You might also like

- FR Additional Questions For Practice - Dec 21 ExamsDocument59 pagesFR Additional Questions For Practice - Dec 21 ExamsmNo ratings yet

- FR (New) Suggested Ans CA Final Jan 21Document33 pagesFR (New) Suggested Ans CA Final Jan 21ritz meshNo ratings yet

- Index MCQ Booklet: Audit MCQ Compiler by Shubham Keswani Shubham KeswaniDocument108 pagesIndex MCQ Booklet: Audit MCQ Compiler by Shubham Keswani Shubham Keswaniasd100% (2)

- AIR1CA Mock Test Series - CA Final May 2020Document2 pagesAIR1CA Mock Test Series - CA Final May 2020Ñïkêţ Bäûðhå0% (2)

- Audit MCQDocument299 pagesAudit MCQVamseenath N RNo ratings yet

- Additional Questions in FR (Ed 5 To Ed 6)Document67 pagesAdditional Questions in FR (Ed 5 To Ed 6)shivam kukrejaNo ratings yet

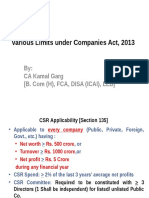

- Various Limits Under Companies Act, 2013 (CA Final)Document61 pagesVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedNo ratings yet

- AUDIT CA INTERMEDIATE Revision For May 19 NotesDocument68 pagesAUDIT CA INTERMEDIATE Revision For May 19 Notesdiya100% (1)

- The Ultimate Solution - MCQ Booklet: Author's MessageDocument53 pagesThe Ultimate Solution - MCQ Booklet: Author's MessageVishal VermaNo ratings yet

- 01A Audit of Limited CompaniesDocument34 pages01A Audit of Limited CompaniesSai VardhanNo ratings yet

- CA INTER AUDIT MCQ CA Ravi AgarwalDocument186 pagesCA INTER AUDIT MCQ CA Ravi AgarwalHarshit BahetyNo ratings yet

- FR Concept Notes For Nov 22 ExamsDocument223 pagesFR Concept Notes For Nov 22 ExamsMonu RaiNo ratings yet

- Case Studies Compilation (Company Law)Document485 pagesCase Studies Compilation (Company Law)SANTHOSH KUMAR T MNo ratings yet

- @CACell CA Inter Audit Correct OR Incorrect Nov22Document28 pages@CACell CA Inter Audit Correct OR Incorrect Nov22Srushti Agarwal100% (1)

- Audit of Different Types of Entity Summary Notes by CA Kapil GoyalDocument24 pagesAudit of Different Types of Entity Summary Notes by CA Kapil GoyalDrake DDNo ratings yet

- SFM Concept Notes For May 23 ExamsDocument146 pagesSFM Concept Notes For May 23 ExamsSonia Shah100% (1)

- Inter SA Compact BookDocument46 pagesInter SA Compact Bookvishnuverma0% (1)

- Cma ProspectusDocument68 pagesCma ProspectusDeepak NimmojiNo ratings yet

- (Sample) Law Bomb 2.0 (CA Final) by CA Ravi AgarwalDocument11 pages(Sample) Law Bomb 2.0 (CA Final) by CA Ravi AgarwalRishabh RudraNo ratings yet

- FR Concept Notes For May 22 ExamsDocument217 pagesFR Concept Notes For May 22 ExamssanilNo ratings yet

- GST PRACTICE SET - 6th EDITION - SET JDocument6 pagesGST PRACTICE SET - 6th EDITION - SET JGANESH KUNJAPPA POOJARINo ratings yet

- CA Final IDT Amendments May21 Tharun Raj @CA - Study - NotesDocument57 pagesCA Final IDT Amendments May21 Tharun Raj @CA - Study - NotesKrishna Rama Theertha KoritalaNo ratings yet

- III Sem BCOM Corporate Accounting SSM 1-5 ModulesDocument148 pagesIII Sem BCOM Corporate Accounting SSM 1-5 ModulesSinghan SNo ratings yet

- 2b CA Intermediate GST Question Bank 8th Edition Dec 2021 ExamDocument232 pages2b CA Intermediate GST Question Bank 8th Edition Dec 2021 ExamSATHYA SAINATH MNo ratings yet

- FR V2 Concept Notes by Pratik Jagati @mission - CA - FinalDocument131 pagesFR V2 Concept Notes by Pratik Jagati @mission - CA - FinalVrinda KNo ratings yet

- FR QB Black&WhiteDocument767 pagesFR QB Black&WhitesarikamuthyalaNo ratings yet

- CA ZAMBIA PROGRAMME EXAM CONSOLIDATED GROUP STATEMENTDocument176 pagesCA ZAMBIA PROGRAMME EXAM CONSOLIDATED GROUP STATEMENTinnocent moonoNo ratings yet

