeds the amounts scheduled, in order to provide

a conservative picture, the Debtor has estimated the approximate amount of total

general unsecured claims to equal proximately $11,219,388.

CLASS TREATMENT ESTIMATED ESTIMATED

ALLOWED PERCENTAGE

AMOUNT RECOVERY

Unclassified DIP Pursuant to the DIP Loan Settlement, on $1,800,000.00 100%

Loan Claims or before the Effective Date, each holder

of an Allowed DIP Loan Claim shall

(Non-Voting) receive in full satisfaction, settlement,

release and discharge of, and in exchange

for, its Allowed DIP Loan Claim an

amount of Preferred A Shares of

Reorganized IEAM (the “Preferred A

Shares”) equal to one (1) Preferred A

Share for each one dollar ($1.00) of

Allowed DIP Loan Claims. Each

Preferred A Share shall accrue interest at

FIRST AMENDED DISCLOSURE STATEMENT 6

a rate of seven percent (7%) per annum

from the Effective Date until payment,

and such interest shall accrue and shall

only be payable upon payment via the

liquidation preference outlined in the

succeeding sentence. The Preferred A

Shares shall have a liquidation preference

equal to one dollar ($1.00) for each

Preferred A Share plus all interest accrued

thereon from the Effective Date through

the date of payment. The Preferred A

Shares shall have a liquidation preference

over the Preferred B Shares of

Reorganized IEAM (the “Preferred B

Shares”), the Preferred C Shares of

Reorganized IEAM (the “Preferred C

Shares”) and any newly issued Common

Stock. The Preferred A Shares may be

convertible to additional shares of New

Common B Stock of Reorganized IEAM

(the “New Common B Stock”) (at a

conversion rate equal to 30 million Shares

of New B Common Stock divided by the

aggregate amount of issued Preferred A

Shares) at any time upon the sole

discretion of the holder of the Series A

Preferred Stock.

Unclassified Except to the extent that an Allowed $205,000.00 100%

Administrative Administrative Claim has been paid prior

Claims to the Effective Date, each holder of an

Allowed Administrative Claim shall

(Non-Voting) receive payment of the amount of such

Allowed Administrative Claim in Cash on

the Effective Date, or as soon as

reasonably practicable thereafter, or

immediately after entry of an order

approving an application therefor if after

the Effective Date, in full satisfaction,

settlement, release and discharge of, and

in exchange for, such Allowed

Administrative Claim.

Unclassified Except to the extent that an Allowed $385,968.00 100%

Priority Tax Priority Tax Claim has been paid prior to

Claims the Effective Date, each holder of an

Allowed Priority Tax Claim shall receive

(Non-Voting) in full satisfaction, settlement, release and

discharge of, and in exchange for, such

Allowed Priority Tax Claim, equal

monthly payments over a period of five

(5) years from the Effective Date in an

aggregate principal amount equal to the

FIRST AMENDED DISCLOSURE STATEMENT 7

face amount of such Allowed Priority Tax

Claim, with interest on the unpaid portion

thereof at the rate of interest determined

under applicable nonbankruptcy law as of

the calendar month in which the Plan is

confirmed.

Class A Except to the extent that an Allowed Non- $102,864.00 100%

Non-Tax Tax Priority Claim has been paid prior to

Priority Claims the Effective Date, each holder of an

Allowed Non-Tax Priority Claim shall

(Unimpaired, receive in full satisfaction, settlement,

Non-Voting) release and discharge of, and in exchange

for, such Allowed Non-Tax Priority

Claim, payment of the amount of such

Non-Tax Priority Claim in Cash on the

Effective Date or as soon as reasonably

practicable thereafter.

Class B On the Effective Date, or as soon as $160,000.00 100%

Convenience reasonably practicable thereafter, each

Claims holder of an Allowed Convenience Claim

shall receive in full satisfaction,

(Unimpaired, settlement, release and discharge of, and

Non-Voting) in exchange for, such Allowed

Convenience Claim, payment of the

amount of such Allowed Convenience

Claim in Cash.

Class C Pursuant to the terms of the Prepetition $2,200,000.00 47.8%

Prepetition Loan Settlement, on the Effective Date, or

Lender Secured as soon as reasonably practicable

Claims thereafter, the Prepetition Loan Collateral

shall be liquidated and all the proceeds

(Impaired, thereof shall be remitted to

Voting) OMTAMMOT, LLC in full satisfaction,

settlement, release and discharge of, and

in exchange for, the secured portion of the

Allowed Prepetition Lender Secured

Claims. The Allowed deficiency Claim

of OMTAMMOT, LLC shall be treated as

a Class D Claim.

