You might also like

- Eoy Doc 2018 PDFDocument3 pagesEoy Doc 2018 PDFmrfutschNo ratings yet

- Wbc-Ec 2020Document6 pagesWbc-Ec 2020mrfutschNo ratings yet

- China Economic Update 15 April 2019Document3 pagesChina Economic Update 15 April 2019mrfutschNo ratings yet

- NAB CEO Press Conference Transcript PDFDocument4 pagesNAB CEO Press Conference Transcript PDFmrfutschNo ratings yet

- ANZ Media CommentsDocument3 pagesANZ Media CommentsmrfutschNo ratings yet

- Ops PDFDocument43 pagesOps PDFmrfutschNo ratings yet

- Mailer 2017 Westpac Research Fellowships Opening of ApplicationsDocument1 pageMailer 2017 Westpac Research Fellowships Opening of ApplicationsmrfutschNo ratings yet

- January August: Please Note: Events and Dates Are Subject To Change. Terms and Conditions ApplyDocument1 pageJanuary August: Please Note: Events and Dates Are Subject To Change. Terms and Conditions ApplymrfutschNo ratings yet

- January August: Please Note: Events and Dates Are Subject To Change. Terms and Conditions ApplyDocument1 pageJanuary August: Please Note: Events and Dates Are Subject To Change. Terms and Conditions ApplymrfutschNo ratings yet

- Aus Chamber Westpac 2018 Q2Document14 pagesAus Chamber Westpac 2018 Q2mrfutschNo ratings yet

- NAB Residential Property Survey Q1 2018Document11 pagesNAB Residential Property Survey Q1 2018mrfutschNo ratings yet

- RandDocument9 pagesRandalfredNo ratings yet

- Bank Pac WeeklyDocument14 pagesBank Pac WeeklymrfutschNo ratings yet

- ANU Key Dates WestpacDocument1 pageANU Key Dates WestpacmrfutschNo ratings yet

- Budget PaperDocument308 pagesBudget PapermrfutschNo ratings yet

- Us Ecominic UpdateDocument5 pagesUs Ecominic UpdatemrfutschNo ratings yet

- West Pac WeeklyDocument12 pagesWest Pac WeeklymrfutschNo ratings yet

- Westpac Group Financial CalendarDocument4 pagesWestpac Group Financial CalendarmrfutschNo ratings yet

- Westpac Future Leaders Scholarship Presentation 2016Document7 pagesWestpac Future Leaders Scholarship Presentation 2016mrfutschNo ratings yet

- ANZ Subordinated Offer DocumentDocument99 pagesANZ Subordinated Offer DocumentmrfutschNo ratings yet

- Teaching and Learning 21st Century SkillsDocument37 pagesTeaching and Learning 21st Century SkillsMac SensNo ratings yet

- Quotes HieroclesDocument1 pageQuotes HieroclesmrfutschNo ratings yet

- Westpac WeeklyDocument12 pagesWestpac WeeklymrfutschNo ratings yet

- Australian Markets Weekly: Underemployment Dragging On Wages GrowthDocument6 pagesAustralian Markets Weekly: Underemployment Dragging On Wages GrowthmrfutschNo ratings yet

- Dagon Rising - The Litany of Dagon by Phil HineDocument28 pagesDagon Rising - The Litany of Dagon by Phil HineDru De Nicola De Nicola100% (1)

- Cults of Cthulhu - H.P. Lovecraft and The Occult TraditionDocument26 pagesCults of Cthulhu - H.P. Lovecraft and The Occult TraditionTsigalko77100% (2)

- Parent Orientation Powerpoint-2013-2014 PreschoolDocument46 pagesParent Orientation Powerpoint-2013-2014 PreschoolmrfutschNo ratings yet

- Economic OutlookDocument70 pagesEconomic OutlookmrfutschNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ValuationDocument3 pagesValuationBryan IbarrientosNo ratings yet

- ANZ Personal Banking Account Fees and ChargesDocument20 pagesANZ Personal Banking Account Fees and ChargesmmirpuriNo ratings yet

- Project Economics & Financial MangmentDocument38 pagesProject Economics & Financial MangmentshardultagalpallewarNo ratings yet