- CA INTERMEDIATE Financial Management Compiler QuestionsDocument295 pagesCA INTERMEDIATE Financial Management Compiler QuestionsVINAY SHARMANo ratings yet

- Pratik Jagati Question BankDocument420 pagesPratik Jagati Question BankRoshan PoudelNo ratings yet

- Fullcoverageoficaistudymat Chapterwise&Attemptwiseq&Asbifurcation Includesallillustrations, Theory&Practicalq&As Allpastpapers, Mtps&RtpsincludedDocument633 pagesFullcoverageoficaistudymat Chapterwise&Attemptwiseq&Asbifurcation Includesallillustrations, Theory&Practicalq&As Allpastpapers, Mtps&RtpsincludedAS & AssociatesNo ratings yet

- Cost & FMDocument4 pagesCost & FMSurajNo ratings yet

- Ca Final SFM (New) Chapterwise Abc & Marks Analysis - Ca Ravi AgarwalDocument2 pagesCa Final SFM (New) Chapterwise Abc & Marks Analysis - Ca Ravi AgarwalG KNo ratings yet

- FM Rocks Book by CA Swapnil PatniDocument124 pagesFM Rocks Book by CA Swapnil Patniraj bawaNo ratings yet

- Standards by Sanidhya Saraf Serial 1 5Document85 pagesStandards by Sanidhya Saraf Serial 1 5rahul gobburiNo ratings yet

- CA Inter Paper 1 All Question PapersDocument205 pagesCA Inter Paper 1 All Question PapersNivedita SharmaNo ratings yet

- CA Inter Costing Practical Questions With SolutionsDocument311 pagesCA Inter Costing Practical Questions With SolutionsAnkit KumarNo ratings yet

- Inter Cost 2Document27 pagesInter Cost 2Anirudha SatheNo ratings yet

- CA Inter Cost Blast From The Past PDFDocument83 pagesCA Inter Cost Blast From The Past PDFAashish TiwariNo ratings yet

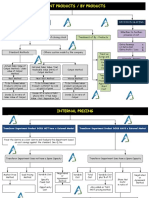

- Joint Products / by Products: Accounting Decision MakingDocument16 pagesJoint Products / by Products: Accounting Decision MakingKaran KashyapNo ratings yet

- Contract Act One Day Before Notes - 20340986 - 2023 - 06!24!20 - 15Document16 pagesContract Act One Day Before Notes - 20340986 - 2023 - 06!24!20 - 15tiwaripranay60No ratings yet

- Ch-2 Audit PlanningDocument3 pagesCh-2 Audit PlanningSavya Sachi100% (1)

- Inp 2234 Tax Question PaperDocument11 pagesInp 2234 Tax Question PaperAnshit BahediaNo ratings yet

- CA Final Direct Tax Flow Charts May 2017 2SDMBZA2Document92 pagesCA Final Direct Tax Flow Charts May 2017 2SDMBZA2Meet Mehta100% (1)

- CA Final May 2020 Question Bank PDFDocument1,624 pagesCA Final May 2020 Question Bank PDFAjay JosephNo ratings yet

- Final Accounts QuestionsDocument6 pagesFinal Accounts QuestionsGandharva Shankara Murthy100% (1)

- CA Inter GST Marathon NotesDocument133 pagesCA Inter GST Marathon NotesNandan Gambhir100% (1)

- Expected QuestionsDocument168 pagesExpected QuestionskaushikagarwalNo ratings yet

- Out of Charge Copy: Indian CustomsDocument6 pagesOut of Charge Copy: Indian CustomsaaanathanNo ratings yet

- M & A Solutions PDFDocument28 pagesM & A Solutions PDFayushmehtha7No ratings yet

- 5th Semester Bcom Auditing Notes Blotia EditDocument214 pages5th Semester Bcom Auditing Notes Blotia EditKnowledge NiwasNo ratings yet

- 03c GST Question Bank CA Inter June 2020 Exam 5th EditionDocument178 pages03c GST Question Bank CA Inter June 2020 Exam 5th Editionk kakkarNo ratings yet

- Accounts Complier (QB) @mission - CA - InterDocument350 pagesAccounts Complier (QB) @mission - CA - Intershivangi sharma0907100% (1)

- The Ultimate Solution Summary Book Nov'23Document225 pagesThe Ultimate Solution Summary Book Nov'23r79qwkxcfj100% (1)

- AOADocument15 pagesAOAhappydaysshree2291No ratings yet

- Ooin@A/Sparchansraj: S.P.A.R.CDocument155 pagesOoin@A/Sparchansraj: S.P.A.R.CadsaNo ratings yet

