You might also like

- RG - 2012-13Document6 pagesRG - 2012-13sam_bhopNo ratings yet

- Updates On Global Credit Exposure Policy 2020 - KEDAR KULKARNIDocument11 pagesUpdates On Global Credit Exposure Policy 2020 - KEDAR KULKARNIShilpa JhaNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document5 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Tradres Loan 2016 BCC - BR - 108 - 432Document45 pagesTradres Loan 2016 BCC - BR - 108 - 432RAJANo ratings yet

- Risk Synopsis - Brookes Pharma (PVT) LTDDocument9 pagesRisk Synopsis - Brookes Pharma (PVT) LTDZ_Z_Z_ZNo ratings yet

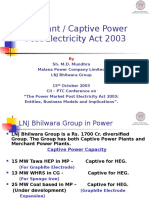

- M D Mundhra - Malana PowerDocument17 pagesM D Mundhra - Malana PowerrobinNo ratings yet

- 12pwd108 258Document55 pages12pwd108 258Shahab KhanNo ratings yet

- Cmpli: L. R-VPDocument13 pagesCmpli: L. R-VPAnsuman SingNo ratings yet

- The Introduction of Lean Manufacturing Concepts at QualcommDocument25 pagesThe Introduction of Lean Manufacturing Concepts at Qualcommzakria100100No ratings yet

- Assignment On Financial ManagementDocument13 pagesAssignment On Financial Managementdiplococcous89% (9)

- 1.5 MLDDocument40 pages1.5 MLD9044nksNo ratings yet

- ( FLF") F'XX: LD: Card'Document6 pages( FLF") F'XX: LD: Card'rafikul123No ratings yet

- Standalone Financial Results, Form A, Auditors Report For March 31, 2016 (Result)Document9 pagesStandalone Financial Results, Form A, Auditors Report For March 31, 2016 (Result)Shyam SunderNo ratings yet

- 3X660Mw Koradi Thermal Power Station, Koradi: 1. Qualification CriteriaDocument4 pages3X660Mw Koradi Thermal Power Station, Koradi: 1. Qualification Criteriarbdubey2020No ratings yet

- CAP Regulation 70-1 - 09/01/2003Document49 pagesCAP Regulation 70-1 - 09/01/2003CAP History LibraryNo ratings yet

- Title-15 kVA TF - T-1256Document10 pagesTitle-15 kVA TF - T-1256Ubaid Ur RehmanNo ratings yet

- Standalone Financial Results For September 30, 2016 (Result)Document2 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Ready Reckoner For Retail UpgradationDocument122 pagesReady Reckoner For Retail UpgradationAnuranjan ShettyNo ratings yet

- RDSO Vendor1Document169 pagesRDSO Vendor1adarshietk100% (1)

- 3.3 Technical Specifications of Prefabricated ContainerizedDocument81 pages3.3 Technical Specifications of Prefabricated Containerized021804No ratings yet

- Full Result Ip Revised Result 2020Document105 pagesFull Result Ip Revised Result 2020Justin PrabaharNo ratings yet

- BII ClarificationsDocument13 pagesBII ClarificationsJinalSNo ratings yet

- Vendor Directory2014 WagonsDocument211 pagesVendor Directory2014 WagonsKundan MeshramNo ratings yet

- Technology and LicenorDocument7 pagesTechnology and LicenorahmedNo ratings yet

- Nit KSGN 17 559CDocument4 pagesNit KSGN 17 559CAjay NandaNo ratings yet

- ASPIRE10.01.2022Document16 pagesASPIRE10.01.2022tushar nathNo ratings yet

- Tendernotice 1Document13 pagesTendernotice 1Vijay KumarNo ratings yet

- Case StudyDocument21 pagesCase StudyAmarinder Singh Sandhu100% (1)

- CPCS 2021-013 Grant of Extraordinary and Miscellaneous ExpensesDocument3 pagesCPCS 2021-013 Grant of Extraordinary and Miscellaneous ExpensesEdson Jude DonosoNo ratings yet

- Policy For Commerical VehicleDocument37 pagesPolicy For Commerical VehicleMadhu Shankar GowdaNo ratings yet

- Budget and ExpenditureDocument56 pagesBudget and ExpenditureManohara BabuNo ratings yet

