You might also like

- Killer Commodities: How to Cash in on the Hottest New Trading TrendsFrom EverandKiller Commodities: How to Cash in on the Hottest New Trading TrendsNo ratings yet

- Project Market Structure: Meaning, Characteristics and FormsDocument22 pagesProject Market Structure: Meaning, Characteristics and FormsSipun SahooNo ratings yet

- Market Structure and Pricing PoliciesDocument32 pagesMarket Structure and Pricing PoliciesSharanya Ramesh100% (1)

- Market: Subject: Business Economics Subject Code: SBAA1103Document19 pagesMarket: Subject: Business Economics Subject Code: SBAA1103ushna ahmedNo ratings yet

- Bs. EconomicsDocument18 pagesBs. EconomicsRameshNo ratings yet

- Unit IV Notes (Updated)Document13 pagesUnit IV Notes (Updated)21EBKCS074PARULNo ratings yet

- Unit IV Notes (Updated)Document15 pagesUnit IV Notes (Updated)ayan.azimNo ratings yet

- Bs. Economics 1Document17 pagesBs. Economics 1UmeshNo ratings yet

- Market StructuresDocument45 pagesMarket StructuresbonduamrutharaoNo ratings yet

- Unit 4Document65 pagesUnit 4M ChandruNo ratings yet

- Perfect MarketDocument7 pagesPerfect MarketAlit AbrahamNo ratings yet

- Market Structure: Meaning, Characteristics and Forms - EconomicsDocument15 pagesMarket Structure: Meaning, Characteristics and Forms - EconomicsLouise Laine Dayao100% (1)

- Meaning of Market StructureDocument18 pagesMeaning of Market StructureAbhishek Yadav100% (2)

- Market StructureDocument19 pagesMarket StructureSudhanshu BhattNo ratings yet

- Market (Economics)Document12 pagesMarket (Economics)anirudh birlaNo ratings yet

- Module 4Document20 pagesModule 4Anonymous d3CGBMzNo ratings yet

- Theory of Market-1Document259 pagesTheory of Market-1Adel TaarabtyNo ratings yet

- Theory of Market-1Document259 pagesTheory of Market-1Adel Taarabty100% (1)

- Perfect CompetitionDocument10 pagesPerfect Competitionann585878No ratings yet

- Classification of Markets: Local Markets: in Such A Market The Buyers and Sellers Are Limited To The Local Region orDocument5 pagesClassification of Markets: Local Markets: in Such A Market The Buyers and Sellers Are Limited To The Local Region orNIKITHAA ASHWINNo ratings yet

- Name of The Course: Business Economics Name of The Course: Business Economics Course Code: Course CodeDocument33 pagesName of The Course: Business Economics Name of The Course: Business Economics Course Code: Course CodeVIVA MANNo ratings yet

- Unit Iii Market StructureDocument35 pagesUnit Iii Market StructureJeeva BalanNo ratings yet

- Asgnmt4 (522) Sir Yasir ArafatDocument24 pagesAsgnmt4 (522) Sir Yasir ArafatDil NawazNo ratings yet

- MarketDocument4 pagesMarketNainil TripathiNo ratings yet

- Unit IvDocument24 pagesUnit IvrajapatnaNo ratings yet

- Unit IV - (Managerial Economics) Market Structures & Pricing StrategiesDocument37 pagesUnit IV - (Managerial Economics) Market Structures & Pricing StrategiesAbhinav SachdevaNo ratings yet

- Financial Market and Market StructuresDocument23 pagesFinancial Market and Market StructuresRamil Jr GaciasNo ratings yet

- MEFA Edhoti Le KaaniDocument63 pagesMEFA Edhoti Le KaaniChethan MuthukuruNo ratings yet

- A2 Markets & Market SystemsDocument17 pagesA2 Markets & Market SystemsAnnacky AngalaNo ratings yet

- 10 Chapter 2Document39 pages10 Chapter 2Reymark BigcasNo ratings yet

- Chapter No. 9: Forms of Market: Lilavatibai Podar High School. ISCDocument12 pagesChapter No. 9: Forms of Market: Lilavatibai Podar High School. ISCStephine BochuNo ratings yet

