You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- International Governmental Organisations and Global Youth UnemploymentDocument1 pageInternational Governmental Organisations and Global Youth Unemploymentshekhar3843No ratings yet

- International Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy DiscoursesDocument5 pagesInternational Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy Discoursesshekhar3843No ratings yet

- Clip 4Document3 pagesClip 4shekhar3843No ratings yet

- International Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy DiscoursesDocument5 pagesInternational Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy Discoursesshekhar3843No ratings yet

- Gift DeedDocument5 pagesGift Deedshekhar3843No ratings yet

- International Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy DiscoursesDocument5 pagesInternational Governmental Organisations and Global Youth Unemployment: The Normative and Ideational Foundations of Policy Discoursesshekhar3843No ratings yet

- Brain DrainDocument6 pagesBrain Drainshekhar3843No ratings yet

- Brain DrainDocument6 pagesBrain Drainshekhar3843No ratings yet

- With Reference To The Video Shown and The Doctrines of Administrative Law, Answer The Following Questions: (2 5 10)Document1 pageWith Reference To The Video Shown and The Doctrines of Administrative Law, Answer The Following Questions: (2 5 10)shekhar3843No ratings yet

- A Project On Stamp DutyDocument13 pagesA Project On Stamp DutySurajit RoyNo ratings yet

- Tamil Nadu National Law School: Relevance of Social Security in International LawDocument19 pagesTamil Nadu National Law School: Relevance of Social Security in International Lawshekhar3843No ratings yet

- 1111Document15 pages1111shekhar3843No ratings yet

- Lawteacher: Order NowDocument11 pagesLawteacher: Order Nowshekhar3843No ratings yet

- E Vasila Copyrightability of CharactersDocument14 pagesE Vasila Copyrightability of Charactersshekhar3843No ratings yet

- Plaintiff Case ListDocument2 pagesPlaintiff Case Listshekhar3843No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Loan LetterDocument1 pageLoan LetterMuhd HisyamuddinNo ratings yet

- Outline - AC2101 Seminar 4-5 FA Outline - Revised - StudentsDocument35 pagesOutline - AC2101 Seminar 4-5 FA Outline - Revised - StudentsC.TangibleNo ratings yet

- CHAPTER 17 INVESTMENTS ExercisesDocument14 pagesCHAPTER 17 INVESTMENTS ExercisesAila Marie MovillaNo ratings yet

- Bankruptcy RemediesDocument7 pagesBankruptcy RemediesMohd Ridzuan ZainalNo ratings yet

- Credit Risk and Bank Interest Rate Spreads in Uganda FinalDocument82 pagesCredit Risk and Bank Interest Rate Spreads in Uganda FinalbagumaNo ratings yet

- Jargon Buster Fact SheetDocument9 pagesJargon Buster Fact Sheettedi wediNo ratings yet

- Borrowing Costs and Government GrantsDocument3 pagesBorrowing Costs and Government Grantstough mamaNo ratings yet

- State of Black RI Home Ownership Report June 2022Document8 pagesState of Black RI Home Ownership Report June 2022NBC 10 WJARNo ratings yet

- TIME PRESENT AND TIME PAST: GLOBALIZATION, INTERNATIONAL FINANCIAL INSTITUTIONS, AND THE THIRD WORLD - Antony AnghieDocument27 pagesTIME PRESENT AND TIME PAST: GLOBALIZATION, INTERNATIONAL FINANCIAL INSTITUTIONS, AND THE THIRD WORLD - Antony AnghieFlorencia Zubeldía CascónNo ratings yet

- HDFC PPT (RCML&RDocument16 pagesHDFC PPT (RCML&RAtharv BhavsarNo ratings yet

- Homework 4 - AnswerDocument9 pagesHomework 4 - Answer蔡杰翰No ratings yet

- 360kompany GMBH Corporate Structure TreeDocument1 page360kompany GMBH Corporate Structure Treeprabhav2050No ratings yet

- Working Capital Management Quick NotesDocument9 pagesWorking Capital Management Quick NotesAlliah Mae ArbastoNo ratings yet

- Company Law ProblemsDocument4 pagesCompany Law ProblemsPuneetGupta100% (1)

- Particulars of Claim FinalDocument58 pagesParticulars of Claim FinalCensored News NowNo ratings yet

- Capital Growth, Financing Source and Profitability of Small Businesses: Evidence From Taiwan Small EnterprisesDocument2 pagesCapital Growth, Financing Source and Profitability of Small Businesses: Evidence From Taiwan Small EnterprisesKukurubuuuNo ratings yet

- Acctg 100C 16 PDFDocument4 pagesAcctg 100C 16 PDFQuid DamityNo ratings yet

- Topic 9 Lecture Additional NotesDocument28 pagesTopic 9 Lecture Additional NotesNguyễn Mạnh HùngNo ratings yet

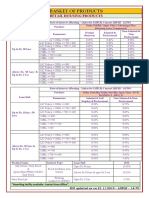

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaNo ratings yet

- 2839 MEG CV 2 CaseDocument10 pages2839 MEG CV 2 CasegueigunNo ratings yet

- OSHPD ReportsDocument137 pagesOSHPD ReportsDCHS FriendsNo ratings yet

- MAE - P4 Chapter 5Document2 pagesMAE - P4 Chapter 5Leah Mae NolascoNo ratings yet

- MMPC 14 Solved Assignment Final Zbyn0x (1) 220427 061357Document12 pagesMMPC 14 Solved Assignment Final Zbyn0x (1) 220427 061357yogesh sharmaNo ratings yet

- Ch2TQ AnswersDocument14 pagesCh2TQ AnswersLeonid Leo100% (2)

- Financial Modelling For A ProjectDocument8 pagesFinancial Modelling For A ProjectKingsley Chika NwangwuNo ratings yet

- 5 - FAAC Rules PDFDocument4 pages5 - FAAC Rules PDFDzulija TalipanNo ratings yet

- LBO BMC Course Manual - 5c34e57d43e95 PDFDocument135 pagesLBO BMC Course Manual - 5c34e57d43e95 PDFSiddharth JaswalNo ratings yet

- Berot v. SiapnoDocument2 pagesBerot v. SiapnoAnsai Claudine CaluganNo ratings yet

- PSE Overview PDFDocument43 pagesPSE Overview PDFRonStephaneMaylonNo ratings yet

- Quiz Working Cap-StudentsDocument4 pagesQuiz Working Cap-StudentsJennifer RasonabeNo ratings yet