Class D On the Effective Date, or as soon as $11,219,388 100%

General reasonably practicable thereafter, each

Unsecured holder of an Allowed General Unsecured

Claims Claim shall receive in full satisfaction,

settlement, release and discharge of, and

(Impaired, in exchange for, such Allowed General

Voting) Unsecured Claim:

(i) Cash in an amount equal to the

lesser of (A) two percent (2%) of the

amount of such Allowed General

FIRST AMENDED DISCLOSURE STATEMENT 8

Unsecured Claim or (B) $200,000.00 to

be distributed Pro Rata to the holders of

Class D Claims; plus

(ii) an amount of Preferred B Shares

to be issued on a Pro Rata basis equal to

the greater of (A) ninety-eight percent

(98%) of the amount of such Allowed

General Unsecured Claim or (B) the total

amount of all Allowed General Unsecured

Claims in Class D less $200,000.00. One

(1) Preferred B Share shall be issued on

account of each one dollar ($1.00) of

Allowed General Unsecured Claims. The

Preferred B Shares shall not accrue

interest or otherwise be convertible. The

Preferred B Shares shall have a

liquidation preference equal to one dollar

($1.00) for each Preferred B Share. The

Preferred B Shares shall have a

liquidation preference over the Preferred

C Shares and any newly issued Common

Stock. When the net cash balances of

Reorganized IEAM are equal to or greater

than the preference amounts of Preferred

A Shares and Preferred B Shares,

Reorganized IEAM may in its sole

discretion liquidate the Preferred B

Shares. In addition, the holders of

Preferred B Shares may require

Reorganized IEAM to liquidate the

Preferred B Shares.

Class E Existing The Existing IEAM Interests shall be $0.00 100%

IEAM Interests deemed cancelled and extinguished as of

the Effective Date. On, or as soon as

(Impaired, reasonably practicable after the Effective

Voting) Date, each holder of an Allowed Existing

IEAM Interest shall receive its Pro Rata

share of 30 million shares of New

Common B Stock, to be issued by

Reorganized IEAM.

Class F To the extent that monetary damages are $0.00 100%

Subordinated assessed against any of the Debtors

Claims arising from any claim for damages for

the purchase or sale of any securities of

(Impaired, any of the Debtors, and to the extent such

Voting) damages are not paid by any insurance, in

accordance with the provisions of 510(b)

of the Code, such monetary damages shall

treated by the issuance of Preferred C

Shares. One (1) Preferred C Share shall

FIRST AMENDED DISCLOSURE STATEMENT 9

be issued on account of each one dollar

($1.00) of Allowed Subordinated Claims.

The Preferred C Shares will not accrue

interest or otherwise be convertible;

however, the Preferred C Shares shall

have a liquidation preference over New

Common Shares of Reorganized IEAM.

Class G All Non-IEAM Interests shall be deemed n/a 0%

Non-IEAM cancelled and extinguished as of the

Interests Effective Date, and the holders of all

Non-IEAM Interests shall not receive or

(Impaired) retain any property or interest in property

under the Plan on account of such Non-

IEAM Interests.

IV. THE DEBTORS.

The current management of IEAM first became affiliated with the company’s

subsidiaries on September 12, 2008. Management’s access to corporate records of the parent,

IEAM, has been limited as a result of the refusal of certain members of prior management to turn

over books and records. Management is relying on public filings previously made with the

United States Securities and Exchange Commission and records that they have been given access

to or obtained by a document request through the use of the turnover motion in the Bankruptcy

Court. As such, certain disclosures may be subject to revision and current management cannot

be certain if they have received all of IEAM’s records.

A. Pre-Petition Background and History.

IEAM’s organizational history was last described in a Form 10-KSB Amendment 1-FY

2006, Filed December 28, 2007. That document disclosed the following:

• IEAM originally operated as a holding company with four (4) wholly owned

subsidiaries, Pitt Penn Holding Inc., a Delaware corporation ("PPH"), EMC

Packaging, Inc., a Delaware corporation ("EMC"), Unifide Industries Limited

Liability Company, a New Jersey limited liability company ("Unifide"), and

Todays Way Manufacturing, LLC, a New Jersey limited liability company

("Todays Way").

• PPH, through its wholly owned subsidiary Pitt Penn Oil Co., LLC, an Ohio

limited liability company (“Pitt Penn”), was a leading manufacturer, marketer and

seller of automotive chemicals and additives.

• EMC’s original business consisted of converting hydrofluorocarbon gases

(“HFC”) R134a and R152a into branded private label refrigerant and propellant

products.

FIRST AMENDED DISCLOSURE STATEMENT 10

• Unifide was a leading marketer and seller of automotive chemicals and additives.

• Todays Way manufactured and packaged the products which were sold by

Unifide.

B. Background – Formation and Maintenance of Corporate Records.

The Company was originally incorporated in the State of Florida on June 14, 1990 as

Mid-Way Medical Diagnostic Center, Inc. ("Mid-Way (Florida)"). Mid-Way (Florida) was

initially engaged in the business of seeking to establish and operate medical and diagnostic

centers. During 1991, Mid-Way (Florida) abandoned its efforts to engage in such business.

In December 1997, Mid-Way (Florida) effected a reorganization by merging Mid-Way

Acquisition Corp. (the “Merger Sub”), a wholly owned Nevada corporation created by Mid-Way

(Florida) solely for the purpose of merging with Ciro Jewelry, Inc. ("Ciro Jewelry (Delaware)"),

a Delaware corporation. By virtue of the merger, all of the assets, liabilities, and business of Ciro

Jewelry (Delaware) became the assets, liabilities, and business of the Merger Sub. As a result of

the merger, the Merger Sub changed its name to Ciro Jewelry, Inc. ("Ciro Jewelry"); the then-

current sole officer and director resigned as the sole officer and director of both the Company

and Ciro Jewelry and simultaneously appointed Murray Wilson as the sole director of each

entity.

In December 1997, Mid-Way (Florida) changed its name to Ciro International, Inc.

