You might also like

- ICAEW - Valuing A BusinessDocument4 pagesICAEW - Valuing A BusinessMyrefNo ratings yet

- Code of Ethics Part C Professional Accountants in Business 1 Jan 2011Document11 pagesCode of Ethics Part C Professional Accountants in Business 1 Jan 2011James De Torres CarilloNo ratings yet

- September 14 Gary Kadi MI SeminarDocument2 pagesSeptember 14 Gary Kadi MI SeminarHenryScheinDentalNo ratings yet

- Final Exam Case NotesDocument17 pagesFinal Exam Case NotesMike Ambrosino100% (1)

- AT&T Vrs Microsoft Litigation Case StudyDocument3 pagesAT&T Vrs Microsoft Litigation Case StudyFrancis TetteyNo ratings yet

- Special Report PDM Guidebook2016Document44 pagesSpecial Report PDM Guidebook2016Vinoth KumarNo ratings yet

- MBA104 - Almario - Parco - Case Study LGAOP01Document15 pagesMBA104 - Almario - Parco - Case Study LGAOP01Jesse Rielle CarasNo ratings yet

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Document25 pagesMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Jesse Rielle CarasNo ratings yet

- Ecopak Case Notes Chapter 4 5Document3 pagesEcopak Case Notes Chapter 4 5Gajan SelvaNo ratings yet

- CTDP & CTP Certification - Handbook PDFDocument21 pagesCTDP & CTP Certification - Handbook PDFNimish Kumar BhatiaNo ratings yet

- Financial management practices of small firms in GhanaDocument5 pagesFinancial management practices of small firms in GhanaTakuriNo ratings yet

- Financial Accounting: Unit-1Document22 pagesFinancial Accounting: Unit-1Garima Kwatra100% (1)

- Corporate Finance - Raising Equity - UnimelbDocument63 pagesCorporate Finance - Raising Equity - UnimelbGenPershingNo ratings yet

- Tax Issues in Purchase and Sale AgreementsDocument20 pagesTax Issues in Purchase and Sale AgreementsTaichi ChenNo ratings yet

- 2511 Practice Final Exam AnswersDocument7 pages2511 Practice Final Exam AnswersMarco A HenriquezNo ratings yet

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Document23 pagesMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Jesse Rielle CarasNo ratings yet

- TAX ADMINISTRATION GUIDEDocument4 pagesTAX ADMINISTRATION GUIDEwumel01No ratings yet

- Due Diligence ChecklistDocument4 pagesDue Diligence ChecklistHans Gretel100% (1)

- Company Law For Business BLAW2006: Tutorial QuestionsDocument6 pagesCompany Law For Business BLAW2006: Tutorial QuestionsYashrajsing LuckkanaNo ratings yet

- Audit and Assurance Aa Revison Notes 2019Document85 pagesAudit and Assurance Aa Revison Notes 2019Jeshna JoomuckNo ratings yet

- Regulation MyNotesDocument50 pagesRegulation MyNotesaudalogy100% (1)

- Purchase Price AllocationDocument8 pagesPurchase Price AllocationTharnn KshatriyaNo ratings yet

- Argenti A ScoreDocument1 pageArgenti A Scoremd1586100% (1)

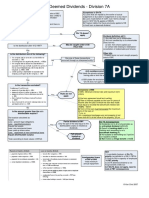

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713No ratings yet

- Aljared ProfileDocument30 pagesAljared ProfileAmeen AlwaeyNo ratings yet

- As 26 Intangible AssetsDocument45 pagesAs 26 Intangible Assetsjoseph davidNo ratings yet

- Chevron Case AnalysisDocument29 pagesChevron Case AnalysisKhawaja UsmanNo ratings yet

- Hisrich Entrepreneurship 11e Chap010Document11 pagesHisrich Entrepreneurship 11e Chap010swapnilNo ratings yet

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713No ratings yet

- CPA Regulation (Reg) Notes 2013Document7 pagesCPA Regulation (Reg) Notes 2013amichalek0820100% (3)

- IAS 16 Property, Plant & EquipmentDocument63 pagesIAS 16 Property, Plant & Equipmentali muzamilNo ratings yet

