You might also like

- GIMPA SPSG Short Programmes 10.11.17 Full PGDocument2 pagesGIMPA SPSG Short Programmes 10.11.17 Full PGMisterAto MaisonNo ratings yet

- Acyst Tech SupportDocument7 pagesAcyst Tech SupportMisterAto MaisonNo ratings yet

- How To Determine The Location of A Mobile Subscriber: Sergey PuzankovDocument3 pagesHow To Determine The Location of A Mobile Subscriber: Sergey PuzankovMisterAto MaisonNo ratings yet

- MTG2000 Trunk Gateway Datasheet v1.0Document3 pagesMTG2000 Trunk Gateway Datasheet v1.0MisterAto MaisonNo ratings yet

- QOs Trend For April 2012Document6 pagesQOs Trend For April 2012boulicoNo ratings yet

- Tower LicenceDocument28 pagesTower LicenceMisterAto MaisonNo ratings yet

- SASSE 1988 Biogas PlantsDocument66 pagesSASSE 1988 Biogas PlantsOmar EzzatNo ratings yet

- An Invitation To Submit BidsDocument28 pagesAn Invitation To Submit BidsMisterAto MaisonNo ratings yet

- 2022 - 11 CCC QcombbdbgDocument41 pages2022 - 11 CCC QcombbdbgFrancesco PompiliNo ratings yet

- National Communications Authority (Nca) 2015 New Schedule of FeesDocument8 pagesNational Communications Authority (Nca) 2015 New Schedule of FeesMisterAto MaisonNo ratings yet

- Dinstar GSM/CDMA VoIP Gateway Configuration GuideDocument7 pagesDinstar GSM/CDMA VoIP Gateway Configuration GuideMisterAto MaisonNo ratings yet

- Mobicents SLEE RA MAP User GuideDocument36 pagesMobicents SLEE RA MAP User GuideMisterAto MaisonNo ratings yet

- Vehicle Tracking System Using "GPS" and "Google Maps"Document24 pagesVehicle Tracking System Using "GPS" and "Google Maps"MisterAto MaisonNo ratings yet

- Vos 2500Document217 pagesVos 2500lankoorNo ratings yet

- Course Contents:: Tech-Vidhya Certified 3G Implementation Engineer Tech-Vidhya Certified 3G Implementation EngineerDocument4 pagesCourse Contents:: Tech-Vidhya Certified 3G Implementation Engineer Tech-Vidhya Certified 3G Implementation EngineerMisterAto MaisonNo ratings yet

- clc3220 PDFDocument228 pagesclc3220 PDFMisterAto MaisonNo ratings yet

- Coral Zephyr Gsm/Cdma GatewayDocument10 pagesCoral Zephyr Gsm/Cdma GatewayMisterAto MaisonNo ratings yet

- Call and SMS Termination Case StudyDocument2 pagesCall and SMS Termination Case StudyMisterAto MaisonNo ratings yet

- Restoring The Value of The CediDocument50 pagesRestoring The Value of The CediMahamudu Bawumia100% (6)

- VSAT BrochureDocument13 pagesVSAT BrochureMisterAto MaisonNo ratings yet

- Userman Hotspot TutorialDocument17 pagesUserman Hotspot TutorialMisterAto MaisonNo ratings yet

- The VSAT Buyers GuideDocument148 pagesThe VSAT Buyers GuidesleeperinNo ratings yet

- Asterisk Ss7 Performance TestingDocument9 pagesAsterisk Ss7 Performance TestingPatrick Chenjun ShenNo ratings yet

- AX1600P-Elastix SetupguideDocument11 pagesAX1600P-Elastix SetupguideMisterAto MaisonNo ratings yet

- AtlasCopcoGhana EMEA Apr12 Bro SDocument7 pagesAtlasCopcoGhana EMEA Apr12 Bro SMisterAto MaisonNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CONTEXT CORP. v. CIR - DigestDocument2 pagesCONTEXT CORP. v. CIR - DigestMark Genesis RojasNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sushma KumariNo ratings yet

