You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Extensive Bin ListDocument64 pagesExtensive Bin ListMajor Minor67% (6)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- E Cash Payment SystemDocument29 pagesE Cash Payment Systemhareesh64kumar100% (2)

- Marketplace Handbook 11 08 2015 PDFDocument56 pagesMarketplace Handbook 11 08 2015 PDFomthakur77100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Cricket Bill Pay Methods - Cricket WirelessDocument6 pagesCricket Bill Pay Methods - Cricket WirelessJohn Michael Antonio100% (1)

- Sbi PDFDocument2 pagesSbi PDFpavans25No ratings yet

- JNNJDocument48 pagesJNNJBirdmanZxNo ratings yet

- Invoice #RCS-25559-23102019: Riau Cyber SolutionDocument1 pageInvoice #RCS-25559-23102019: Riau Cyber SolutionDave JhonNo ratings yet

- Sinergitas Perbankan Dan Financial TechnologyDocument11 pagesSinergitas Perbankan Dan Financial Technologysub bidang belanja tidak langsung BPKADmagelangkotaNo ratings yet

- Jamie Leigh Case 2608 Haines City Crest, DR 33844Document1 pageJamie Leigh Case 2608 Haines City Crest, DR 33844SolomonNo ratings yet

- 2020 - Medici - India Fintech ReportDocument125 pages2020 - Medici - India Fintech Reportdevang bohra100% (3)

- New Text DocumentDocument3 pagesNew Text Documentngtkoanh100% (1)

- CB Insights Corporate Innovation Labs Finance NurtureDocument47 pagesCB Insights Corporate Innovation Labs Finance Nurturedrestadyumna ChilspiderNo ratings yet

- PDFDocument3 pagesPDFPrabha KaranNo ratings yet

- Robo Advisory 2Document8 pagesRobo Advisory 2Ankur Pandey0% (1)

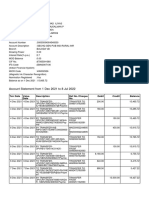

- Account Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVIVEK CHAUHANNo ratings yet

- Kellogg PGCPM B16 BrochureDocument21 pagesKellogg PGCPM B16 BrochureAnkur PandeyNo ratings yet

- Ey Digital Investment ServicesDocument20 pagesEy Digital Investment ServicesAnkur PandeyNo ratings yet

- An Evolutionary Method For Financial Forecasting IDocument18 pagesAn Evolutionary Method For Financial Forecasting IAnkur PandeyNo ratings yet

- Wang W D 2018Document136 pagesWang W D 2018Ankur PandeyNo ratings yet

- March of The Robo-AdvisorsDocument37 pagesMarch of The Robo-AdvisorsAnkur PandeyNo ratings yet

- Seminar On Equity Research Dion Presentation ANMIDocument23 pagesSeminar On Equity Research Dion Presentation ANMIAnkur PandeyNo ratings yet

- Robo Advisor Automated Advice Platform Cgi Patpatia White PaperDocument10 pagesRobo Advisor Automated Advice Platform Cgi Patpatia White PaperAnkur PandeyNo ratings yet

- Accenture Wealth Management Rise of Robo Advice PDFDocument12 pagesAccenture Wealth Management Rise of Robo Advice PDFAnkur PandeyNo ratings yet

- Fin Wealth Epamv5 090516Document33 pagesFin Wealth Epamv5 090516Ankur PandeyNo ratings yet

- Viewpoint Digital Investment Advice September 2016Document16 pagesViewpoint Digital Investment Advice September 2016Ankur PandeyNo ratings yet

- Viewpoint Digital Investment Advice September 2016Document16 pagesViewpoint Digital Investment Advice September 2016Ankur PandeyNo ratings yet

- PWC Top Financial Services Issues 2017Document30 pagesPWC Top Financial Services Issues 2017Ankur PandeyNo ratings yet

- Cohort Analysis 4Document4 pagesCohort Analysis 4Ankur PandeyNo ratings yet

- Classified As Internal Use OnlyDocument2 pagesClassified As Internal Use OnlyIbukunNo ratings yet

- ExtracionDocument84 pagesExtracionTatiana Lozada RodriguezNo ratings yet

- Annex A-2: Sample Conceptual Framework of Information SystemsDocument1 pageAnnex A-2: Sample Conceptual Framework of Information SystemspetiepanNo ratings yet

- Statement of Account: Membership Summary Information For Member # 56228 As of 3/31/20Document4 pagesStatement of Account: Membership Summary Information For Member # 56228 As of 3/31/20Mark HolobaughNo ratings yet

- E-Banking Services of RbiDocument14 pagesE-Banking Services of RbiSrinivasan SrinivasanNo ratings yet

- Kasbit Kasbit Kasbit: Challan No: Challan No: 265412 265412 265412 Challan NoDocument2 pagesKasbit Kasbit Kasbit: Challan No: Challan No: 265412 265412 265412 Challan NoMalik of ChakwalNo ratings yet

- Royal Bank of Canada (RBC), Bridgetown Branch Routing Number, Transit Number, MICR Banks CanadaDocument1 pageRoyal Bank of Canada (RBC), Bridgetown Branch Routing Number, Transit Number, MICR Banks CanadaShannan RichardsNo ratings yet

- Pearson VUE Voucher Sales Order: Bill To: Ship ToDocument1 pagePearson VUE Voucher Sales Order: Bill To: Ship ToNotnow CalmNo ratings yet

- Fin Tech 1 To 30Document428 pagesFin Tech 1 To 30Harshil MehtaNo ratings yet

- Questionnaire On Consumer Awareness and Perception About Credit Cards in IndiaDocument6 pagesQuestionnaire On Consumer Awareness and Perception About Credit Cards in IndiaSARATH KUMAR D100% (1)

- Bank of Maharashtra: One Family One Bank - MahabankDocument17 pagesBank of Maharashtra: One Family One Bank - MahabankShivam Kumar JhaNo ratings yet

- A Study On Consumer Perception Towards Digital Payment: Prakash MDocument12 pagesA Study On Consumer Perception Towards Digital Payment: Prakash MZEDXNo ratings yet

- 1 KM HDFC-impDocument3 pages1 KM HDFC-impHARSHAL MITTALNo ratings yet

- Management Thesis-Ii: Submitted To:-Ms. Smita Kulkarni (Faculty Guide)Document8 pagesManagement Thesis-Ii: Submitted To:-Ms. Smita Kulkarni (Faculty Guide)Ashok KhaireNo ratings yet

- (Read-Only) (Compatibility Mode)Document1 page(Read-Only) (Compatibility Mode)Rintu DasNo ratings yet

- Use Case Document 3Document4 pagesUse Case Document 3Mohd JamalNo ratings yet

- Statement PDFDocument3 pagesStatement PDFParaizo ClubNo ratings yet