- Final Assignment On FMDocument13 pagesFinal Assignment On FMRahul GuptaNo ratings yet

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document5 pagesFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document6 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- BOI MSME Loan ProductsDocument95 pagesBOI MSME Loan ProductsganpatigajanandganeshNo ratings yet

- Sandfits Foundries Private LimitedDocument7 pagesSandfits Foundries Private Limitedvignesh seenirajNo ratings yet

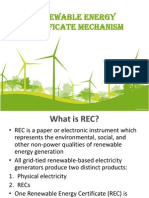

- Renewable Energy Certificate MechanismDocument36 pagesRenewable Energy Certificate MechanismAdam CunninghamNo ratings yet

- Faqs Eclgs Updated On 31.03.2022Document32 pagesFaqs Eclgs Updated On 31.03.2022Akhtar HussainNo ratings yet

- Nabard Rural Godown PDFDocument6 pagesNabard Rural Godown PDFVivek KhandelwalNo ratings yet

- Guidelines For RFQDocument69 pagesGuidelines For RFQjawed_mazharNo ratings yet

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Document2 pagesStatement On Impact of Audit Qualifications For The Period Ended March 31, 2015 (Company Update)Shyam SunderNo ratings yet

- Key Credit Factor For The Retail and Restaurants IndustryDocument18 pagesKey Credit Factor For The Retail and Restaurants IndustryAl MahmunNo ratings yet

- Bid Query ExampleDocument7 pagesBid Query ExampleSandeep K TiwariNo ratings yet

- Sanction Letter Pages For TLDocument5 pagesSanction Letter Pages For TLgtyhNo ratings yet

- Love Council Proposal Alt Rev24 Plus Flow ChartDocument9 pagesLove Council Proposal Alt Rev24 Plus Flow ChartcityhallblogNo ratings yet

- 01 - Adv Issues in Cap BudgetingDocument17 pages01 - Adv Issues in Cap BudgetingMudit KumarNo ratings yet

- Accounting 100 Imp Questions 1642414989Document93 pagesAccounting 100 Imp Questions 1642414989Shashank SikarwarNo ratings yet

- TVNL - 10G Switch - Wo - 066 - 24.01.2021Document2 pagesTVNL - 10G Switch - Wo - 066 - 24.01.2021Md. Aslam JabedNo ratings yet

- Advance Circular Revision in Interest Rates On Domestic NRO NRE Rupee Term Deposits W e F 20.08.2022Document5 pagesAdvance Circular Revision in Interest Rates On Domestic NRO NRE Rupee Term Deposits W e F 20.08.2022bansalh06No ratings yet

- 1 Bid Document Vol IDocument122 pages1 Bid Document Vol IDhabalia AshvinNo ratings yet

- Tender Enquiry: OfficeDocument17 pagesTender Enquiry: OfficeThanh Phuc NguyenNo ratings yet

- Investor Updates (Company Update)Document28 pagesInvestor Updates (Company Update)Shyam SunderNo ratings yet

- Delegation of Power To The Project Officers of Mines/Projects, Washeries, Captive Power Plant and Regional Repair ShopsDocument15 pagesDelegation of Power To The Project Officers of Mines/Projects, Washeries, Captive Power Plant and Regional Repair ShopsTowshif SkNo ratings yet

- t000004815 - Filename - Tender Crude Antifoulant Cdu 1 and Cdu 2Document53 pagest000004815 - Filename - Tender Crude Antifoulant Cdu 1 and Cdu 2Prashant SinghNo ratings yet

- Advertisement - Final - Central Zone - SignedDocument4 pagesAdvertisement - Final - Central Zone - SignedMANOJ BORUAHNo ratings yet

- Re-Tpis: Short Notice Inviting BidsDocument8 pagesRe-Tpis: Short Notice Inviting Bidsrafikul123No ratings yet

- 2decision Theory HODocument14 pages2decision Theory HOadesh guliaNo ratings yet

- 117-06 Part 1 Vehicle Loan Master CircularDocument50 pages117-06 Part 1 Vehicle Loan Master CircularManish Kumar KingraniNo ratings yet

- Harmonizing Power Systems in the Greater Mekong Subregion: Regulatory and Pricing Measures to Facilitate TradeFrom EverandHarmonizing Power Systems in the Greater Mekong Subregion: Regulatory and Pricing Measures to Facilitate TradeNo ratings yet

