You might also like

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (1)

- Integrated Case Study - Anandam Manufacturing CompanyDocument12 pagesIntegrated Case Study - Anandam Manufacturing CompanyAdma Wahyu Dwi Shania100% (1)

- Counterparty Credit Risk: The new challenge for global financial marketsFrom EverandCounterparty Credit Risk: The new challenge for global financial marketsRating: 2.5 out of 5 stars2.5/5 (2)

- The Investment Detective Case StudyDocument3 pagesThe Investment Detective Case StudyItsCj100% (1)

- Spectral FFT Max Ms PDocument17 pagesSpectral FFT Max Ms Phockey66patNo ratings yet

- Chapter7 DigitalData 2Document217 pagesChapter7 DigitalData 2orizaNo ratings yet

- Training On Optical Fiber NetworkDocument96 pagesTraining On Optical Fiber Networkpriyasingh1682100% (1)

- BioavailabilityDocument16 pagesBioavailabilityTyshanna JazzyNicole BariaNo ratings yet

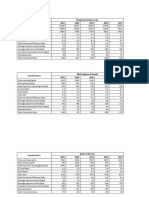

- Current Ratio Currentassets/current LiabiltiesDocument12 pagesCurrent Ratio Currentassets/current LiabiltiespuneetNo ratings yet

- Project Financial RatiosDocument25 pagesProject Financial RatiosParthiv MistryNo ratings yet

- 5 Year Ratio Analysis For RENATA LIMITED PDFDocument47 pages5 Year Ratio Analysis For RENATA LIMITED PDFDhruv singhNo ratings yet

- Assignment 2Document12 pagesAssignment 2Nimra SiddiqueNo ratings yet

- PPT-HDFC Bal & Unbalanced FundDocument11 pagesPPT-HDFC Bal & Unbalanced FundManasi AjithkumarNo ratings yet

- Summer TrainingDocument17 pagesSummer TrainingpallaviNo ratings yet

- Case 4 For AnanlysisDocument2 pagesCase 4 For AnanlysisLaura HNo ratings yet

- Cash Management IN Unimech Seals India PVT LTD: Second ReviewDocument24 pagesCash Management IN Unimech Seals India PVT LTD: Second Reviewwasim musthaqNo ratings yet

- Name: Hira Saqib Rehman Submitted To: Sir Nasir Rasool Section:03 Date: 11 December 2023 Subject: Financial Statement AnalysisDocument18 pagesName: Hira Saqib Rehman Submitted To: Sir Nasir Rasool Section:03 Date: 11 December 2023 Subject: Financial Statement Analysishira saqibNo ratings yet

- Investment Detective AnalyisDocument3 pagesInvestment Detective AnalyisZeeshan RafaqatNo ratings yet

- Fin 302Document19 pagesFin 302aburayhanNo ratings yet

- Vardhman Textile Financial Ratio AnalysisDocument6 pagesVardhman Textile Financial Ratio Analysisnishant singhalNo ratings yet

- Square Pharmaceuticals-Financial AnalysisDocument17 pagesSquare Pharmaceuticals-Financial AnalysisShahid MahmudNo ratings yet

- Earnings based-ROE(s)Document14 pagesEarnings based-ROE(s)Vaishali GuptaNo ratings yet

- Fca B SiddharthDocument12 pagesFca B SiddharthSiddharth SangtaniNo ratings yet

- Comparative Analysis of Npa of Public and Private Sector BanksDocument6 pagesComparative Analysis of Npa of Public and Private Sector Banksiaset123No ratings yet

- DR - Reddy's Ratio AnalysisDocument15 pagesDR - Reddy's Ratio AnalysisDurgaPrasadNo ratings yet

- RatioDocument18 pagesRatioYoosuf Mohamed IrsathNo ratings yet

- Mcdo RatiosDocument3 pagesMcdo RatiosMykaNo ratings yet

- Interpretation R FinalDocument42 pagesInterpretation R FinalrifatbudhwaniNo ratings yet

- Bank Management ProjectDocument20 pagesBank Management ProjectK M Tanveer AhmedNo ratings yet

- Ratio Analysis of Milk PlantDocument26 pagesRatio Analysis of Milk PlantTushar GuptaNo ratings yet

- Ratio Analysis: Liquidity RatiosDocument5 pagesRatio Analysis: Liquidity RatiosVanshGuptaNo ratings yet

