You might also like

- MortgageDocument8 pagesMortgagePriyanjali BanerjeeNo ratings yet

- Difference Between Mortgage and ChargeDocument18 pagesDifference Between Mortgage and Chargeriddhi tulshian100% (2)

- Simple MortgageDocument10 pagesSimple MortgagesubramonianNo ratings yet

- Rights and Liabilities of MortgagerDocument6 pagesRights and Liabilities of MortgagerSaad KhanNo ratings yet

- Transfer of Property Act - 1882 - Reading MaterialDocument13 pagesTransfer of Property Act - 1882 - Reading MaterialPankaj Thakur0% (1)

- Hadley v. Baxendale - Case Brief Summary: FactsDocument2 pagesHadley v. Baxendale - Case Brief Summary: FactsJason Marquez100% (1)

- Banker and Customer RelationshipDocument24 pagesBanker and Customer RelationshipNana OpokuNo ratings yet

- SALE DEEDS PROJECT REQUIREMENTSDocument9 pagesSALE DEEDS PROJECT REQUIREMENTSsparsh9634No ratings yet

- Duties of Banker Towards His CoustomerDocument24 pagesDuties of Banker Towards His CoustomerAakashsharma0% (2)

- Indian Contract Act 1872 SummaryDocument65 pagesIndian Contract Act 1872 SummaryArjan ParmarNo ratings yet

- GRAND EDDY KNOWLES V OHAN TRANSPORT LIMITEDDocument5 pagesGRAND EDDY KNOWLES V OHAN TRANSPORT LIMITEDSimushi SimushiNo ratings yet

- Contract of IndemnityDocument11 pagesContract of IndemnityAishwarya KrishnaKumarNo ratings yet

- LLB 404 - Banking Law and Practice ModuleDocument38 pagesLLB 404 - Banking Law and Practice Modulepeter kachama100% (1)

- Advantages and Disadvantages of LawDocument2 pagesAdvantages and Disadvantages of LawMuhammad ShehzadNo ratings yet

- Doctrine of Clog and FettersDocument10 pagesDoctrine of Clog and FettersGautam Jayasurya100% (1)

- Bank Guarantees in IndiaDocument30 pagesBank Guarantees in IndiaGajendra Bhansali0% (1)

- Mortgages and ChargesDocument4 pagesMortgages and ChargesJadhako Dichwo100% (1)

- Contract Act AssignmentDocument25 pagesContract Act AssignmentMuhammad Haris SalamNo ratings yet

- Assignment 2ndDocument14 pagesAssignment 2ndSwarup Das DiptoNo ratings yet

- Fixtures and ChattelsDocument9 pagesFixtures and ChattelsJoshua AtkinsNo ratings yet

- R V Panel On Takeovers and MergersDocument2 pagesR V Panel On Takeovers and Mergersanon_826995160No ratings yet

- DK Basu Versus State of WestBengalDocument12 pagesDK Basu Versus State of WestBengalbansNo ratings yet

- Workers' compensation case overturned due to fraudDocument3 pagesWorkers' compensation case overturned due to fraudPriyankaNo ratings yet

- Dr. M.S. Raj-Purohit's Notes on Indian Limitation ActDocument10 pagesDr. M.S. Raj-Purohit's Notes on Indian Limitation ActRadhika Reddy50% (2)

- Breach of Contract AssignmentDocument7 pagesBreach of Contract AssignmentSamiul RatulNo ratings yet

- Creation of AgencyDocument3 pagesCreation of AgencyMeenal Pachory Pandey100% (1)

- Unit 4 Duty of Disclosure Materiality of Facts and MisrepresentationDocument19 pagesUnit 4 Duty of Disclosure Materiality of Facts and MisrepresentationIsrael KalabaNo ratings yet

- Land Law Martin DixonDocument43 pagesLand Law Martin DixonEdwin Oloo100% (1)

- Property law - transfer by ostensible ownerDocument12 pagesProperty law - transfer by ostensible ownerMRINMAY KUSHAL100% (1)

- Assignment and Nomination Under Insurance PoliciesDocument5 pagesAssignment and Nomination Under Insurance PoliciesNasma AbidiNo ratings yet

- Act 1955 - ClassDocument40 pagesAct 1955 - ClassLokesh KumarNo ratings yet

- Holland v Hodgson key tests for determining fixtures and fittingsDocument5 pagesHolland v Hodgson key tests for determining fixtures and fittingsSuvigya TripathiNo ratings yet

- Whether Automatic Vending Machines Make OffersDocument10 pagesWhether Automatic Vending Machines Make OffersHarshit JainNo ratings yet

- Brief Note Fulham CaseDocument2 pagesBrief Note Fulham CaseAyush JohriNo ratings yet

- CLAYTON'S CASE & RulesDocument3 pagesCLAYTON'S CASE & Rulesvivekananda RoyNo ratings yet

