You might also like

- Harrington Case - Group CDocument2 pagesHarrington Case - Group CSagar RiazNo ratings yet

- Harrington's CollectionDocument3 pagesHarrington's CollectionSiew_Shen_Kae_3172100% (2)

- Callawaygolfcompanycgc-110330093402 - Callaway Golf Company Case Analysisphpapp02Document22 pagesCallawaygolfcompanycgc-110330093402 - Callaway Golf Company Case Analysisphpapp02Snehal JoshiNo ratings yet

- Harrington Collection Case SummaryDocument3 pagesHarrington Collection Case SummaryManash JRNo ratings yet

- HONY, CIFA, AND ZOOMLION: Creating Value and Strategic Choices in A Dynamic MarketDocument5 pagesHONY, CIFA, AND ZOOMLION: Creating Value and Strategic Choices in A Dynamic MarketJitesh ThakurNo ratings yet

- Factors Affecting Selection of Distribution ChannelDocument2 pagesFactors Affecting Selection of Distribution ChannelDivya SinghNo ratings yet

- Kingfisher Vs Fosters With Porters Five ForcesDocument32 pagesKingfisher Vs Fosters With Porters Five Forcesvenkataswamynath channa100% (5)

- Eco 7Document18 pagesEco 7PreetamNo ratings yet

- Merril Lynch Case StudyDocument3 pagesMerril Lynch Case StudyElda VuciNo ratings yet

- S&D Final ReportDocument9 pagesS&D Final ReportSuddhata ArnabNo ratings yet

- Guidelines SebiDocument19 pagesGuidelines SebiDylan WilcoxNo ratings yet

- Case 4 Harringtom Collection+Financials - Mar2Document11 pagesCase 4 Harringtom Collection+Financials - Mar2Ameen Almohsen100% (1)

- Omni-Channel Retailing: Retail Management - Term PaperDocument11 pagesOmni-Channel Retailing: Retail Management - Term Papernagadeep reddyNo ratings yet

- Raymond James QuestionsDocument1 pageRaymond James QuestionsNikhil ChawlaNo ratings yet

- Session 18 19 Public Goods ExternalitiesDocument50 pagesSession 18 19 Public Goods ExternalitiesMeet SanghviNo ratings yet

- Hill Rom-Vardhan KamatDocument4 pagesHill Rom-Vardhan KamatVardhan KamatNo ratings yet

- Wrightline IncDocument6 pagesWrightline IncdhanrajkamatNo ratings yet

- Takeover & Acquisition: Mergers and Acquisitions and CRDocument11 pagesTakeover & Acquisition: Mergers and Acquisitions and CROmkar PandeyNo ratings yet

- Case 1 Analysis QuestionsDocument1 pageCase 1 Analysis QuestionsDivya RudramoorthyNo ratings yet

- Case Study - LEVI STRAUSS & CO. AND CHINADocument7 pagesCase Study - LEVI STRAUSS & CO. AND CHINAakashkr619No ratings yet

- Charles Schwab & CoDocument11 pagesCharles Schwab & CoAkshit GargNo ratings yet

- Anusha.G: Saranya.BDocument33 pagesAnusha.G: Saranya.BsdaNo ratings yet

- Swosti FoodsDocument6 pagesSwosti FoodsAdarshNo ratings yet

- Introduction To Conscious Capitalism in The MarketplaceDocument9 pagesIntroduction To Conscious Capitalism in The MarketplaceTANVEER AHMEDNo ratings yet

- The Case of The Pricing PredicamentDocument4 pagesThe Case of The Pricing PredicamentSumit BansalNo ratings yet

- Customer Experience Management: 5 Competencies For CX SuccessDocument38 pagesCustomer Experience Management: 5 Competencies For CX SuccessAnonymous VPuGwuNo ratings yet

- Assignment 3Document10 pagesAssignment 3Amit MishraNo ratings yet

- Wikipedia Case Study: Business ModelDocument13 pagesWikipedia Case Study: Business ModelIman FawazNo ratings yet

- Channel ConflictDocument37 pagesChannel Conflictनवीण दत्तNo ratings yet

- HEWLETT PACKARD Computer Systems Organization Selling To Enterprise CustomersDocument16 pagesHEWLETT PACKARD Computer Systems Organization Selling To Enterprise CustomersAakanksha Gulabdhar MishraNo ratings yet