("Ciro"); at the same time, Ciro merged with Mid-Way Medical and Diagnostic Center, Inc., a

Nevada corporation, which was established solely for the purpose of changing the domicile of

the Company from the State of Florida to the State of Nevada.

On April 21, 2003, Ciro and Advanced Bio/Chem, Inc., a Texas corporation (“ABC

Texas”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) whereby a

wholly owned subsidiary of Ciro, Ciro Acquisition Corp., a Texas corporation (which was

inappropriately identified in the Merger Agreement as Advanced Bio/Chem Acquisition Corp.),

merged with and into ABC Texas in a tax free exchange of shares at which time ABC Texas

became a wholly owned subsidiary of Ciro (the "Merger").

Until June 2003, the Company existed primarily as a holding company, and accordingly,

the operations were those of the former operating subsidiary, Ciro Jewelry. Until late 2002, the

main source of income derived from the licensing of the “Ciro” name. Effective June 9, 2003,

the Company sold all of the issued and outstanding common stock of the wholly owned

subsidiary, Ciro Jewelry, to Merchant’s T&F, Inc. (“MT&F”). Following December 2002, Ciro

Jewelry became a “shell” corporation with no defined business purpose and began the process of

searching for a new line of business or a merger candidate.

In May 2004, the Company entered into an Asset Purchase Agreement (the “Power3

Agreement”) with Power3 Medical Products, Inc., a New York corporation ("Power3"), Steven

FIRST AMENDED DISCLOSURE STATEMENT 11

B. Rash and Ira Goldknopf (collectively, the "Shareholders") (the "Power3 Sale"). According to

the Company’s records, the sale to Power3 was approved by the shareholders voting by proxy.

The company’s name was changed to IEAM.

The corporate records of IEAM, the parent, had allegedly been maintained in at least two

locations, its former New York headquarters at 711 Third Avenue, New York, NY and at the law

offices of Margulies and Levinson LLP, 30100 Chagrin Blvd., Suite 250, Pepper Pike, OH

44124. Upon the February 2008 resignation of John D. Mazzuto, president and chief financial

officer, the records held at the New York office were packed and sent to the attention of R.

Daniel Redmond, President, PPO and Executive Vice President, IEAM.

With the departure of John D. Mazzuto in February 2008, IEAM’s functional corporate

headquarters shifted to the offices of Margulies and Levinson, 30100 Chagrin Blvd., Suite 250,

Pepper Pike OH 44124. At least two employees of IEAM and/or its subs have been domiciled

at that location. They included James W. Margulies and Steven W. Berger.

Upon investigation and review it appears that the vast majority of the corporate records

may have been under the custody and control of James W. Margulies, Esquire, who has acted in

various capacities at IEAM. His role was multifaceted. At one time or another, he acted as an

attorney for MC Industrial (FKA New Jersey Acquisition Corp.) a shell corporation which had

announced that it had reached an agreement to acquire EMC packaging which was subsequently

acquired by IEAM in October 2004. Mr. Margulies was engaged as outside counsel to IEAM,

became its CFO before resigning from that position on December 4, 2006. During the period

December 2006 through July 2007, Mr. Margulies was named and received salary compensation

from PPO in return for his services as head of IEAM’s legal department. Mr. Margulies rejoined

IEAM as CEO and CFO and a director in February 2008 as noted in the Company’s 8-K.

On March 6, 2009, the Company received a conditional resignation as its chief executive

officer, James W. Margulies, to be effective March 9, 2009. On March 9, 2009, the Company’s

Board of Directors accepted the resignation of Mr. Margulies as a director, chief executive

officer and chief financial officer. The resignation letter did not indicate any disagreement with

the company’s operations, policies or practices. Mr. Margulies offered to continue to assist the

Company in the completion of the June 2007 filing on Form 10-K, if requested.

As a result of Mr. Margulies’s various and ever-changing relationships with IEAM and

its former management and Board he appears to have been the custodian of the vast majority of

the parent company’s official corporate records, minutes, correspondence with regulators,

transfer agent, and D&O carrier, among others. He has also been the primary signatory on the

largest of the Company’s checking accounts. In his various capacities, Mr. Margulies and Mr.

Mazzuto were the two primary interfaces with IEAM’s outside auditors and various sub-

contractors of accounting services to the parent corporation.

FIRST AMENDED DISCLOSURE STATEMENT 12

C. Acquisitions.

In October 2004, the Company purchased all of the issued and outstanding capital stock

of EMC (the "EMC Shares") from the then holders of the EMC Shares. EMC became the

Company’s wholly owned subsidiary on the effective date of that purchase.

Effective June 30, 2005, the Company acquired 100% ownership of Unifide, which was a

leading marketer and seller of automotive chemicals and additives for an aggregate consideration

of approximately $3.1 million in cash, notes and stock, and Today’s Way, which manufactured

and packaged the products which were sold by Unifide, for an aggregate consideration of

approximately $950,000 in cash, notes and stock. As a result of these acquisitions, Unifide and

Today’s Way became the Company’s wholly owned subsidiaries as of July 17, 2005.