- BB SIR QUESTION BANK DT May 22Document216 pagesBB SIR QUESTION BANK DT May 22Srushti AgarwalNo ratings yet

- 5 6057497367471456479Document59 pages5 6057497367471456479Sachin Dixit100% (1)

- © The Institute of Chartered Accountants of IndiaDocument0 pages© The Institute of Chartered Accountants of IndiaamitmdeshpandeNo ratings yet

- Paper - 2: Strategic Financial Management Questions Project Planning and Capital BudgetingDocument33 pagesPaper - 2: Strategic Financial Management Questions Project Planning and Capital BudgetingShyam virsinghNo ratings yet

- Paper - 2: Strategic Financial Management Questions Risk Analysis in Capital BudgetingDocument25 pagesPaper - 2: Strategic Financial Management Questions Risk Analysis in Capital BudgetingJINENDRA JAINNo ratings yet

- CPA Registration Form 2015Document4 pagesCPA Registration Form 2015Tahsin RazaNo ratings yet

- WildFinMan8e Ch01 PPTDocument60 pagesWildFinMan8e Ch01 PPTWaqar AmjadNo ratings yet

- 10th Physics Notes-1Document95 pages10th Physics Notes-1Waqar AmjadNo ratings yet

- WQTDocument12 pagesWQTWaqar AmjadNo ratings yet

- Attachment 1571841304Document22 pagesAttachment 1571841304Waqar AmjadNo ratings yet

- 100 General KnowledgeDocument5 pages100 General KnowledgeNoumanAwanNo ratings yet

- Attachment 1571841304Document22 pagesAttachment 1571841304Waqar AmjadNo ratings yet

- 5289 Islamic Feminism A Public Lecture byDocument14 pages5289 Islamic Feminism A Public Lecture byWaqar AmjadNo ratings yet

- Central College Multan Test No 7Document1 pageCentral College Multan Test No 7Waqar AmjadNo ratings yet

- Chapter 8 Solutions GitmanDocument22 pagesChapter 8 Solutions GitmanCat Valentine100% (3)

- Attachment 1571841304Document22 pagesAttachment 1571841304Waqar AmjadNo ratings yet

- 100 General KnowledgeDocument5 pages100 General KnowledgeNoumanAwanNo ratings yet

- Welcome To ExamDocument15 pagesWelcome To ExamWaqar AmjadNo ratings yet

- 02 Leveraging Employee Engagement For Competitive Advantage 2Document12 pages02 Leveraging Employee Engagement For Competitive Advantage 2faisalsiddique100% (2)

- Central College Accounting PaperDocument2 pagesCentral College Accounting PaperWaqar AmjadNo ratings yet

- 101 Math Short PDFDocument21 pages101 Math Short PDFHarish AttriNo ratings yet

- Formulating Service Marketing Strategy For Education Service SectorDocument15 pagesFormulating Service Marketing Strategy For Education Service SectorSavin Nain0% (1)

- F2 FMA Study Text Sample ChapterDocument32 pagesF2 FMA Study Text Sample ChapterWaqar AmjadNo ratings yet

- Accounting Basics and PrinciplesDocument20 pagesAccounting Basics and PrinciplesWaqar AmjadNo ratings yet

- Papar EngDocument1 pagePapar EngWaqar AmjadNo ratings yet

- 18 65Document2 pages18 65Waqar AmjadNo ratings yet

- Everyday Science 100 MCQS Part 1Document14 pagesEveryday Science 100 MCQS Part 1Attaullah MalakandNo ratings yet

- Caf05 STDocument321 pagesCaf05 STWaqar Amjad50% (2)

- Income Tax CalculationsDocument1 pageIncome Tax CalculationsWaqar AmjadNo ratings yet

- Assignment Week 7Document9 pagesAssignment Week 7Waqar AmjadNo ratings yet

- Future Value of an Ordinary Annuity TableDocument1 pageFuture Value of an Ordinary Annuity TableWaqar AmjadNo ratings yet

- ACCT Discussion Module 15 HWDocument2 pagesACCT Discussion Module 15 HWWaqar AmjadNo ratings yet

- Assignmen Week 422Document5 pagesAssignmen Week 422Waqar AmjadNo ratings yet

- VW Group's Innovative Marketing Strategies Through the YearsDocument16 pagesVW Group's Innovative Marketing Strategies Through the YearsWaqar AmjadNo ratings yet

- Assignmen Week 422Document5 pagesAssignmen Week 422Waqar AmjadNo ratings yet

- Fidelity Magellan Fund (FMAGX) : No Transaction Fee (1/31/2006-1/31/2016)Document3 pagesFidelity Magellan Fund (FMAGX) : No Transaction Fee (1/31/2006-1/31/2016)wesleybean9381No ratings yet

