You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Commercial Real Estate International Business TrendsDocument21 pagesCommercial Real Estate International Business TrendsNational Association of REALTORS®100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- How Can Cost Segregation Help Minimize Your Tax BurdenDocument6 pagesHow Can Cost Segregation Help Minimize Your Tax BurdenO'Connor AssociateNo ratings yet

- Lehman Futures ModelDocument12 pagesLehman Futures ModelzdfgbsfdzcgbvdfcNo ratings yet

- Session 3 - Valuation Model - AirportsDocument105 pagesSession 3 - Valuation Model - AirportsPrathamesh GoreNo ratings yet

- Business English Kidolgozott TételekDocument60 pagesBusiness English Kidolgozott TételekgiranzoltanNo ratings yet

- The IRS Guidelines For Non-Load Bearing WallsDocument5 pagesThe IRS Guidelines For Non-Load Bearing WallsO'Connor AssociateNo ratings yet

- How To Apply For A Homestead ExemptionDocument6 pagesHow To Apply For A Homestead ExemptionO'Connor AssociateNo ratings yet

- House Flipping - A New Way of IncomeDocument6 pagesHouse Flipping - A New Way of IncomeO'Connor AssociateNo ratings yet

- PRESENTATION - ERE - Tactics For Investors To Drive ROIDocument7 pagesPRESENTATION - ERE - Tactics For Investors To Drive ROIO'Connor AssociateNo ratings yet

- Steps To Protest in Harris CountyDocument7 pagesSteps To Protest in Harris CountyO'Connor AssociateNo ratings yet

- Why O'Connor For Property Tax Reduction?Document7 pagesWhy O'Connor For Property Tax Reduction?O'Connor AssociateNo ratings yet

- Wisconsin Municipal AssessorsDocument48 pagesWisconsin Municipal AssessorsO'Connor AssociateNo ratings yet

- PRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020Document6 pagesPRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020O'Connor AssociateNo ratings yet

- Tax Benefits For Home OwnersDocument7 pagesTax Benefits For Home OwnersO'Connor AssociateNo ratings yet

- 3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationDocument7 pages3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationO'Connor AssociateNo ratings yet

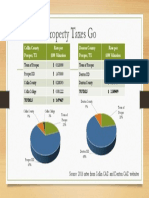

- Where The Property Taxes GoDocument1 pageWhere The Property Taxes GoO'Connor AssociateNo ratings yet

- Top 3 Methods of Valuing Personal PropertyDocument7 pagesTop 3 Methods of Valuing Personal PropertyO'Connor AssociateNo ratings yet

- 25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESDocument8 pages25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESO'Connor AssociateNo ratings yet

- GeorgiaCertificationProgram2017 2018Document2 pagesGeorgiaCertificationProgram2017 2018O'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- Texas Real Estate InspectorDocument25 pagesTexas Real Estate InspectorO'Connor AssociateNo ratings yet

- Tax DeferralDocument1 pageTax DeferralO'Connor AssociateNo ratings yet

- Property Assessment Appeal To The County Board of EqualizationDocument4 pagesProperty Assessment Appeal To The County Board of EqualizationO'Connor AssociateNo ratings yet

- Lincoln Institute of Land Policy's Comparison of 2016 Property TaxesDocument108 pagesLincoln Institute of Land Policy's Comparison of 2016 Property TaxescrainsnewyorkNo ratings yet

- Austin Property Taxpayer Remedies 2017Document1 pageAustin Property Taxpayer Remedies 2017O'Connor AssociateNo ratings yet

- Dallascad - Propertytaxoverview2017Document30 pagesDallascad - Propertytaxoverview2017O'Connor AssociateNo ratings yet

- Cap Rate Rate ReportDocument207 pagesCap Rate Rate ReportO'Connor Associate0% (1)

- Dallas Central Appraisal District 2017 2018Document30 pagesDallas Central Appraisal District 2017 2018O'Connor AssociateNo ratings yet

- Williamson Cad 2017 Rendition General InformationDocument2 pagesWilliamson Cad 2017 Rendition General InformationO'Connor AssociateNo ratings yet