- Q.5 Redeem Up Forclose DownDocument3 pagesQ.5 Redeem Up Forclose DownGauravNo ratings yet

- Discharge of ContractDocument17 pagesDischarge of ContractatreNo ratings yet

- Understanding of Compulsorily Convertible Debentures Vinod KothariDocument7 pagesUnderstanding of Compulsorily Convertible Debentures Vinod KothariNazir kondkariNo ratings yet

- Steps to voluntarily wind up a companyDocument2 pagesSteps to voluntarily wind up a companyPurvi ShahNo ratings yet

- Discharge of ContractDocument3 pagesDischarge of Contractmalik yasirNo ratings yet

- 08 - Chapter 4Document33 pages08 - Chapter 4Vinay Kumar KumarNo ratings yet

- Terms and Conditions of The Loan AgreementsDocument2 pagesTerms and Conditions of The Loan AgreementsCLATOUS CHAMANo ratings yet

- 1.1 Nature of ContractDocument55 pages1.1 Nature of ContractvanshikaNo ratings yet

- Law - Indian Contract Act, 1872 (4 of 6) - 1Document16 pagesLaw - Indian Contract Act, 1872 (4 of 6) - 1Ñävdèèp Käûr RämgärhîäNo ratings yet

- Group 6 Banking Law AssignmentDocument22 pagesGroup 6 Banking Law Assignmentmoses machiraNo ratings yet

- PPP II Application of ELDocument23 pagesPPP II Application of ELShangavi SNo ratings yet

- Rylands V FletcherDocument4 pagesRylands V Fletcherkrishy19No ratings yet

- BR Ch-2 Contract LawDocument12 pagesBR Ch-2 Contract LawROHITHNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Academic SessionDocument10 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Academic SessionSanstubh SonkarNo ratings yet

- Question Papers of Banking and Negotiable Instrument ActDocument93 pagesQuestion Papers of Banking and Negotiable Instrument ActM NageshNo ratings yet

- Unit 2. Law of ContractDocument29 pagesUnit 2. Law of Contractste100% (2)

- Liabilities of Mortgagor and MortgageeDocument4 pagesLiabilities of Mortgagor and MortgageeMahmudul HasanNo ratings yet

- The Rights of The Banker IncludeDocument5 pagesThe Rights of The Banker Includem_dattaias67% (3)

- Agreements Expressly Declared As Void Contingent Contract and Quasi-ContractDocument11 pagesAgreements Expressly Declared As Void Contingent Contract and Quasi-ContractKazia Shamoon Ahmed100% (1)

- Law of Contract NotesDocument112 pagesLaw of Contract NotesChris Sanders80% (5)

- Specific ReliefDocument13 pagesSpecific ReliefDaniel Cook50% (2)

- Annual Labour Administration and Inspection ReportDocument48 pagesAnnual Labour Administration and Inspection ReportJeremia Mtobesya100% (2)

- ATTORNEY GENERAL V ZAMBIA SUGARDocument10 pagesATTORNEY GENERAL V ZAMBIA SUGARSimushi SimushiNo ratings yet

- Project Banking Law Shruti KambleDocument19 pagesProject Banking Law Shruti KambleShruti KambleNo ratings yet

- Criminalising Abortion Dilemma Morality Health ChoicesDocument5 pagesCriminalising Abortion Dilemma Morality Health ChoicesShruti KambleNo ratings yet

- Industrial Adjudication in India and in USADocument22 pagesIndustrial Adjudication in India and in USAShruti KambleNo ratings yet

- Insurance LawDocument15 pagesInsurance LawShruti KambleNo ratings yet

- Democracy and InequalityDocument15 pagesDemocracy and InequalityShruti KambleNo ratings yet

- Project Banking Law Shruti KambleDocument20 pagesProject Banking Law Shruti KambleShruti KambleNo ratings yet

- Mutual FundsDocument6 pagesMutual FundsPratikNo ratings yet

- Rights of Sharholder and StakeholderDocument17 pagesRights of Sharholder and StakeholderShruti KambleNo ratings yet

- InsuranceLIFE INSURANCE: CONCEPT, NATURE AND IMPORTANT PROVISON UNDER THE ACTDocument26 pagesInsuranceLIFE INSURANCE: CONCEPT, NATURE AND IMPORTANT PROVISON UNDER THE ACTShruti Kamble100% (1)

- UN and Global Counter Terrorism StrategyDocument6 pagesUN and Global Counter Terrorism StrategyShruti KambleNo ratings yet

- Piracy On The InternetDocument25 pagesPiracy On The InternetShruti KambleNo ratings yet

- Piracy On The InternetDocument25 pagesPiracy On The InternetShruti KambleNo ratings yet