On January 31, 2006, pursuant to a Membership Interest Purchase Agreement dated

January 17, 2006 (the “Pitt Penn Agreement”), the Company purchased one hundred percent

(100%) of the membership interests of the Pitt Penn Group (as hereinafter defined), a supplier of

automotive and chemical products based outside of Pittsburgh, Pennsylvania. Pursuant to the

Pitt Penn Agreement, the Company acquired the Pitt Penn Group through the purchase of all of

the issued and outstanding membership interests of Spinwell. Spinwell, in turn, owned all of the

issued and outstanding membership interests of (1) Pitt Penn, and (2) Pitt Penn Oil DISC

Company, a Delaware corporation, (together, the "Pitt Penn Group") for an aggregate

consideration of $4,000,000 subject to adjustment as provided in the Pitt Penn Agreement. As a

result of this acquisition, Spinwell became the Company’s wholly owned subsidiary on

January 31, 2006.

On May 12, 2006, the Company sold Springdale Specialty Plastics, Inc., a subsidiary of

Pitt Penn (" Springdale ") pursuant to an Asset Purchase Agreement with Fortco Pittsburgh, LLC

("Fortco"). Pursuant to the Asset Purchase Agreement, the Company sold all right, title and

interest in and to the property and assets, real, personal or mixed, of every kind and description,

which relate solely to the business of Springdale to Fortco for an aggregate amount of two

million five hundred thousand dollars ($2,500,000.00), subject to adjustment as provided in the

Asset Purchase Agreement. The terms of the Asset Purchase Agreement were determined by

arms-length negotiations between the parties.

D. Private Placements- July 2005 through March 2006.

On December 28, 2007 the former management of IEAM filed Form 10-KSB,

Amendment Number 1 for the fiscal year ending June 2006. In that document prior management

identified three private placements. Unless otherwise noted, Debtors are relying on that

document for information disclosed with respect to private placements.

July 2005 Private Placement

IEAM reported that it entered into a subscription agreement as of July 19, 2005.

Pursuant to that subscription agreement, certain investors purchased securities, in a private

placement pursuant to Rule 506 of Regulation D under the Securities Act of 1933, as amended

FIRST AMENDED DISCLOSURE STATEMENT 13

(the "Securities Act"). They included (1) notes convertible into shares of IEAM’s common

stock, as well as (2) five-year warrants to purchase an aggregate of 1,270,833 (post-split) shares

of IEAM’s common stock (excluding finder’s warrants described below), for an aggregate

purchase price of $2,500,000, with $1,500,000 of that purchase price paid on July 19, 2005, the

initial closing date, and the remaining $1,000,000 paid on November 2, 2005, the second closing

date. JG Capital, Inc. ("JG Capital") acted as the finder in connection with the July 2005 private

placement

Pursuant to the subscription agreement, IEAM was required to file with the Securities and

Exchange Commission (the "SEC"), within 30 days of the closing of the July 2005 private

placement, a registration statement which registers the resale of all shares of its common stock

underlying the convertible notes and the warrants issued or issuable by IEAM to the investors in

the July 2005 private placement. IEAM did not comply with those obligations.

The company paid an aggregate of $278,995.27 representing accrued interest and

liquidated damages to the investors in the July 2005 private placement pursuant to a

modification, amendment and waiver agreement, dated as of March 8, 2006. The Company

concluded with such investors as part of the March 2006 private placement as described below

under “—March 2006 Private Placements— Modification, Amendment and Waiver Agreement.”

Debtors continued to incur liquidated damages to these investors until they filed the resale

registration statement on May 31, 2006.

January 2006 Private Placement

IEAM entered into a securities purchase agreement dated as of January 27, 2006 with

JLF Asset Management, LLC and the three funds it manages, JLF Offshore Fund, Ltd., JLF

Partners I, L.P., and JLF Partners II, L.P. (together, “JLF” or the “JLF entities”), pursuant to

which the three JLF entities purchased from IEAM, in a private placement pursuant to Rule 506

of Regulation D under the Securities Act, (1) debentures convertible into shares of IEAM

common stock, as well as (2) Class A warrants to purchase an aggregate of 1,064,166 (post split)

shares of IEAM common stock, and (3) Class B warrants to purchase an aggregate of 1,713,611

(post split) shares of IEAM common stock, for an aggregate purchase price of $5,000,000.

Pursuant to the January 2006 purchase agreement, IEAM agreed to file with the

Commission, within 60 business days of the closing of that offering, a registration statement

which registers the resale of all shares of IEAM common stock underlying the convertible

debentures and the warrants issued or issuable by IEAM to the JLF entities. IEAM did not

comply with those obligations. IEAM filed the registration statement on May 31, 2006.

March 2006 Private Placements

IEAM reported that it entered into a securities purchase agreement dated as of March 8,

2006 with certain investors pursuant to which those investors purchased securities, in a private

placement pursuant to Rule 506 of Regulation D under the Securities Act, (1) debentures

convertible into shares of IEAM common stock, as well as (2) Class A warrants to purchase an

aggregate of 402,778 (post split) shares of IEAM common stock, and (3) Class B warrants to

FIRST AMENDED DISCLOSURE STATEMENT 14

purchase 402,778 (post split), shares of IEAM common stock, for an aggregate purchase price of

$1,450,000.