- The Nirdosh CaseDocument2 pagesThe Nirdosh CaseTatsat PandeyNo ratings yet

- American Well Case StudyDocument4 pagesAmerican Well Case StudyAnuj ChandaNo ratings yet

- Chapter 9Document16 pagesChapter 9BenjaNo ratings yet

- Hiring Without FiringDocument3 pagesHiring Without FiringKaran BaruaNo ratings yet

- Assignment 1: 1) Identify "Quick Wins" As A Result of A Detailed Understanding of The Economics of Your New CompanyDocument5 pagesAssignment 1: 1) Identify "Quick Wins" As A Result of A Detailed Understanding of The Economics of Your New CompanyjyNiNo ratings yet

- Canadian Blood ServicesDocument5 pagesCanadian Blood ServicesAbhinav ChaudharyNo ratings yet

- Dove Shampoo: Submitted byDocument28 pagesDove Shampoo: Submitted byShefali SinghNo ratings yet

- Fischer-Price Toys, Inc.: Group 5Document5 pagesFischer-Price Toys, Inc.: Group 5Arshil RizviNo ratings yet

- Pricing To Capture ValueDocument30 pagesPricing To Capture ValueArshad RS100% (1)

- Analysis 383145150Document6 pagesAnalysis 383145150Poornika AwasthiNo ratings yet

- BGS ModelsDocument24 pagesBGS Modelsprasannamurthy100% (1)

- Howard Schultz: Building Starbucks Community Section 2 Group 4Document7 pagesHoward Schultz: Building Starbucks Community Section 2 Group 4siva mNo ratings yet

- Talk To ChuckDocument6 pagesTalk To ChuckStuti Sethi0% (1)

- Thomas Green L05 Case StudyDocument6 pagesThomas Green L05 Case StudyGreggi RizkyNo ratings yet

- Case Summary - Bhavsar's Herbal Smoking DeviceDocument1 pageCase Summary - Bhavsar's Herbal Smoking DeviceskthakreNo ratings yet

- Infosys's Relationship Scorecard: Measuring Transformational RelationshipsDocument6 pagesInfosys's Relationship Scorecard: Measuring Transformational RelationshipsVijeta GourNo ratings yet

- People Management Fiasco at HMSIDocument45 pagesPeople Management Fiasco at HMSIPrem GiriNo ratings yet

- Motivate Sales PersonDocument2 pagesMotivate Sales PersonSameer MiraniNo ratings yet

- Official Finocontrol Brochure 2020Document23 pagesOfficial Finocontrol Brochure 2020pavan kalyan50% (2)

- Harvard-Sup Chain SylDocument23 pagesHarvard-Sup Chain SylPrashanth CecilNo ratings yet

- MARK1012 CaseDocument5 pagesMARK1012 CasemiapNo ratings yet

- When Workers Rate The BossDocument3 pagesWhen Workers Rate The BossSHIVANGI MAHAJAN PGP 2021-23 BatchNo ratings yet

- Augustine Medical CaseDocument2 pagesAugustine Medical Casemsmithers6No ratings yet

- Bird's EyeDocument4 pagesBird's EyePranav AnandNo ratings yet

- UtvDocument7 pagesUtvTan KailinNo ratings yet

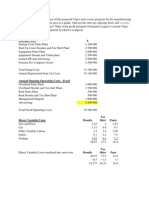

- Bergerac Slides (10.29.14)Document8 pagesBergerac Slides (10.29.14)Chuqiao Wang100% (1)

- Ans 5Document2 pagesAns 5Rida Khan100% (2)

- Objectives of Cost-Volume-Profit AnalysisDocument7 pagesObjectives of Cost-Volume-Profit AnalysisAnonNo ratings yet

- Chapter FourDocument10 pagesChapter Fourliyneh mebrahituNo ratings yet

- Business Math - Q1 - Week 6 - Module 4 - MARGINS AND DISCOUNTS REPRODUCTIONDocument20 pagesBusiness Math - Q1 - Week 6 - Module 4 - MARGINS AND DISCOUNTS REPRODUCTIONJhudiel Dela ConcepcionNo ratings yet