- Capital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsDocument6 pagesCapital Gains Tax For Onerous Transfer of Real Property Classified As Capital AssetsCyrill L. MarkNo ratings yet

- Amended 1040 Tax Form ExplainedDocument2 pagesAmended 1040 Tax Form Explainedgolcha_edu532No ratings yet

- Employee pay slip detailsDocument1 pageEmployee pay slip detailsvenkat100% (2)

- My JioDocument1 pageMy JioNishanthNo ratings yet

- Fix PPH 22 Dan PPH 23 (ENGLISH)Document19 pagesFix PPH 22 Dan PPH 23 (ENGLISH)Muhammad NunoNo ratings yet

- Dashboard For Ebitda Analysis InvestmentsDocument41 pagesDashboard For Ebitda Analysis InvestmentsDiyanaNo ratings yet

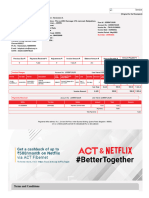

- Act Internet InvoiceDocument2 pagesAct Internet InvoiceSaravanan GuruNo ratings yet

- Office Aggreement 1stDocument3 pagesOffice Aggreement 1stValuelytic AgroNo ratings yet

- CIR V Estate of Benigno Toda (GR No 147188, Sept 2004)Document10 pagesCIR V Estate of Benigno Toda (GR No 147188, Sept 2004)JonNo ratings yet

- PWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021Document6 pagesPWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021arifansari2299No ratings yet

- Receipt BookingDocument1 pageReceipt BookingSultan Gamer 18No ratings yet

- Filinvest Wins Tax Refund CaseDocument11 pagesFilinvest Wins Tax Refund CaseClarinda MerleNo ratings yet

- Complete P&L Statement TemplateDocument4 pagesComplete P&L Statement TemplateGolamMostafaNo ratings yet

- Form 16 2019 20Document4 pagesForm 16 2019 20Kishan SinghNo ratings yet

- Mahusay Acc227 Module 2Document9 pagesMahusay Acc227 Module 2Jeth MahusayNo ratings yet

- CITN STUDY Pack - International TaxationDocument166 pagesCITN STUDY Pack - International TaxationOguntimehin AdebisolaNo ratings yet

- W 8benDocument1 pageW 8benAdam AkbarNo ratings yet

- Surbhi Steel HostingDocument1 pageSurbhi Steel HostingDarshan PatelNo ratings yet

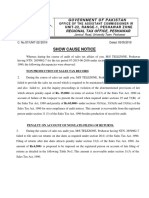

- Show Cause Notice: Government of PakistanDocument3 pagesShow Cause Notice: Government of PakistanFAIZ AliNo ratings yet

- UMi Inc. Payroll ReportDocument10 pagesUMi Inc. Payroll ReportSeagate SilverNo ratings yet

- Umali vs. EstanislaoDocument11 pagesUmali vs. EstanislaoJuan Dela CruzNo ratings yet

- TCS compensation letter details annual pay Rs. 4,69,860Document4 pagesTCS compensation letter details annual pay Rs. 4,69,860AbdulkhadarJilani ShaikNo ratings yet

- ACC 203 Taxation in NepalDocument9 pagesACC 203 Taxation in NepalSophiya PrabinNo ratings yet

- NYS-45 quarterly tax filingDocument2 pagesNYS-45 quarterly tax filingMichael WalkerNo ratings yet

- Sap Bydesign 1702 Product Info Product DataDocument116 pagesSap Bydesign 1702 Product Info Product DataMohammed DobaiNo ratings yet

- Tax Quiz 8-27Document5 pagesTax Quiz 8-27mhilet_chiNo ratings yet

- 13.cir V Benguet CorpDocument5 pages13.cir V Benguet CorpQuengilyn QuintosNo ratings yet

- Tax 2 Syllabus - DDL - 2019 PartA 11jan2019Document7 pagesTax 2 Syllabus - DDL - 2019 PartA 11jan2019ebernardo19No ratings yet