- Chapter 1 Audit f8 - 2.3Document25 pagesChapter 1 Audit f8 - 2.3JosephineMicheal17No ratings yet

- When To Hire A Tax ProfessionalDocument7 pagesWhen To Hire A Tax ProfessionalMaimai Durano100% (1)

- Chapter+11 Transactional+CycleDocument35 pagesChapter+11 Transactional+Cyclemohazka hassan100% (1)

- Agreed Upon Procedures vs. Consulting EngagementsDocument49 pagesAgreed Upon Procedures vs. Consulting EngagementsCharles B. Hall100% (1)

- Client Project Sign-Off Form: Project Name: Project ManagerDocument1 pageClient Project Sign-Off Form: Project Name: Project ManagerBiswajitNo ratings yet

- 15 Financial AccountsDocument111 pages15 Financial AccountsRenga Pandi100% (1)

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Document12 pagesCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiNo ratings yet

- Working Capital Plan for A.G. Private Limited Tea IndustryDocument4 pagesWorking Capital Plan for A.G. Private Limited Tea IndustryIvraj HarlalkaNo ratings yet

- EbitdaDocument6 pagesEbitdaAlper AykaçNo ratings yet

- Accounting Clerk - DacumDocument4 pagesAccounting Clerk - DacumAtif MahmoodNo ratings yet

- Sample Home Electrical Inspection Checklist: OutletsDocument2 pagesSample Home Electrical Inspection Checklist: OutletsjoookingNo ratings yet

- Financial Accounting 1Document530 pagesFinancial Accounting 1aponojecyNo ratings yet

- Digital Health Assesment in Hydro PowerDocument36 pagesDigital Health Assesment in Hydro PowerSuhas100% (1)

- 1 Procurement Best Practice Guideline Procurement Planning enDocument13 pages1 Procurement Best Practice Guideline Procurement Planning enYani IriawadiNo ratings yet

- ch05 SM Leo 10eDocument31 pagesch05 SM Leo 10ePyae Phyo100% (2)

- Construction AuditDocument26 pagesConstruction AuditSithick MohamedNo ratings yet

- Facilities: ManagementDocument27 pagesFacilities: Managementriyan riyadiNo ratings yet

- Financial Statements and Performance Analysis: DR Leslie Mitchell Financial ControlDocument31 pagesFinancial Statements and Performance Analysis: DR Leslie Mitchell Financial Controlosaleemi100% (1)

- Commercial Building Energy Audit DataDocument8 pagesCommercial Building Energy Audit DataAARON HUNDLEYNo ratings yet

- FPG DueDiligenceDocument22 pagesFPG DueDiligenceEmeric RenaudNo ratings yet

- Buiolding MantenanceDocument13 pagesBuiolding MantenanceSean ChanNo ratings yet

- Recent Studies/Tax Credit Benefits ObtainedDocument7 pagesRecent Studies/Tax Credit Benefits ObtainedResearch and Development Tax Credit Magazine; David Greenberg PhD, MSA, EA, CPA; TGI; 646-705-2910No ratings yet

- Oil and Gas Accounting and Firm'S Financial PerformanceDocument8 pagesOil and Gas Accounting and Firm'S Financial Performanceابوالحروف العربي ابوالحروفNo ratings yet

- Business and The Social EnvironmentDocument20 pagesBusiness and The Social EnvironmentPiran UmrigarNo ratings yet

- Managing Financial Risk: OutcomesDocument35 pagesManaging Financial Risk: OutcomesprabodhNo ratings yet

- Risk Management in Entrepre Nuria L VenturesDocument9 pagesRisk Management in Entrepre Nuria L VenturesAustin JosephNo ratings yet

- (Russell D.) Insuring The Bottom Line How To Prot (BookFi) PDFDocument609 pages(Russell D.) Insuring The Bottom Line How To Prot (BookFi) PDFNeha SainiNo ratings yet

- Risk in Business El Yaagoubi Zineb Boussoughi Nahid Hiba El Khoudri Ayoub Zdaik LamiaeDocument11 pagesRisk in Business El Yaagoubi Zineb Boussoughi Nahid Hiba El Khoudri Ayoub Zdaik LamiaeAchraf El aouameNo ratings yet