- Woven - Carpets Made From Weaving Fibers or Yarn in and Out To Make A ContinuousDocument5 pagesWoven - Carpets Made From Weaving Fibers or Yarn in and Out To Make A ContinuousfdinglasanNo ratings yet

- Poodle - Pug - Rottweiler Pattern - Heather Gibbs 2Document9 pagesPoodle - Pug - Rottweiler Pattern - Heather Gibbs 2Tatu AradiNo ratings yet

- Mańczak - A Practical Grammar of EnglishDocument141 pagesMańczak - A Practical Grammar of Englisha.kubrak100% (1)

- Achievers B1 Festival Boxing DayDocument1 pageAchievers B1 Festival Boxing DayJaritza JaAnNo ratings yet

- Get Involved American Edition Level 1 Teacher S Edition Unit 4Document9 pagesGet Involved American Edition Level 1 Teacher S Edition Unit 4alexandracarolinasassanoalcantNo ratings yet

- Brown, Meghan (The Pliant Girls)Document98 pagesBrown, Meghan (The Pliant Girls)Tyler DubucNo ratings yet

- Iso 13994 2005 en PDFDocument8 pagesIso 13994 2005 en PDFrenny krisnawatiNo ratings yet

- Louis VittonDocument1 pageLouis Vittonjojie dadorNo ratings yet

- Distressed Jeans For WomensDocument7 pagesDistressed Jeans For WomensJeans BoutiqueNo ratings yet

- CombinationsDocument44 pagesCombinationsStephen Jayde CagadasNo ratings yet

- Cumulative Tests B - Answer Keys Units 1-5: Grammar Use of EnglishDocument6 pagesCumulative Tests B - Answer Keys Units 1-5: Grammar Use of EnglishCamilla GazizovaNo ratings yet

- Fabric and Garment Designing TechniqueDocument28 pagesFabric and Garment Designing TechniqueMae-maeGarmaNo ratings yet

- Secrets of The CircusDocument2 pagesSecrets of The CircusEmma BerwickNo ratings yet

- Answers Fourcorners 3 Work Book 1 12Document14 pagesAnswers Fourcorners 3 Work Book 1 12Tabatha RosasNo ratings yet

- Chuky Malo - PDF Versión 1Document28 pagesChuky Malo - PDF Versión 1rocio100% (2)

- PRIMARK To NIGERIA Group 12 ENG7144 - International Business & Marketing PresentationDocument77 pagesPRIMARK To NIGERIA Group 12 ENG7144 - International Business & Marketing PresentationAdetomilola AduNo ratings yet

- Care Labelling StandardDocument9 pagesCare Labelling Standardภูมิภักดิ์ ธรรมวิหารคุณNo ratings yet

- PSP Dan Konstruksi Alat Tes - Ristin Dewi Nolia - 181810047Document3 pagesPSP Dan Konstruksi Alat Tes - Ristin Dewi Nolia - 181810047Jeany AsterlitaNo ratings yet

- SSC JE Mechanical Oct 9 2023 Shift 2Document74 pagesSSC JE Mechanical Oct 9 2023 Shift 2arnabhsahu96No ratings yet

- Sonnets 16 and 18 by Shakespeare and MoreDocument3 pagesSonnets 16 and 18 by Shakespeare and MoreJohan TadlasNo ratings yet

- Future Tense With "Going To" - What Is Sara Going To Do?Document14 pagesFuture Tense With "Going To" - What Is Sara Going To Do?ludy genid33% (3)

- Offenlegung Von Hauptproduktionssta Tten Fu R Textilien Und SchuheDocument33 pagesOffenlegung Von Hauptproduktionssta Tten Fu R Textilien Und Schuhetesting accountNo ratings yet

- AIR JORDANS InfoDocument4 pagesAIR JORDANS InfoMayankNo ratings yet

- 1upcrochet - MewDocument8 pages1upcrochet - Mewliligkjj100% (2)

- Atelier Clandestin Villager GeneratorDocument6 pagesAtelier Clandestin Villager GeneratorEmma PileNo ratings yet

- The Impact of The Fashion Industry in The EnvironmentDocument4 pagesThe Impact of The Fashion Industry in The EnvironmentBeatriz Coutinho de AlmeidaNo ratings yet