- Montgomery County Exemption AnalysisDocument19 pagesMontgomery County Exemption AnalysisO'Connor AssociateNo ratings yet

- 2016 Annual Report TravisCADDocument41 pages2016 Annual Report TravisCADO'Connor AssociateNo ratings yet

- W C A D: Ise Ounty Ppraisal IstrictDocument43 pagesW C A D: Ise Ounty Ppraisal IstrictO'Connor AssociateNo ratings yet

- Financial Assignment APCDocument6 pagesFinancial Assignment APCNgọc Hồ HoàngNo ratings yet

- Eagle Alpha White PaperDocument30 pagesEagle Alpha White PapertabbforumNo ratings yet

- KotakDocument78 pagesKotakNaMan SeThiNo ratings yet

- What Is SMA - Simple Moving Average - FidelityDocument3 pagesWhat Is SMA - Simple Moving Average - FidelityArundhathi MNo ratings yet

- In The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingDocument62 pagesIn The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingRahmat M JayaatmadjaNo ratings yet

- Group 3 Financial MarketsDocument17 pagesGroup 3 Financial MarketsLady Lou Ignacio LepasanaNo ratings yet

- PDF FinanceDocument25 pagesPDF FinanceThulani NdlovuNo ratings yet

- Soal Try Out Akl 2Document5 pagesSoal Try Out Akl 2Ilham Dwi NoviantoNo ratings yet

- Harvard SEAS Annual Report 2009/10Document24 pagesHarvard SEAS Annual Report 2009/10Harvard School of Enginering and ANo ratings yet

- Investment Portfolio BrochureDocument15 pagesInvestment Portfolio BrochureAndrés RedondoNo ratings yet

- Ch03 17Document3 pagesCh03 17Md Emamul HassanNo ratings yet

- Golden Age of Private MarketsDocument11 pagesGolden Age of Private MarketsDee CeylanNo ratings yet

- 23.10.02 Adriatic HRIS Selection Roadmap & StatusDocument3 pages23.10.02 Adriatic HRIS Selection Roadmap & StatusMateo OstojicNo ratings yet

- Beat The Bank TutorialDocument3 pagesBeat The Bank TutorialgirliepoplollipopNo ratings yet

- Mas Test Bank QuestionDocument3 pagesMas Test Bank QuestionEricka CalaNo ratings yet

- Lara Isabelle Abellar News Presentation Template Fourth QuarterDocument2 pagesLara Isabelle Abellar News Presentation Template Fourth QuarterdreyyNo ratings yet

- FIN4414 SyllabusDocument31 pagesFIN4414 SyllabusQQQQQQNo ratings yet

- Registrar of Companies 28/06/2022: Company DetailsDocument7 pagesRegistrar of Companies 28/06/2022: Company Detailssdafj ndksdngkNo ratings yet

- Chap 5 Capital Market Research in AccountingDocument26 pagesChap 5 Capital Market Research in AccountingGayatri Panirselvam -No ratings yet

- Engineering EconomyDocument26 pagesEngineering Economyrica_escladaNo ratings yet

- NBFC in PakistanDocument3 pagesNBFC in PakistanSalman AsimNo ratings yet

- Chapter VI Financial AspectDocument11 pagesChapter VI Financial AspectTokZhit100% (1)

- Marketing Strategies For Fast-Moving Consumer GoodsDocument4 pagesMarketing Strategies For Fast-Moving Consumer GoodsKrishna MhatreNo ratings yet

- For The Quarter Ended September 30, 2021 (Un-Audited) : Condensed Interim Financial InformationDocument26 pagesFor The Quarter Ended September 30, 2021 (Un-Audited) : Condensed Interim Financial Informationmahnoor javaidNo ratings yet

- Bitcoin Bank America BCBA - About Us - Business PlanDocument2 pagesBitcoin Bank America BCBA - About Us - Business Planmalik_saleem_akbarNo ratings yet

- De Chart of Acounts SKR 03 - EN - 2011Document12 pagesDe Chart of Acounts SKR 03 - EN - 2011Ana CristescuNo ratings yet

- NIKE, Inc. Financial Analysis ExampleDocument4 pagesNIKE, Inc. Financial Analysis ExampleAmruth KurrellaNo ratings yet