- MEFA U3 MaterialDocument10 pagesMEFA U3 MaterialBhaskhar ReddyNo ratings yet

- Market and Revenue Curves of Firms - Ch12Document17 pagesMarket and Revenue Curves of Firms - Ch12LeenaNo ratings yet

- Managerial EconomicsssssDocument2 pagesManagerial EconomicsssssAgha TaimoorNo ratings yet

- Price Determination in Different Markets: Unit - 1: Meaning and Types of MarketsDocument12 pagesPrice Determination in Different Markets: Unit - 1: Meaning and Types of MarketsPriyanshu SharmaNo ratings yet

- PPT-CO3-Market FormsDocument67 pagesPPT-CO3-Market FormsSARAH SIKHANo ratings yet

- ECO XII - Topic X (FORMS OF MARKET)Document17 pagesECO XII - Topic X (FORMS OF MARKET)Tanisha PoddarNo ratings yet

- Micro PresentationDocument24 pagesMicro Presentationrakibsarkar619No ratings yet

- Market StructureDocument20 pagesMarket StructureSunny RajpalNo ratings yet

- Business Economics Unit 4Document29 pagesBusiness Economics Unit 4Kainos GreyNo ratings yet

- Mefa Unit-3Document20 pagesMefa Unit-3rosieNo ratings yet

- Economics, Market StructureDocument4 pagesEconomics, Market StructureJulliena BakersNo ratings yet

- TCW Module 3Document17 pagesTCW Module 3John Laurence OrbeNo ratings yet

- Impact Analysis of Market Structure On Supply of Goods in The Market.Document21 pagesImpact Analysis of Market Structure On Supply of Goods in The Market.Vritika ChanjotraNo ratings yet

- U 3 NotesDocument29 pagesU 3 NotesSuryansh RantaNo ratings yet

- Intro To Eco Chapter FiveDocument36 pagesIntro To Eco Chapter Fivegetasew muluyeNo ratings yet

- Economics - Vihaan ChaudharyDocument27 pagesEconomics - Vihaan Chaudharyvihaan chaudharyNo ratings yet

- Pbea Unit-IiiDocument24 pagesPbea Unit-IiiYugandhar YugandharNo ratings yet

- Perfect Competition-Term ReportDocument40 pagesPerfect Competition-Term ReportTalha HameedNo ratings yet

- THE Contemporary World: Market IntegrationDocument8 pagesTHE Contemporary World: Market IntegrationChristian Marzan100% (1)

- Mefa Unit-IiiDocument35 pagesMefa Unit-IiiGANDLA GOWTHAMI CSENo ratings yet

- Managerial EconomicsDocument33 pagesManagerial EconomicsajayghangareNo ratings yet

- Mb1102 Me - U III - Dr.r.arunDocument47 pagesMb1102 Me - U III - Dr.r.arunDr. R. ArunNo ratings yet

- Market and Agricultural MarketingDocument13 pagesMarket and Agricultural MarketingKIRUTHIKANo ratings yet

- Project For First Semester: MarketDocument22 pagesProject For First Semester: MarketShravan SisodiyaNo ratings yet

- Business Economics Unit 4Document30 pagesBusiness Economics Unit 4Kainos GreyNo ratings yet

- Perfect CompetitionDocument30 pagesPerfect CompetitionBhavesh BajajNo ratings yet

- Eco - Module 1 - Unit 3Document8 pagesEco - Module 1 - Unit 3Kartik PuranikNo ratings yet

- Project On Commodity MarketDocument46 pagesProject On Commodity Marketprajuprathu50% (2)

- Market SituationsDocument6 pagesMarket SituationsAndrew BuffeNo ratings yet

- Unit IDocument16 pagesUnit IRomi SNo ratings yet

- Gray and Blue Simple Teacher ResumeDocument2 pagesGray and Blue Simple Teacher ResumeRomi SNo ratings yet

- Bauxite ResDocument3 pagesBauxite ResKruti GaliaNo ratings yet

- IMYB 2011 - Graphite PDFDocument12 pagesIMYB 2011 - Graphite PDFRomi SNo ratings yet