- Au BP Good - Security - Good - Business Eng 2008Document32 pagesAu BP Good - Security - Good - Business Eng 2008BMNo ratings yet

- Welding Aluminium 1090-3Document2 pagesWelding Aluminium 1090-3roldoguidoNo ratings yet

- Common Line CuttingDocument1 pageCommon Line CuttingroldoguidoNo ratings yet

- Guidance Note Plate Bending No. 5.04: ScopeDocument3 pagesGuidance Note Plate Bending No. 5.04: ScoperoldoguidoNo ratings yet

- Eurocentrism - Samir Amin PDFDocument290 pagesEurocentrism - Samir Amin PDFEduardo Souza Cunha100% (1)

- EN-10149-2 Thermo Mec SteelDocument18 pagesEN-10149-2 Thermo Mec SteelroldoguidoNo ratings yet

- Efective Mamnage (Risk) SpringerDocument241 pagesEfective Mamnage (Risk) Springerroldoguido100% (4)

- Wereld Ongelijkheid Rapport 2018Document300 pagesWereld Ongelijkheid Rapport 2018Chris de Vries100% (1)

- ISO TR 25901 1 2016 en VocabularyDocument11 pagesISO TR 25901 1 2016 en VocabularyroldoguidoNo ratings yet

- Politics of Heroin in South East AsiaDocument508 pagesPolitics of Heroin in South East Asiaites76No ratings yet

- Stress Strain & Hardening Uni CalifDocument7 pagesStress Strain & Hardening Uni CalifroldoguidoNo ratings yet

- Cold Formig Techniques PDFDocument4 pagesCold Formig Techniques PDFroldoguidoNo ratings yet

- JRC Steel Embrittlem Cold Hollow PDFDocument204 pagesJRC Steel Embrittlem Cold Hollow PDFroldoguidoNo ratings yet

- NB CPD Sg18!07!052 GlulamDocument22 pagesNB CPD Sg18!07!052 GlulamroldoguidoNo ratings yet

- Pull DownDocument8 pagesPull DownroldoguidoNo ratings yet

- Is Iso 6789 2003 PDFDocument22 pagesIs Iso 6789 2003 PDFsuresh kumar100% (1)

- High Strength Structural Bolting Assemblies For Preloading, According To EN 14399. Technical Information For UseDocument8 pagesHigh Strength Structural Bolting Assemblies For Preloading, According To EN 14399. Technical Information For UseAlexander MarinovNo ratings yet

- G - Carinici - DuplexFab PDFDocument56 pagesG - Carinici - DuplexFab PDFlewgne08No ratings yet

- Aws D10.9Document73 pagesAws D10.9scrib93420No ratings yet

- 10STWJ - Arora Cooling Rate From Dim AnalysesDocument5 pages10STWJ - Arora Cooling Rate From Dim AnalysesroldoguidoNo ratings yet

- Aws QC1 (1996)Document18 pagesAws QC1 (1996)ippon_osotoNo ratings yet

- Undermatching Weld Metal Where AdvantageousDocument3 pagesUndermatching Weld Metal Where AdvantageousEng-JR100% (1)

- Din en Iso 9013Document8 pagesDin en Iso 9013roldoguidoNo ratings yet

- Welding PreheatDocument2 pagesWelding PreheatsjmudaNo ratings yet

- 10STWJ - Arora Cooling Rate From Dim AnalysesDocument5 pages10STWJ - Arora Cooling Rate From Dim AnalysesroldoguidoNo ratings yet

- Wps Follow Chart PDFDocument2 pagesWps Follow Chart PDFmail_younes6592100% (1)

- Heat Treat Bridge Rehabilitat Uni PurdueDocument77 pagesHeat Treat Bridge Rehabilitat Uni PurdueroldoguidoNo ratings yet

- Post Cold Form Limits & HT RequiremtsDocument1 pagePost Cold Form Limits & HT RequiremtsroldoguidoNo ratings yet

- Cold Form Toughness CIDECT-1B-2 - 03Document30 pagesCold Form Toughness CIDECT-1B-2 - 03roldoguidoNo ratings yet