- L1 R50 HY NotesDocument7 pagesL1 R50 HY Notesayesha ansariNo ratings yet

- 46370bosfinal p2 cp6 PDFDocument85 pages46370bosfinal p2 cp6 PDFgouri khanduallNo ratings yet

- FAC202 JetAirwaysDocument21 pagesFAC202 JetAirwaysNeha ReddyNo ratings yet

- PGP 2021-23 Term 3 Financial Derivatives: An Assignment OnDocument12 pagesPGP 2021-23 Term 3 Financial Derivatives: An Assignment Onnischal mathurNo ratings yet

- Marriott Corporation Cost of Capital Case AnalysisDocument11 pagesMarriott Corporation Cost of Capital Case Analysisjen1861269% (13)

- Fundamentals of Financial Management 14th Edition Brigham Solutions ManualDocument38 pagesFundamentals of Financial Management 14th Edition Brigham Solutions Manualjeanbarnettxv9v100% (8)

- Performance Analysis of Mid Cap Mutual Funds in India (2014 To 2023)Document9 pagesPerformance Analysis of Mid Cap Mutual Funds in India (2014 To 2023)International Journal of Innovative Science and Research TechnologyNo ratings yet

- Ca Final SFM Test Paper QuestionDocument8 pagesCa Final SFM Test Paper Question1620tanyaNo ratings yet

- 2830203-Security Analysis and Portfolio ManagementDocument2 pages2830203-Security Analysis and Portfolio ManagementbhumikajasaniNo ratings yet

- Risk, Return, and The Capital Asset Pricing ModelDocument52 pagesRisk, Return, and The Capital Asset Pricing ModelFaryal ShahidNo ratings yet

- Chapter - 11 Portfolio ManagementDocument5 pagesChapter - 11 Portfolio ManagementD2NNo ratings yet

- Sharpe, Treynor and Jenson SumDocument2 pagesSharpe, Treynor and Jenson SumNikita ShekhawatNo ratings yet

- A Report On Capital Structure of BHELDocument17 pagesA Report On Capital Structure of BHELRAVI RAUSHAN JHANo ratings yet

- Sharpe Treynor N JensenDocument4 pagesSharpe Treynor N JensenjustsatyaNo ratings yet

- Fairness Opinion on Danaher's CHF 17.10 per Share Offer for Nobel BiocareDocument35 pagesFairness Opinion on Danaher's CHF 17.10 per Share Offer for Nobel BiocareCommodityNo ratings yet

- Kaplan Constructed Response Workshop on Equity and Fixed Income Portfolio ManagementDocument16 pagesKaplan Constructed Response Workshop on Equity and Fixed Income Portfolio Managementhammad haqNo ratings yet

- Optimal risky portfolios and problem setsDocument13 pagesOptimal risky portfolios and problem setsBiloni KadakiaNo ratings yet

- Is Beta Dead or AliveDocument4 pagesIs Beta Dead or Aliveahmad faisolNo ratings yet

- BA1727 - SECURITY ANALYSIS & PORTFOLIO MANAGEMENT Question BankDocument13 pagesBA1727 - SECURITY ANALYSIS & PORTFOLIO MANAGEMENT Question BankAnonymous y3E7iaNo ratings yet

- Calculate WACC for SCS CoDocument11 pagesCalculate WACC for SCS CoHusnina FakhiraNo ratings yet

- Midland Energy Resources (Final)Document4 pagesMidland Energy Resources (Final)satherbd21100% (3)

- RISK and RETURN With SolutionsDocument33 pagesRISK and RETURN With Solutionschiaraferragni100% (2)

- Markowitz Portfolio ModelDocument9 pagesMarkowitz Portfolio ModelSamia Islam BushraNo ratings yet

- Financial Management - Risk and Rates of Return (Slides)Document137 pagesFinancial Management - Risk and Rates of Return (Slides)Nabiha KhattakNo ratings yet

- Case 30: Efficient Financing DiscussionsDocument5 pagesCase 30: Efficient Financing Discussionswaldek87No ratings yet

- Chapter 2: Traditional and Behavioral FinanceDocument22 pagesChapter 2: Traditional and Behavioral FinanceGeeta RanjanNo ratings yet

- Investing in Stocks: © 2013 Pearson Education, Inc. All Rights Reserved. 13-1Document41 pagesInvesting in Stocks: © 2013 Pearson Education, Inc. All Rights Reserved. 13-1zooz1992No ratings yet

- 7 - Risk and Rates of ReturnDocument1 page7 - Risk and Rates of ReturnAxce1996No ratings yet

- Applied Asset and Risk Management PDFDocument491 pagesApplied Asset and Risk Management PDFKomang DharmawanNo ratings yet