- CHANDNIDocument2 pagesCHANDNISonia KhileriNo ratings yet

- StarWars ArmorsDocument11 pagesStarWars ArmorsMac AvityNo ratings yet

- Describing People: A Descriptive Composition About A Person Should Consist ofDocument3 pagesDescribing People: A Descriptive Composition About A Person Should Consist ofabril iñon rukavinaNo ratings yet

- Demonstrative PronounsDocument2 pagesDemonstrative PronounsLamanNo ratings yet

- High Road Leadership: Bringing People Together in a World That DividesFrom EverandHigh Road Leadership: Bringing People Together in a World That DividesNo ratings yet

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverFrom EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverRating: 4.5 out of 5 stars4.5/5 (186)

- Summary of Noah Kagan's Million Dollar WeekendFrom EverandSummary of Noah Kagan's Million Dollar WeekendRating: 5 out of 5 stars5/5 (2)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4.5 out of 5 stars4.5/5 (2)

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobFrom EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobRating: 4.5 out of 5 stars4.5/5 (37)

- Spark: How to Lead Yourself and Others to Greater SuccessFrom EverandSpark: How to Lead Yourself and Others to Greater SuccessRating: 4.5 out of 5 stars4.5/5 (132)

- The First Minute: How to start conversations that get resultsFrom EverandThe First Minute: How to start conversations that get resultsRating: 4.5 out of 5 stars4.5/5 (57)

- How to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersFrom EverandHow to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersRating: 4.5 out of 5 stars4.5/5 (95)

- Leadership Skills that Inspire Incredible ResultsFrom EverandLeadership Skills that Inspire Incredible ResultsRating: 4.5 out of 5 stars4.5/5 (11)

- Scaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0From EverandScaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Rating: 5 out of 5 stars5/5 (2)

- The 7 Habits of Highly Effective PeopleFrom EverandThe 7 Habits of Highly Effective PeopleRating: 4 out of 5 stars4/5 (2566)

- Billion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsFrom EverandBillion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsRating: 4.5 out of 5 stars4.5/5 (52)

- The Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderFrom EverandThe Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderNo ratings yet

- The Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceFrom EverandThe Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceRating: 5 out of 5 stars5/5 (22)

- Good to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tFrom EverandGood to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tRating: 4.5 out of 5 stars4.5/5 (63)

- Unlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsFrom EverandUnlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsRating: 4.5 out of 5 stars4.5/5 (28)

- 300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionFrom Everand300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionRating: 5 out of 5 stars5/5 (1)

- The Introverted Leader: Building on Your Quiet StrengthFrom EverandThe Introverted Leader: Building on Your Quiet StrengthRating: 4.5 out of 5 stars4.5/5 (35)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- 7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthFrom Everand7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthRating: 5 out of 5 stars5/5 (52)

- Summary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisFrom EverandSummary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisRating: 4.5 out of 5 stars4.5/5 (3)

- Superminds: The Surprising Power of People and Computers Thinking TogetherFrom EverandSuperminds: The Surprising Power of People and Computers Thinking TogetherRating: 3.5 out of 5 stars3.5/5 (7)

- Think Like Amazon: 50 1/2 Ideas to Become a Digital LeaderFrom EverandThink Like Amazon: 50 1/2 Ideas to Become a Digital LeaderRating: 4.5 out of 5 stars4.5/5 (60)

- Summary of Marshall Goldsmith & Mark Reiter's What Got You Here Won't Get You ThereFrom EverandSummary of Marshall Goldsmith & Mark Reiter's What Got You Here Won't Get You ThereRating: 3 out of 5 stars3/5 (2)

- The 7 Habits of Highly Effective People: 30th Anniversary EditionFrom EverandThe 7 Habits of Highly Effective People: 30th Anniversary EditionRating: 5 out of 5 stars5/5 (337)

- Management Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowFrom EverandManagement Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowRating: 4.5 out of 5 stars4.5/5 (27)

- The Manager's Path: A Guide for Tech Leaders Navigating Growth and ChangeFrom EverandThe Manager's Path: A Guide for Tech Leaders Navigating Growth and ChangeRating: 4.5 out of 5 stars4.5/5 (99)