You might also like

- North Korea Conflict: International Industry Research and Economics DepartmentDocument9 pagesNorth Korea Conflict: International Industry Research and Economics DepartmentPeter PandaNo ratings yet

- 2017 MIP Report China Online EdtechDocument29 pages2017 MIP Report China Online EdtechPeter PandaNo ratings yet

- What Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostDocument6 pagesWhat Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostPeter PandaNo ratings yet

- BVCA Guide To Corporate Venture CapitalDocument16 pagesBVCA Guide To Corporate Venture CapitalPeter PandaNo ratings yet

- IO Ethanol 2018 enDocument7 pagesIO Ethanol 2018 enPeter PandaNo ratings yet

- Characteristics: C5 Petrochemical ProductDocument3 pagesCharacteristics: C5 Petrochemical ProductPeter PandaNo ratings yet

- News Articles 2018-01-16 The-Flow-OfDocument5 pagesNews Articles 2018-01-16 The-Flow-OfPeter PandaNo ratings yet

- Role Play Scenario 1:: Group No. .Document1 pageRole Play Scenario 1:: Group No. .Peter PandaNo ratings yet

- mati08-2537 มติคณะกรรมการสิ่งแวดล้อมDocument4 pagesmati08-2537 มติคณะกรรมการสิ่งแวดล้อมPeter PandaNo ratings yet

- Christie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostDocument3 pagesChristie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostPeter PandaNo ratings yet

- Thai NessDocument17 pagesThai NessPeter PandaNo ratings yet

- Shell Marine Imo BrochureDocument6 pagesShell Marine Imo BrochurePeter PandaNo ratings yet

- Evaluation Form For MassageDocument1 pageEvaluation Form For MassagePeter PandaNo ratings yet

- LucerneDocument52 pagesLucernePeter PandaNo ratings yet

- Brexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionDocument17 pagesBrexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionPeter PandaNo ratings yet

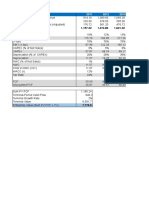

- Total Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Document6 pagesTotal Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Peter PandaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Competitive AnalysisDocument10 pagesCompetitive AnalysisVikrant SinghNo ratings yet

- Quiz 1: Spring 1998: Business Average Beta Average D/E RatioDocument43 pagesQuiz 1: Spring 1998: Business Average Beta Average D/E RatioDenisse SánchezNo ratings yet

- Function of Commercial Banks in IndonesiaDocument4 pagesFunction of Commercial Banks in IndonesiaAbahLatifCanvasmasNo ratings yet

- Social Investment ManualDocument56 pagesSocial Investment ManualWorld Economic Forum82% (66)

- Chapter 4Document28 pagesChapter 4Hitesh BhargavaNo ratings yet

- Consolidated Accounts QuestionsDocument10 pagesConsolidated Accounts QuestionsGiedrius SatkauskasNo ratings yet

- Zerodha ComDocument25 pagesZerodha ComBalakrishna BoyapatiNo ratings yet

- Assignment 2 24 August 2017Document6 pagesAssignment 2 24 August 2017kanteshk7No ratings yet

- A Comparative Analysis of Life InsuranceDocument41 pagesA Comparative Analysis of Life InsuranceDibyaRanjanBeheraNo ratings yet

- Term Loan ProcedureDocument8 pagesTerm Loan ProcedureSunita More0% (2)

- Form S11 For Subscribers Having A Tier I Account Without A PRAN Card - SG T II A PDFDocument5 pagesForm S11 For Subscribers Having A Tier I Account Without A PRAN Card - SG T II A PDFSudhir ShastriNo ratings yet

- 1 Internship Report MCBDocument68 pages1 Internship Report MCBAbdullah Afzal100% (1)

- Tanaka 2Document15 pagesTanaka 2Firani Reza ByaNo ratings yet

- Disha Publication AFCAT Ratio Proportion & Variations PDFDocument23 pagesDisha Publication AFCAT Ratio Proportion & Variations PDFAnonymous sQ0klTOzglNo ratings yet

- Answers To Practice Questions: Capital Budgeting and RiskDocument8 pagesAnswers To Practice Questions: Capital Budgeting and Risksharktale2828No ratings yet

- Resort Operations Chapter 2Document20 pagesResort Operations Chapter 2Aaron Black100% (2)

- 1Document21 pages1Joshua S MjinjaNo ratings yet

- Corp Tax OutlineDocument86 pagesCorp Tax Outlinebrooklandsteel100% (1)

- Msu Bba Vadodara.: Report On Jhaveri Securities Pvt. LTDDocument16 pagesMsu Bba Vadodara.: Report On Jhaveri Securities Pvt. LTDShalin PatelNo ratings yet

- ch24 Presentation and Disclosure in FinancialReportingDocument74 pagesch24 Presentation and Disclosure in FinancialReportingIma Listyaningrum100% (1)

- Standalone Financial Results For March 31, 2016 (Result)Document3 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Financial Management - Brigham Chapter 3Document4 pagesFinancial Management - Brigham Chapter 3Fazli AleemNo ratings yet

- Chapter 3 Corporate GovernanceDocument25 pagesChapter 3 Corporate GovernanceOmer UddinNo ratings yet

- 5.practice Set Ibps Cwe Po-IVDocument19 pages5.practice Set Ibps Cwe Po-IVgopalraja732No ratings yet

- PUSEQF Prospectus SC PDFDocument43 pagesPUSEQF Prospectus SC PDFIdo Firadyanie MarcelloNo ratings yet

- News of The Day: Attention To Our Distinguished SubscribersDocument13 pagesNews of The Day: Attention To Our Distinguished Subscriberssmiley346No ratings yet

- Chapter 12 (Income Tax On Corporations)Document10 pagesChapter 12 (Income Tax On Corporations)libraolrackNo ratings yet

- University of Professional Studies Accra-Upsa: Project Work PresentationDocument16 pagesUniversity of Professional Studies Accra-Upsa: Project Work Presentationjames Nartey Agbo100% (1)

- Chapter 3Document38 pagesChapter 3akmal_07No ratings yet

- 2 MasDocument15 pages2 MasJames Louis BarcenasNo ratings yet