- STUDY ON PRESUMPTION AS TO THE DOCUMENTS OF 30 YEAR OLD DOCUMENTSceDocument16 pagesSTUDY ON PRESUMPTION AS TO THE DOCUMENTS OF 30 YEAR OLD DOCUMENTSceShruti Kamble0% (1)

- Application of Doctrine of Public Policy in Conflict of LawsDocument17 pagesApplication of Doctrine of Public Policy in Conflict of LawsShruti Kamble100% (1)

- Liquidation of CompaniesDocument34 pagesLiquidation of CompaniesShakthi p raiNo ratings yet

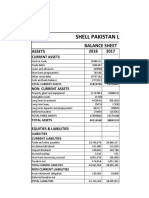

- Shell Pakistan LTD: Assets 2018 2017Document11 pagesShell Pakistan LTD: Assets 2018 2017mohammad bilalNo ratings yet

- Bloomberg Fixed IncomeDocument2 pagesBloomberg Fixed Incomeprachiz1No ratings yet

- ACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilityDocument5 pagesACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilitySayadi AdiihNo ratings yet

- Cash Budgeting Examples.Document21 pagesCash Budgeting Examples.Muhammad azeem83% (6)

- TractorexcesscreditDocument2 pagesTractorexcesscreditash209606No ratings yet

- Fiqh Muamalah: Islamic Business TransactionDocument15 pagesFiqh Muamalah: Islamic Business TransactionMahyuddin KhalidNo ratings yet

- 5/5 Adjustable Rate Mortgage Loan: 5/5 Arm Home Loan Rates and TermsDocument5 pages5/5 Adjustable Rate Mortgage Loan: 5/5 Arm Home Loan Rates and TermsAmin KNo ratings yet

- Instructions For Completing Uniform Residential Loan Application-Instructions Freddie Mac Form 65 - Fannie Mae Form 1003Document15 pagesInstructions For Completing Uniform Residential Loan Application-Instructions Freddie Mac Form 65 - Fannie Mae Form 1003larry-612445No ratings yet

- Asian Cathay Finance and Leasing Corp PDFDocument2 pagesAsian Cathay Finance and Leasing Corp PDFNelia Mae S. VillenaNo ratings yet

- LoanDocument9 pagesLoanM YusronNo ratings yet

- Full Download Prealgebra 4th Edition Tom Carson Solutions ManualDocument36 pagesFull Download Prealgebra 4th Edition Tom Carson Solutions Manualjaydenvbe100% (39)

- Understanding Cash and Cash EquivalentsDocument6 pagesUnderstanding Cash and Cash EquivalentsNicole Anne Santiago SibuloNo ratings yet

- Small Business Reorganization ActDocument10 pagesSmall Business Reorganization ActSam GikonyoNo ratings yet

- Aave v2 WhitepaperDocument14 pagesAave v2 Whitepaperalexander benNo ratings yet

- True-False Statements: The Recording ProcessDocument17 pagesTrue-False Statements: The Recording ProcessMary Grace Abales LaboNo ratings yet

- Trans-Pacific Industrial v. CADocument1 pageTrans-Pacific Industrial v. CAKimNo ratings yet

- Notes Receivable ReviewerDocument3 pagesNotes Receivable ReviewerWinnie ToribioNo ratings yet

- Team Code 3Document143 pagesTeam Code 3alam amarNo ratings yet

- Sbi Home Loan InfoDocument4 pagesSbi Home Loan InfoBhargavaSharmaNo ratings yet

- Loan Status Report (LSR)Document1 pageLoan Status Report (LSR)api-18738338No ratings yet

- The Law On Credit TransactionsDocument57 pagesThe Law On Credit TransactionsJutajero, Camille Ann M.No ratings yet

- Stephen Snyder - Good CreditDocument26 pagesStephen Snyder - Good CreditRobert GutierrezNo ratings yet

- Auto Title Loans and The Law BrochureDocument2 pagesAuto Title Loans and The Law BrochureSC AppleseedNo ratings yet

- Module 6: The Mathematics of FinanceDocument16 pagesModule 6: The Mathematics of FinanceMabel LynNo ratings yet

- INTERROGATIVES Depositions For DisclosureDocument6 pagesINTERROGATIVES Depositions For Disclosureolboy92No ratings yet

- MBS Data: Agency Mortgage-Backed Securities (MBS) Purchase ProgramDocument572 pagesMBS Data: Agency Mortgage-Backed Securities (MBS) Purchase ProgramTheBusinessInsiderNo ratings yet

- Lecture-11 Compound Interest)Document2 pagesLecture-11 Compound Interest)Aditya SahaNo ratings yet

- Lehman Brothers and LIBOR ScandalDocument16 pagesLehman Brothers and LIBOR Scandalkartikaybansal8825No ratings yet

- Math0301 Review Exercise Set 15Document5 pagesMath0301 Review Exercise Set 15Ever DaleNo ratings yet