- Liquidity RatiosDocument5 pagesLiquidity Ratioskashish AgarwalNo ratings yet

- Fin 254 - Project: Company Name: Meghna Cement Mills LimitedDocument18 pagesFin 254 - Project: Company Name: Meghna Cement Mills LimitedAniruddha RantuNo ratings yet

- Internsip Presentation On Financial Performance Analysis of NCC Bank Limited A Study On Madhunaghat BranchDocument19 pagesInternsip Presentation On Financial Performance Analysis of NCC Bank Limited A Study On Madhunaghat BranchShafayet JamilNo ratings yet

- JS Income FundDocument9 pagesJS Income Fundcoolbouy85No ratings yet

- Analysis and Discussion 6.1 Current RatioDocument86 pagesAnalysis and Discussion 6.1 Current RatioMAYUGAMNo ratings yet

- Ratio Analysis of FSIBL & ICBILDocument12 pagesRatio Analysis of FSIBL & ICBILAmitNo ratings yet

- Berger Paints: Types of Ratios 2012-2013 2011-2012Document7 pagesBerger Paints: Types of Ratios 2012-2013 2011-2012NehaAsifNo ratings yet

- Investment Banking Assignment by MadihaDocument3 pagesInvestment Banking Assignment by MadihamadihaNo ratings yet

- Report-Analysis of Financial SimulationDocument6 pagesReport-Analysis of Financial Simulationariba farrukhNo ratings yet

- Analysis For Dalmia Bharat LTD: Capital StructureDocument4 pagesAnalysis For Dalmia Bharat LTD: Capital Structurejaiminspatel127No ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisAkuma KhanNo ratings yet

- DBBL FinalDocument8 pagesDBBL Finalnaziba aliNo ratings yet

- Solvency Ratios: Name Unit 2014 2015 Maithan Alloys Anjaney Alloys Maithan AlloysDocument3 pagesSolvency Ratios: Name Unit 2014 2015 Maithan Alloys Anjaney Alloys Maithan AlloysANSHULI DMNo ratings yet

- CamelDocument43 pagesCamelsuyashbhatt1980100% (1)

- Stock Valuation FinalDocument8 pagesStock Valuation Finalnaziba aliNo ratings yet

- Assignment FM StarbucksDocument13 pagesAssignment FM StarbucksAmirah AzmiNo ratings yet

- 712-Ratio AnalysisDocument13 pages712-Ratio AnalysisAnarNo ratings yet

- Annual Report 2017Document2 pagesAnnual Report 2017PG93No ratings yet

- 2014 AFS ReviewDocument21 pages2014 AFS ReviewdjokouwmNo ratings yet

- Morning Star Report 20191102055140Document1 pageMorning Star Report 20191102055140Yogi173No ratings yet

- Case Study FM Group 1Document4 pagesCase Study FM Group 1Ini IchiiiNo ratings yet

- A Project Report On Analysis of Financial StatementsDocument15 pagesA Project Report On Analysis of Financial StatementsJaya KumarNo ratings yet

- Results and Analysis: Chapter - TwoDocument2 pagesResults and Analysis: Chapter - TwoShivam KarnNo ratings yet

- Chapter 4Document39 pagesChapter 4Pratikshya KarkiNo ratings yet

- Analysis and Interpretation: Determination of Members of The BankDocument37 pagesAnalysis and Interpretation: Determination of Members of The BankpradeepNo ratings yet

- Electro SteelDocument3 pagesElectro SteelqazxswNo ratings yet

- A Presentation On Alibaba Group's Financial Health AnalysisDocument14 pagesA Presentation On Alibaba Group's Financial Health AnalysisNayeem Ahamed AdorNo ratings yet

- A Study On Financial Performance Analysis of Sakthi Finance LimitedDocument25 pagesA Study On Financial Performance Analysis of Sakthi Finance Limitedwasim musthaqNo ratings yet

- Research Paper On Working Capital Management Made by Satyam KumarDocument3 pagesResearch Paper On Working Capital Management Made by Satyam Kumarsatyam skNo ratings yet

- Ratio Analysis of NCC & UCB Bank (2010-2014)Document17 pagesRatio Analysis of NCC & UCB Bank (2010-2014)سرابوني رحمانNo ratings yet

- A Report On Alibaba Group's Financial Health AnalysisDocument8 pagesA Report On Alibaba Group's Financial Health AnalysisNayeem Ahamed AdorNo ratings yet

- Morning Star Report 20190726102135Document1 pageMorning Star Report 20190726102135YumyumNo ratings yet