- Training Lecture Sheet Mostafa KamalDocument19 pagesTraining Lecture Sheet Mostafa KamalArif Uz ZamanNo ratings yet

- Beat The Bank TutorialDocument3 pagesBeat The Bank TutorialgirliepoplollipopNo ratings yet

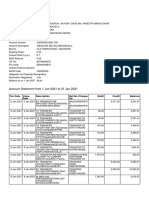

- Sbi Account Jan 2021Document2 pagesSbi Account Jan 2021Manoj GaurNo ratings yet

- Audit of Receivables: Cebu Cpar Center, IncDocument10 pagesAudit of Receivables: Cebu Cpar Center, IncEvita Ayne TapitNo ratings yet

- Za Test 8 KumarDocument30 pagesZa Test 8 KumarMia Omerika100% (1)

- Chase B Statement-MarDocument4 pagesChase B Statement-MarЮлия ПNo ratings yet

- Philippine Stocks Index Fund CorpDocument1 pagePhilippine Stocks Index Fund CorptimothymaderazoNo ratings yet

- SBI Life - Smart Platina Plus - Cr1 Handbill - SIBDocument1 pageSBI Life - Smart Platina Plus - Cr1 Handbill - SIBKiran JohnNo ratings yet

- Swot AnalysisDocument6 pagesSwot Analysissouvikrock12No ratings yet

- High Yield Bonds Market Structure, Valuation, and Portfolio StrategiesDocument689 pagesHigh Yield Bonds Market Structure, Valuation, and Portfolio StrategiesFurqaan Syah100% (1)

- X Ay TFF XMST 3 N Avx YDocument8 pagesX Ay TFF XMST 3 N Avx YRV SATYANARAYANANo ratings yet

- Total Return Swaps On Corp CDOsDocument11 pagesTotal Return Swaps On Corp CDOszdfgbsfdzcgbvdfcNo ratings yet

- Project Finance MethodologyDocument35 pagesProject Finance MethodologySky walkingNo ratings yet

- Buildium Outstanding BalancesDocument34 pagesBuildium Outstanding BalancesJulian KurtNo ratings yet

- Chapter 8 Stock ValuationDocument14 pagesChapter 8 Stock ValuationLuu Quang TungNo ratings yet

- Abc-Consolidation With Intercompany TransactionsDocument3 pagesAbc-Consolidation With Intercompany TransactionsLeonardo MercaderNo ratings yet

- Chapter 1 An Introduction To Accounting: Fundamental Financial Accounting Concepts, 10e (Edmonds)Document53 pagesChapter 1 An Introduction To Accounting: Fundamental Financial Accounting Concepts, 10e (Edmonds)brockNo ratings yet

- Applied EconomicsDocument9 pagesApplied EconomicsJanisha RadazaNo ratings yet

- Initial Project Screening Method - Payback Period: Lecture No.15 Contemporary Engineering EconomicsDocument32 pagesInitial Project Screening Method - Payback Period: Lecture No.15 Contemporary Engineering EconomicsAfiq de WinnerNo ratings yet

- Futures 0Document10 pagesFutures 0Tithi jainNo ratings yet

- Dubai Islamic Bank Results Update 16 AugustDocument4 pagesDubai Islamic Bank Results Update 16 AugustEmran Lhr PakistanNo ratings yet

- 4 AmlaDocument133 pages4 AmlaDanielle Nicole ValerosNo ratings yet

- Market Analysis November 2020Document21 pagesMarket Analysis November 2020Lau Wai KentNo ratings yet

- Does Stock Split Influence To Liquidity and Stock ReturnDocument9 pagesDoes Stock Split Influence To Liquidity and Stock ReturnBhavdeepsinh JadejaNo ratings yet

- Report Myanmar Financial Sector - A Challenging Environment For Banks Nov2013Document56 pagesReport Myanmar Financial Sector - A Challenging Environment For Banks Nov2013THAN HANNo ratings yet

- Acc Topic 7Document7 pagesAcc Topic 7BM10622P Nur Alyaa Nadhirah Bt Mohd RosliNo ratings yet

- Business Finance Week 7 Basic Long-Term Financial ConceptsDocument16 pagesBusiness Finance Week 7 Basic Long-Term Financial ConceptsJessa Gallardo0% (1)