- The Future of GoldDocument199 pagesThe Future of GoldJohn OxNo ratings yet

- Aromaterapie Si Uleiuri EsentialeDocument1 pageAromaterapie Si Uleiuri EsentialeBogdan Şi Alexandra AmbăruşNo ratings yet

- PGDFM Finacial Mangment Final PDFDocument260 pagesPGDFM Finacial Mangment Final PDFAnonymous H4xWhTmNo ratings yet

- 3.fluctuation of YuanDocument2 pages3.fluctuation of YuanĐặng Quỳnh TrangNo ratings yet

- Bispap 143Document190 pagesBispap 143qhycvhx8jmNo ratings yet

- Standing Order of Reference From The United States District Court For The District of DelawareDocument44 pagesStanding Order of Reference From The United States District Court For The District of DelawareLuis Fernando Pino RangelNo ratings yet

- Module 1 Special Topics in Financial ManagementDocument22 pagesModule 1 Special Topics in Financial Managementkimjoshuadiaz12No ratings yet

- Exposure NormsDocument30 pagesExposure Normspadam_09No ratings yet

- The Monetary System in The International ArenaDocument2 pagesThe Monetary System in The International Arenagian reyesNo ratings yet

- Assignment On IbDocument11 pagesAssignment On IbRajashree MuktiarNo ratings yet

- Bank Indonesia Regulation No 16-17-PBI-2014 (English Version)Document33 pagesBank Indonesia Regulation No 16-17-PBI-2014 (English Version)YuLy EkawatiNo ratings yet

- RobovidapekDocument2 pagesRobovidapekBELLO SAIFULLAHINo ratings yet

- TDA Account HandbookDocument14 pagesTDA Account HandbookgrupometroNo ratings yet

- FOREX Day Trading..Document3 pagesFOREX Day Trading..Ahmed NabilNo ratings yet

- Forex Basics & Secrets in 15 MinutesDocument19 pagesForex Basics & Secrets in 15 MinutesMakeForexEasy100% (11)

- The Coming Reset of The International Monetary SystemDocument1 pageThe Coming Reset of The International Monetary SystemEliezer Ben Iejeskel100% (1)

- Smart Money Trading GuideDocument9 pagesSmart Money Trading GuidesgksanalNo ratings yet

- Competitive Prices for Bathroom FittingsDocument2 pagesCompetitive Prices for Bathroom FittingsvictorNo ratings yet

- Balance of Payment 20Document79 pagesBalance of Payment 20Anshul SinhaNo ratings yet

- Chapter 6 - Hedging Foreign Exchange RiskDocument66 pagesChapter 6 - Hedging Foreign Exchange RiskHay JirenyaaNo ratings yet

- Re: Exposure Draft Comment: Hedge Accounting (ED/2010/13) : Blend and Extend Interest Rate Swap Transactions (IRS)Document3 pagesRe: Exposure Draft Comment: Hedge Accounting (ED/2010/13) : Blend and Extend Interest Rate Swap Transactions (IRS)mutuluNo ratings yet

- Vol-4 Introduction To Technical AnalysisDocument77 pagesVol-4 Introduction To Technical Analysissskendre100% (1)

- 7 Currencies Worth More Than The U.S. Dollar in 2022Document11 pages7 Currencies Worth More Than The U.S. Dollar in 2022dhaiwat100% (1)

- Annual Report Analysis For FMCG CompaniesDocument5 pagesAnnual Report Analysis For FMCG CompaniesJyoti GuptaNo ratings yet

- FX Rates Spot Forward Borrowing LendingDocument17 pagesFX Rates Spot Forward Borrowing Lending919Pranav ShedgeNo ratings yet

- Details RequireDocument2 pagesDetails RequireVadim KuzinNo ratings yet

- Econ 472 AB EicherDocument8 pagesEcon 472 AB EicherframestiNo ratings yet

- Evolution of International Monetary SystemsDocument8 pagesEvolution of International Monetary Systemsmohan7708No ratings yet

- PER KILO - CLEANED - 2023 (2) - CompressedDocument7 pagesPER KILO - CLEANED - 2023 (2) - CompressedVishnu PrasannaNo ratings yet

- International Financial Management Lecture 8 & 9 PDFDocument87 pagesInternational Financial Management Lecture 8 & 9 PDFAshish KhetadeNo ratings yet