- SLES Concentration Effect On The Rheolog TraducidoDocument22 pagesSLES Concentration Effect On The Rheolog TraducidoJose GamezNo ratings yet

- NCERT Solutions For Class 12 Physics Chapter 12 AtomsDocument14 pagesNCERT Solutions For Class 12 Physics Chapter 12 AtomsKritika MishraNo ratings yet

- Electronic - Banking and Customer Satisfaction in Greece - The Case of Piraeus BankDocument15 pagesElectronic - Banking and Customer Satisfaction in Greece - The Case of Piraeus BankImtiaz MasroorNo ratings yet

- Design, Development, Fabrication and Testing of Small Vertical Axis Wind TurbinevDocument4 pagesDesign, Development, Fabrication and Testing of Small Vertical Axis Wind TurbinevEditor IJTSRDNo ratings yet

- Chemical Bonding and Molecular Structure: 2.1. Fundamental Concepts of Chemical BondsDocument47 pagesChemical Bonding and Molecular Structure: 2.1. Fundamental Concepts of Chemical BondsNguyễn Quốc HưngNo ratings yet

- Airbus A319/320/321 Notes: Welcome To The Airbus! Resistance Is Futile, You Will Be AssimilatedDocument128 pagesAirbus A319/320/321 Notes: Welcome To The Airbus! Resistance Is Futile, You Will Be Assimilatedejt01No ratings yet

- Paragon Error Code InformationDocument19 pagesParagon Error Code InformationnenulelelemaNo ratings yet

- Newton First Law of MotionDocument6 pagesNewton First Law of MotionKin ChristineNo ratings yet

- 2003 - Serriano - Form Follows SoftwareDocument21 pages2003 - Serriano - Form Follows SoftwareMina Hazal TasciNo ratings yet

- Fastener NoteDocument8 pagesFastener NoteAmit PrajapatiNo ratings yet

- Inductive Sensor For Temperature Measurement in Induction Heating Applications PDFDocument8 pagesInductive Sensor For Temperature Measurement in Induction Heating Applications PDFNjabulo XoloNo ratings yet

- Btech Ec 7 Sem Digital Image Processing Nec032 2019Document1 pageBtech Ec 7 Sem Digital Image Processing Nec032 2019Deepak SinghNo ratings yet

- 2021 10 11 - Intro ML - InsermDocument41 pages2021 10 11 - Intro ML - Insermpo esperitableNo ratings yet

- Exercise 11ADocument12 pagesExercise 11AAdrian BustamanteNo ratings yet

- Kalman FilterDocument14 pagesKalman FilterNeetaa MunjalNo ratings yet

- SLG Math5 6.3.1 Increasing and Decreasing Functions and The First Derivative Test Part 1Document7 pagesSLG Math5 6.3.1 Increasing and Decreasing Functions and The First Derivative Test Part 1Timothy Tavita23No ratings yet

- Calflo Heat Transfer Fluids Tech DataDocument4 pagesCalflo Heat Transfer Fluids Tech DataKhaled ElsayedNo ratings yet

- Foundations of Nonlinear Algebra (John Perry)Document425 pagesFoundations of Nonlinear Algebra (John Perry)Tao-Wei HuangNo ratings yet

- Zanussi Zou 342 User ManualDocument12 pagesZanussi Zou 342 User Manualadatok2No ratings yet

- DEE APPLIED PHYSICS - Remedial TestDocument2 pagesDEE APPLIED PHYSICS - Remedial TestMilan SasmolNo ratings yet

- Mark Scheme (Results) October 2020: Pearson Edexcel International Advanced Level in Core Mathematics C34 (WMA02) Paper 01Document29 pagesMark Scheme (Results) October 2020: Pearson Edexcel International Advanced Level in Core Mathematics C34 (WMA02) Paper 01nonNo ratings yet

- Hot-Forged 6082 Suspension PartsDocument13 pagesHot-Forged 6082 Suspension Partsfkaram1965No ratings yet

- Tautology and ContradictionDocument10 pagesTautology and ContradictionChristine Tan0% (1)

- C Programming Board Solve PDFDocument12 pagesC Programming Board Solve PDFEstiak Hossain ShaikatNo ratings yet

- Sound Intensity Level CalculationDocument10 pagesSound Intensity Level CalculationvenkateswaranNo ratings yet

- Paper 1research MethodologyDocument2 pagesPaper 1research MethodologySg_manikandanNo ratings yet