In addition, also effective March 8, 2006, IEAM entered into a separate securities

purchase agreement (together with the abovementioned securities purchase agreement, the

“March 2006 purchase agreements”) with Truk International Fund, LP and Truk Opportunity

Fund, LLC (together, “Truk”), pursuant to which these investors purchased from IEAM, in a

separate private placement pursuant to Rule 506 of Regulation D under the Securities Act,

(1) debentures convertible into shares of IEAM common stock, as well as (2) Class A warrants to

purchase an aggregate of 138,888 (post split) shares of IEAM common stock, and (3) Class B

warrants to purchase an aggregate of 138,888 (post split) shares of IEAM common stock, for an

aggregate purchase price of $500,000.

The Class A warrants IEAM issued in the March 2006 private placement had the exercise

price of $3.40 per share, and the Class B warrants have the exercise price of $3.40 per share.

Each of the Class A and Class B warrants will expire on the third anniversary of their issuance

date, and can be exercised at any time during such period. The warrants we issued to the

investors in the March 2006 private placements are not subject to cashless exercise. As

previously noted, management is relying on information contained in a filing made by former

management of IEAM in Form 10-KSB, Amendment Number 1 for the fiscal year ending June

2006, filed on December 28, 2007. That document was silent with respect to the exercise of the

warrants. Current management is still reviewing these transactions. Any of such warrants

which have not been exercised have expired.

Pursuant to the March 2006 purchase agreements, IEAM agreed to file with the SEC,

within 60 business days of the closing dates of those offerings, a registration statement which

registers the resale of all shares of our common stock underlying the convertible debentures and

the warrants issued or issuable by IEAM to the investors in the March 2006 private placements.

IEAM did not comply with those obligations. IEAM filed the registration statement on May 31,

2006.

E. John D. Mazzuto’s Personal Bankruptcy is Disclosed to the Board.

In March 2006, the members of the Board of Directors of IEAM, were sent certified

letters by the former CEO of Advanced Biochem, Crawford Shaw. Among other things, those

letters notified the company that John Mazzuto’s 2002 bankruptcy which was filed in the U.S.

Bankruptcy Court Southern District of New York (SDNY), Case 02-15586-rdd, had not been

disclosed and needed to be disclosed in SEC filings.

• Mr. Shaw used an action against IEAM in Texas as the vehicle by which

he sued for payment under his employment contract.

• In conjunction with this lawsuit, Mr. Mazzuto was deposed in District

Court Harris County on July 12, 2006. His statements under oath are not

reflected in SEC filings.

FIRST AMENDED DISCLOSURE STATEMENT 15

• Mr. Mazzuto’s prior business history including various failed business

ventures, board seats and directorships and his ongoing personal

bankruptcy were never disclosed2.

On May 31, 2006 the Company filed a Form SB2 which is a securities registration for

small business. This registration statement is relevant. Despite the March 2006 written notice to

directors, IEAM continued to omit material facts. Specifically, this filing failed to disclose Mr.

Mazzuto’s bankruptcy, and the bankruptcy of George Cannan, Sr. (Chapter 7 Southern District

of Florida, Case 01-27073-BKC-RBR, Kenneth A Welt, US Bankruptcy Trustee).

According to U.S. Securities and Exchange Commission, Litigation Release No. 19732 /

June 21, 2006, SEC v. Carl R. Rose, et al., Civil Action No. H-04-CV-2799, the SEC announced

that on June 19, 2006, the United States District Court for the Southern District of Texas entered

a Final Judgment against Defendant George J. Cannan, Sr., based on his consent.

Cannan, Sr., without admitting or denying the allegations of the complaint, consented to

an order of permanent injunction which permanently restrained and enjoined him from violating,

directly or indirectly, the anti-fraud and reporting provisions of the Exchange Act as well as

other provisions of the Securities laws, including, Exchange Act Sections 10(b) (and Rule 10b-5

thereunder), 13(a), 13(d)(1) (and Rules 13d-1 and 13d-2 thereunder), 15(a)(1) and 16(a) (and

Rule 16a-3 thereunder) and Securities Act Sections 5 and 17(a) and Rule 101 of Regulation M

under the Exchange Act. The order also bars Cannan Sr. for five years from acting as an officer

or director of any issuer that has a class of securities registered pursuant to Section 12 of the

Exchange Act or that is required to file reports pursuant to Section 15(d). Further, the order

requires Cannan, Sr., to pay a civil penalty in the amount of $75,000.

George Cannan, Sr. acted as President and CEO of EMC from the time of its acquisition

on October 7, 2004 until his termination for cause on July 14, 2008. He was one of the five

highest paid officers of IEAM and its subsidiaries subsequently reached an agreement with the

SEC to refrain from acting as an officer or director of a public company.

Neither the SEC investigation nor the consent order was ever disclosed by IEAM in a

public filing. Further, despite a change in the corporate by-laws mandating the filing of a proxy

and the holding of an annual meeting, IEAM under the Mazzuto and Margulies management

never filed a proxy or held a shareholder meeting.

F. Indecent Disclosure: The Use of Press Releases, Investor Meetings, and

“Promoters.”

At the heart of the IEAM problems was Mazzuto’s and Margulies’s attempt to portray the

Debtors as a business success. As noted earlier, starting in late-2006, the Company hosted a

series of investor meetings designed to portray IEAM as a small but growing company in a

mundane business with professional management which was beginning to generate positive cash

2

Baker MacKenzie represented IEAM in this matter.