- Facilitating Power Trade in the Greater Mekong Subregion: Establishing and Implementing a Regional Grid CodeFrom EverandFacilitating Power Trade in the Greater Mekong Subregion: Establishing and Implementing a Regional Grid CodeNo ratings yet

- Manual of Simulation With Arena For Lab - Note - 3Document16 pagesManual of Simulation With Arena For Lab - Note - 3Kristin MackNo ratings yet

- Additive Manufacturing - Types PDFDocument60 pagesAdditive Manufacturing - Types PDFRAJANo ratings yet

- Additive Manufacturing of Parts For Indigenous Aero EnginesDocument1 pageAdditive Manufacturing of Parts For Indigenous Aero EnginesRAJANo ratings yet

- Additive Manufacturing of Parts For Indigenous Aero EnginesDocument1 pageAdditive Manufacturing of Parts For Indigenous Aero EnginesRAJANo ratings yet

- Arena TutorialDocument8 pagesArena TutorialCoxa100NocaoNo ratings yet

- QTR Ch8 - Additive Manufacturing TA Feb-13-2015 - 0 PDFDocument27 pagesQTR Ch8 - Additive Manufacturing TA Feb-13-2015 - 0 PDFRAJANo ratings yet

- Ijaerv12n18 97Document15 pagesIjaerv12n18 97RAJANo ratings yet

- Arena TutorialDocument8 pagesArena TutorialCoxa100NocaoNo ratings yet

- Install Notes PDFDocument5 pagesInstall Notes PDFRAJANo ratings yet

- SyllabusDocument81 pagesSyllabusRAJANo ratings yet

- Interactive Aerospace Engineering and Design by Dava J. NewmanDocument374 pagesInteractive Aerospace Engineering and Design by Dava J. NewmanGuillermo Alcantara100% (1)

- 2 2013 Motorcycle Helmets A State of The Art Review1Document21 pages2 2013 Motorcycle Helmets A State of The Art Review1RAJANo ratings yet

- Arena Serial NumberDocument1 pageArena Serial NumberRAJANo ratings yet

- Roll No: (To Be Filled in by The Candidate)Document2 pagesRoll No: (To Be Filled in by The Candidate)RAJANo ratings yet

- Polyethylene: Assembly Name: Water Pump FixtureDocument1 pagePolyethylene: Assembly Name: Water Pump FixtureRAJANo ratings yet

- Tolerance ChartDocument1 pageTolerance ChartRAJANo ratings yet

- 4.0 Number of Cavities CalculationDocument40 pages4.0 Number of Cavities CalculationStelwin Fernandez80% (5)

- Guidelines For Project Work111Document5 pagesGuidelines For Project Work111RAJANo ratings yet

- Fe-C Phase DiagramDocument34 pagesFe-C Phase DiagramYoung-long Choi100% (1)

- Design Basics: or How To Put Together Simple Things SimplyDocument26 pagesDesign Basics: or How To Put Together Simple Things SimplyRAJANo ratings yet

- End Plate Base: Name: Gowtham Kumar ROLL NO: 15P208Document1 pageEnd Plate Base: Name: Gowtham Kumar ROLL NO: 15P208RAJANo ratings yet

- Combination of SpoonsDocument5 pagesCombination of SpoonsRAJANo ratings yet

- Patents: Production of Edible China SpoonDocument6 pagesPatents: Production of Edible China SpoonRAJANo ratings yet

- 1594 1426 1 PB PDFDocument6 pages1594 1426 1 PB PDFRAJANo ratings yet

- CH 14Document2 pagesCH 14RAJANo ratings yet

- Scanned by CamscannerDocument9 pagesScanned by CamscannerRAJANo ratings yet

- Design of A HelmetDocument43 pagesDesign of A HelmetShooters Anna ReloadedNo ratings yet

- Surveying ErrorsDocument9 pagesSurveying ErrorsVikash PeerthyNo ratings yet

- 3 SgefDocument4 pages3 SgefRAJANo ratings yet

- Lecture 8Document12 pagesLecture 8Jiawei WangNo ratings yet

- 1 Kyc PDFDocument70 pages1 Kyc PDFMallikaNo ratings yet

- Slips Edu 06-2021Document9,468 pagesSlips Edu 06-2021Umar AzanNo ratings yet

- Claimspaid 2021Document72 pagesClaimspaid 2021sNo ratings yet

- Analysis of Mutual Fund & Portfolio Management in Mutual Fund For Motilal Oswal Securities by Kalpa KabraDocument59 pagesAnalysis of Mutual Fund & Portfolio Management in Mutual Fund For Motilal Oswal Securities by Kalpa KabravishalbehereNo ratings yet