FIRST AMENDED DISCLOSURE STATEMENT 16

flow through operating efficiencies and the integration of similar businesses (EMC, Unifide, and

PPO).3

In early-December 2006, James Margulies resigned as CFO and moved to the legal

department. John Mazzuto assumed the role and announced the search for a permanent

replacement. In March 2007 the company announced that Dennis O’Neill had accepted a

position as CFO. Under a potential adversary proceeding in the Bankruptcy Court, Mr. O’Neill’s

counsel turned over certain documents including a March 8, 2007 initial agreement and a copy of

a May 11, 2007 resignation letter. The March 8, 2007 letter contradicts the Company’s public

statements. Points One and Two of that agreement are as follows:

1. All parties agree that the current operations of IEAM are in a “troubled state.”

2. The extent of this condition, if any, is not yet known to the parties.

With these three acquisitions under its belt, IEAM management was now in a position to

begin to tell a “story” which might attract investor interest. Company management made a series

of presentations in various public forums outlining their strategy of integrating these three

businesses on both an operational and financial basis.4

The company with the assistance of David Zazoff of ZA-Consulting began a public

relations campaign to tell the IEAM story. With JLF Asset Management, LLC, a well known

money management firm, as a core investor, the company began to craft a series of presentations

hosted by brokerage firms. The apparent purpose of these presentations was to promote the

merits of IEAM as being an attractive investment opportunity.

The company hosted major presentations as follows:

• September 7, 2006 – Roth Conference

• November 8, 2006 – Pacific Growth Conference

• March 14, 2007 – B. Riley Conference

Management also began hosting a series of plant tours. The October 25, 2006 investor

package was representative of IEAM’s standard presentation. In addition, beginning in

December 2006 the company was distributing a 77-page package telling the IEAM story. The

first seven pages of that package made a number of material misstatements about both the

company and Mr. Mazzuto. The last 70 pages consisted of public filings.

3

In retrospect, it appears that IEAM may have been insolvent in March 2007 or earlier. In response to a request from the

bankruptcy court, Dennis O’Neill’s attorney has turned over 2,000 pages of documents between August 25, 2009 and

August 31, 2009. A review of Mr. O’Neill’s correspondence in March 2007 suggests that was known to Mr. Mazzuto and

others at that time.

4

While IEAM took some steps to integrate operations, it continued to maintain three separate accounting systems. IEAM,

the parent company, kept its books on a Quickbooks accounting system. Pitt Penn Oil used a vibrant, state-of-the art

Microsoft Great Plains accounting system. Unifide and Today’s Way accounting were partially, but not completely,

integrated into this system. EMC Packaging maintains its accounting on a legacy accounting system.

FIRST AMENDED DISCLOSURE STATEMENT 17

IEAM has a June fiscal year. During the period December 4-6, 2006 the company filed a

10-QSB and two amendments for the period ended September 30, 2006. All of those documents

indicated that were just over 9.9 million shares outstanding. James Margulies, who acting as the

company’s CFO, stepped down from that position as of December 6, 2006 and joined the

company’s “legal department.” He continued as a salaried employee in that position until

July 31, 2007. Despite the fact that the press release referenced IEAM’s legal department, his

salary was paid by PPO without an offset to IEAM. During the period from August 1, 2007 until

February 2008 he had an ambiguous role as outside counsel to the audit committee and the

board.

Between October 2006 and the Spring of 2007, IEAM had begun to attract the attention

of many sophisticated institutional investors as well as a diverse group of individual investors.

The appeal of IEAM was based upon the proposition that a group of entrepreneurs had found a

publicly traded shell corporation (IEAM-FKA Advanced Bio Chem) and with the assistance of

some outside financing had assembled a portfolio of corporations producing products for the

automotive after markets.

In addition, in December 2006, the Company issued a press release which noted that it

had signed a joint venture with Sino Chem to import specialized gas into the United States.5

Further, while dilution was expected from the exercise of warrants and the conversion of various

notes, management suggested in various public forums that with all exercises fully diluted shares

would fall within a range of 13.0 – 14.0 million shares.

On February 16, 2007, the Company filed Form 10-QSB for the period ended

December 31, 2006. That filing indicated that there were 12.9 million shares outstanding. On

April 20, 2007 the company filed Form 8-A12B/A which is a NASDAQ listing application. That

form indicated that there were 16.848 million shares outstanding as of April 18, 2007. When

questioned about this on a conference call, Mr. Mazzuto suggested that these shares did not

reflect the “retirement” of certain shares due to stock purchase. On May 22, 2007 the company

filed a 10-QSB for the period ending March 31, 2007. That filing indicated that there were

13.297 million shares outstanding as of May 18, 2007.

An 8-K filing and a subsequent conference call shows that there was a $6.2 million

investment in a joint venture (which was identified as being with the Chinese partner). That

filing and conference call also indicated that there was a problem with revenue recognition. That

issue has subsequently been identified as a “bill and hold issue.” The issues of revenue

recognition and bill and hold are the central elements in a current class action complaint.

5

While SEC regulations require the filing of a report on Form 8-K to disclose “material events,” this press release was

among one of at least three press releases discussing a material event which were never filed with the SEC. As we have

determined, the information contained in the press release was false. Independent investigation and a Spring 2008 e-mail

from George Cannan to Dan Redmond confirm that there never was a joint venture.

FIRST AMENDED DISCLOSURE STATEMENT 18

On July 12, 2007, the Company issued a press release. That release indicated without

elaboration that there were 19.0 million shares outstanding. The press release also went on to

indicate that the company had authorized a $25.0 million share repurchase.6

On October 11, 2007, IEAM, along with all of its subsidiaries, entered into a $5.0 million

revolving credit line with Sovereign Bank. Margulies and Levinson provided an opinion letter to

Martin Weisberg at Baker McKenzie. Weisberg provided an opinion letter with respect to IEAM

to Sovereign Bank. In our subsequent review of the documents submitted to the bank it appears

that (1) the backgrounds of the principals were misstated, (2) IEAM was clearly not current in its

financial filings with the SEC, (3) other documentation supplied by IEAM may have been false,

and (4) IEAM was out of compliance with the terms of the loan when it was made.

On November 7, 2007 the Company issued two press releases. One related to the

suspension of Jorge Yepes, a CFO who had been appointed on September 4, 2007. The second

press release made a number of material disclosures relating to (1) a variable interest entity

(VIE) in Akron, OH; (2) an increase in a litigation reserve; (3) reversal of bill and hold activities

for the December 2006 and March 2007 quarters; (4) the settlement of certain litigation; (5) a

share count increased to 26.0 million shares; and (6) a continuation of a stock buyback program,

among other items. These disclosures, all of which were material, were never filed with the SEC

on Form 8-K.

On January 31, 2008, the Company filed an 8-KA which indicated that on January 15,

2008 Black Nickel had lent IEAM $750,000 at a double digit interest rate and received 75,000

purchase warrants plus 2.0 million shares of IEAM stock increasing the shares outstanding to

28.0 million.7

G. February 2008 - John D. Mazzuto Resigns and James W. Margulies Becomes

CEO and CFO.

On February 5, 2008, James Margulies replaced John Mazzuto as both CEO and CFO.

On February 19, 2008 the Company issued a four page press release entitled, “IEAM Provides an

Accounting and Operational Update.” That press release discussed (1) the delayed filings, (2)

the increase in share count announced in the July 12, 2007 press release, and (3) the company’s

financing needs.8

Of particular interest was the caption, “The substantial increase in share count

announced in the July 12, 2007 Press Release was a surprise to investors and to the Board.”

6

Our subsequent review of the record books shows that as of June 30, 2007 the company’s transfer agent suggests that there

were approximately 22.9 million shares outstanding. In our limited access to board records, we have found no such

approval. Further given the company’s actual cash position at the time, no such program was feasible.

7

The company failed to disclose that on January 15, 2008 it had issued some 500,000 shares of freely trading IEAM shares

to Black Nickel under its S-8 registration statement.

8

The February 19, 2008 press release was never filed as part of a Form 8-K.

FIRST AMENDED DISCLOSURE STATEMENT 19

The notation went on to say, “the vast majority of the increase in the number of shares

were properly and rightfully issued on the exercise of convertible debt and warrants thereto;

however additional shares appear to have been issued by the former CEO based upon

authorization granted to him by the December 2004 Board of Directors….” The Debtors’

subsequent review suggested this was disingenuous at best and an outright fabrication at worst.9

In February 2008, Jim Margulies committed to filing the company 10-K for the period

ending June 2007 within several weeks of taking office as CEO and CFO. No such 10-K has yet

been filed.

H. April 2008 - Mr. Margulies Discusses the Company’s Cash Requirements

With a Number of Significant Investors.

Immediately prior to taking the position of CEO and CFO and, shortly thereafter, Mr.

Margulies, the new CEO and CFO of IEAM, discussed the capital requirements of IEAM on a

going-forward basis. The problems facing IEAM were described as a simple liquidity issue.

Certain large investors who owned up to 60.0% of the outstanding shares of the Company’s

common stock indicated that upon the filing of the 10-K for FY 2007, they were willing to

consider a participation in a rights offering to provide $3.0-$5.0 million of common or preferred

stock. The condition was that it be open and available to all current stockholders of the

Company.

Despite assurances to both the investment community and to the Company’s secured

lender that Mr. Margulies was merely reviewing a 10-K prepared by Mr. Mazzuto, no such 10-K

was ever filed. As noted later, the failure to file the June 2007 10-K was a violation of the

Company’s loan agreement with Sovereign Bank as well as a violation of the Black Nickel

agreement. As a result of the failure to file the 10-K, Mr. Margulies caused IEAM to issue an

additional 1.5 million shares to Black Nickel. Further, the failure to file the 10-K was the

proximate cause of Sovereign Bank’s decision to freeze the funds in the Company’s bank

accounts in October 2008.

On April 7, 2008, Mr. Margulies, Mr. Redmond, Mr. Zazoff and Daniel Boucher met

with institutional investors and others who owned more than 45.0% of the company’s shares

outstanding. The purpose of the meeting was to discuss (1) certain financing alternatives, (2) the

potential sale of EMC to George Cannan, Sr. and (3) provide an update on the preparation of the

10-K for FY 2007. During the course of that discussion, Mr. Margulies asserted that if IEAM

did not receive a cash injection of more than $9.0 million by Friday, April 11, 2008 he would be

forced to file “bankruptcy.” He did not specify whether he was contemplating Chapter 11 or

Chapter 7 nor did he specify which of the corporate entities he was considering for a bankruptcy

alternative.