- Bcom ProjectDocument76 pagesBcom ProjectVictor Muto100% (1)

- BCD 4 Design and Build With Schedule of Contract AmendmentsDocument45 pagesBCD 4 Design and Build With Schedule of Contract AmendmentstsuakNo ratings yet

- Tutorial 1 AnswersDocument4 pagesTutorial 1 AnswersBee LNo ratings yet

- Dist AgreementDocument45 pagesDist AgreementknowsauravNo ratings yet

- InfraPPP Resources April 2012Document26 pagesInfraPPP Resources April 2012PPPnewsNo ratings yet

- ReportDocument1 pageReportumaganNo ratings yet

- Employment Offer 'Salahudin'Document6 pagesEmployment Offer 'Salahudin'knight1729No ratings yet

- FAR Study Plan - Becker 2018Document11 pagesFAR Study Plan - Becker 2018Gift ChaliNo ratings yet

- Customer Satisfaction On Online Banking of EXIM Bank LTD.: BRAC UniversityDocument42 pagesCustomer Satisfaction On Online Banking of EXIM Bank LTD.: BRAC UniversityRashel MahmudNo ratings yet

- Pilar de Lim V Sun Life Assurance Company of CanadaDocument1 pagePilar de Lim V Sun Life Assurance Company of Canadakenken320No ratings yet

- Actuarial Mathematics For Life Contingent RisksDocument7 pagesActuarial Mathematics For Life Contingent RisksIda Khairina KamaruddinNo ratings yet

- Master Sub-Fee Protection Agreement With Participants' Full DetailsDocument8 pagesMaster Sub-Fee Protection Agreement With Participants' Full DetailsAlexandre Poignant-spalikowski100% (7)

- Conversion Active LandlinesDocument8 pagesConversion Active LandlinesRitsheNo ratings yet

- Level 3 Integrated Advisory ServicesDocument1 pageLevel 3 Integrated Advisory ServicesAce RamosoNo ratings yet

- David Widlak Hoped He Had Found An Angel To Help Save His Struggling BankDocument21 pagesDavid Widlak Hoped He Had Found An Angel To Help Save His Struggling BankReality TV ScandalsNo ratings yet

- Fee Decleration FormDocument2 pagesFee Decleration FormMohit MohanNo ratings yet

- JMGS1 - Recollected Questions of Exam Held in Feb-2016Document4 pagesJMGS1 - Recollected Questions of Exam Held in Feb-2016Anonymous Ey8uMU5nNo ratings yet

- Charges/Borrowing Details: Charge ID Creation Date Modification Date Closure DateDocument10 pagesCharges/Borrowing Details: Charge ID Creation Date Modification Date Closure DateAnonymous qWY12CYlmNo ratings yet

- Religare Explore Insurance BrochureDocument2 pagesReligare Explore Insurance BrochurearuvindhuNo ratings yet

- Merchant BankingDocument43 pagesMerchant BankingAbhishek Sanghvi100% (1)

- Nov Unlocked PDFDocument4 pagesNov Unlocked PDFDeshraj SehraNo ratings yet

- SIPOC-Cash and Check DepositDocument8 pagesSIPOC-Cash and Check DepositJanice Calunsag ChavezNo ratings yet

- Best Finacle Step by Step Finacle Steps PDFDocument13 pagesBest Finacle Step by Step Finacle Steps PDFTanuj VermaNo ratings yet

- Proposal Eta Theke BanaisiDocument109 pagesProposal Eta Theke BanaisiMaruf Hasibul IslamNo ratings yet

- Taxation of Passed-On' GRTDocument3 pagesTaxation of Passed-On' GRTjeorgiaNo ratings yet

- 12 Favourite Sales Pitches of A Life Insurance 1215321666163853 9Document6 pages12 Favourite Sales Pitches of A Life Insurance 1215321666163853 9D.V.SUBBAREDDYNo ratings yet