9

Our review of the share issuance data, as discussed later in this report, shows that the transfer agent received instructions

signed by either Mr. Mazzuto or Mr. Margulies to issue shares pursuant to an S-8 filed in February 2005. The S-8 was

never made effective. In addition, while the July 12th press release refers to 19.0 million shares outstanding as of the end of

June 2007, there were actually 22.9 million shares outstanding.

FIRST AMENDED DISCLOSURE STATEMENT 20

Subsequent to that meeting the present CEO was contacted by other large shareholders

and was asked to propose a solution for reorganization. On April 9, 2008 both Mr. Ward and

Mr. Renck agreed to begin reviewing reorganization alternatives. At that juncture Mr. Margulies

agreed to provide certain high level information with respect to the operating results of the two

major subsidiaries, PPO and EMC. On or about June 30, 2008, the Company agreed to provide

more detailed information with respect to the subsidiaries.

On Saturday August 9, 2008, Mr. Margulies and the outside investors agreed on a

conceptual approach towards resolving the financial and operational problems faced by IEAM

and its subsidiaries. Other members of IEAM’s operating management then became involved in

the due diligence process. A review of the subsidiary books and records revealed that PPO was

being burdened with excessive salaries including those at parent. The combined staff salaries

throughout the organization as of June 30, 2008 were just under $5.0 million. This did not

include any stock based compensation or grants to various “consultants” or outside contractors

being paid by parent (IEAM). In addition, a review of the internal books and records of the

subsidiaries suggested that there was a significant disconnect between reported results and

reality.

Despite the problems at IEAM, numerous press releases and presentations suggested that

PPO (the major operating entity) was generating positive cash flow during all of 2007. As a

result of questions asked during an intensive due diligence review which began on or about

June 29, 2008, Mr. Redmond prepared a report which indicated that Pitt Penn Oil had never

generated positive cash flow.

I. April 2009 - All Prior Financials, Stock Issuances, and Disclosures Are

Under Review By Current Management.

In a Form 8-K filed with the SEC on May 29, 2009, the current management of IEAM

made the following disclosure:

Under new management, Debtors have been conducting an ongoing review of the

financial records and the books and records of subsidiaries and parent. As part of this review, the

Company has been endeavoring to gather and analyze the books and records from various

sources.

To date, the Company’s review has focused upon the intracompany transactions and the

issuance of the Company’s securities pursuant to certain agreements between the Company and

the subsidiaries and various consultants.

1. The Chaotic State of the Corporate Records Has Created a Major

Problem for New Management.

IEAM is a holding company incorporated in the State of Nevada, with four direct

subsidiaries, EMC, Today’s Way, Unifide, and PPH. IEAM is the sole owner of PPO as a result

of its 100% ownership of PPH. PPO, with annual revenues of approximately $25 Million at the

time of its acquisition in January 2006, became the main operating subsidiary of the IEAM

FIRST AMENDED DISCLOSURE STATEMENT 21

Group. The operational activities of Today’s Way and Unifide had been effectively absorbed

into PPO by December 2006. IEAM had indicated that they were “consolidated.”

By January 2007 Pitt Penn Oil was paying for the obligations of PPO, Today’s Way and

Unifide. In February and May 2007, IEAM acquired the assets of Fire 1st Defense LLC (“FFD”)

and High-Tach respectively. High-Tach was absorbed into PPO.

While relatively small in comparison, at $3 Million in average annual revenues, EMC

remained the only subsidiary with its own payroll and operations. While both the FFD and Hi-

Tach acquisitions were asset purchases, FFD was by all appearances managed from EMC. The

assets of FFD were owned by IEAM. They were physically transferred to EMC. George

Cannan, in his role as President of EMC Packaging, incorporated FFD as a “C” corporation in

the State of Delaware. A separate checking account was set up and certain revenues were run

through that account. This entity was never recorded on the books of either IEAM or EMC.

By 2006, IEAM, as the parent company, had no employees. The burden of payroll

disbursements, as well as the obligations of Today’s Way and Unifide previously mentioned,

were pushed down to PPO.

Functionally, IEAM typically only appears to have had two or three officers at any given

time. From the period December 2006 through February 2008, John Mazzuto was the CEO/CFO

at which time he resigned and was replaced on an interim basis by James Margulies. Mr.

Margulies, over the period 2005 to July 2007, held various roles including CFO and Secretary.

During that period he was paid as an employee of PPO. Robert Dan Redmond served as

Executive VP and President of IEAM during his tenure. Dennis F. O’Neill served as CFO as did

his replacement Jorge Yepes. All of those individuals received their compensation from PPO.

Mr. Margulies continued to be actively engaged with the company on legal and

accounting matters until he assumed the CEO/CFO role in February 2008. In fact, the

accounting records indicate that even after he stepped down as CFO in December 2006 he

appeared to be actively engaged along with Mr. Mazzuto, in the preparation of IEAM’s internal

financial records. The National City Bank checkbook was maintained in Cleveland Ohio at his

office during that time.

Rather than consolidate IEAM financial operations at PPO, where the bulk of the staff

and the most robust accounting system resided, IEAM used paid professionals to fulfill other

roles, primarily accounting. Both Dennis O’Neill and Jorge Yepes, CFOs of IEAM maintained

offices at PPO. Debtors do not know what access, if any they had to IEAM parent records or

checkbooks.

The overall corporate organizational structure of IEAM and its subsidiaries is

unremarkable. What is remarkable is the lack of organizational oversight previously provided by