- Obc Department GRDocument2 pagesObc Department GRRomi SNo ratings yet

- Assam, India: Valley of Tea and TemplesDocument20 pagesAssam, India: Valley of Tea and TemplesAmrit Baruah100% (5)

- MPSC Forest Pre 2016 Exam PaperDocument40 pagesMPSC Forest Pre 2016 Exam Paperabhijeet834u100% (1)

- 24 1 2013 21 41 9 Mining - LeasesDocument41 pages24 1 2013 21 41 9 Mining - LeasesRomi SNo ratings yet

- The Last Leaf PDFDocument5 pagesThe Last Leaf PDFRomi SNo ratings yet

- Master PlanDocument25 pagesMaster Plandev_1989No ratings yet

- Statistical Profiles of Minerals2010-11Document132 pagesStatistical Profiles of Minerals2010-11Romi SNo ratings yet

- ML Exp AfterDocument151 pagesML Exp AfterRomi SNo ratings yet

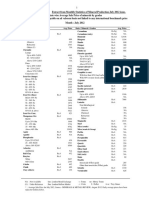

- Avgvalueall Jul12Document6 pagesAvgvalueall Jul12Romi SNo ratings yet

- Avgvalueall Dec11Document6 pagesAvgvalueall Dec11Romi SNo ratings yet

- Bauxite ResDocument3 pagesBauxite ResKruti GaliaNo ratings yet

- TipsDocument4 pagesTipsZeus SkNo ratings yet

- Kramnik Openings WcoDocument12 pagesKramnik Openings WcoAlberto MuguerzaNo ratings yet

- QuestionnaireDocument5 pagesQuestionnaireJay Hong PuiNo ratings yet

- A Tale of Two DonutsDocument4 pagesA Tale of Two DonutsBui Duy DucNo ratings yet

- Super Crisp ReportDocument24 pagesSuper Crisp ReportHassan Gilani100% (1)

- Conomics: Measuring A Nation ' S IncomeDocument13 pagesConomics: Measuring A Nation ' S IncomeMuhammad Aditya TMNo ratings yet

- Porter ExamDocument1 pagePorter ExamElvis Ortega LandeoNo ratings yet

- Marketing Management - II MNG615: Case - 2 RIN in PakistanDocument4 pagesMarketing Management - II MNG615: Case - 2 RIN in PakistanGopichand AthukuriNo ratings yet

- Exercises PartI CLEF Full PDFDocument23 pagesExercises PartI CLEF Full PDFAnonymous g7BcFkHJ0gNo ratings yet

- Aqua Mini ProjectDocument7 pagesAqua Mini ProjectSasa LiliNo ratings yet

- Full ChapterDocument87 pagesFull Chapterk VijayNo ratings yet

- 07a) Income Elasticity of DemandDocument3 pages07a) Income Elasticity of DemandMohamed YasserNo ratings yet

- BTL Atl & TTLDocument4 pagesBTL Atl & TTLPratyaya MitraNo ratings yet

- Agricultural Marketing Environment in AssamDocument7 pagesAgricultural Marketing Environment in AssamobijitNo ratings yet

- Marketing Management FinalDocument22 pagesMarketing Management FinalRadhey Sham SNo ratings yet

- IS-LM ModelDocument6 pagesIS-LM ModelAnand Kant JhaNo ratings yet

- Every SBU Is Profit Center But Every Profit Center Is Not SBUDocument1 pageEvery SBU Is Profit Center But Every Profit Center Is Not SBUNikita NagdevNo ratings yet

- Manual Oranginal Master 3eqDocument1 pageManual Oranginal Master 3eqEdson CarvalhoNo ratings yet

- Submit MipDocument38 pagesSubmit MipArchchana Vek Suren100% (5)

- Marketing of Financial Products CH 5Document26 pagesMarketing of Financial Products CH 5karim kobeissiNo ratings yet

- Consumer's EquilibriumDocument4 pagesConsumer's EquilibriumMahendra ChhetriNo ratings yet

- Youtube Insights: What 18-34 Year Olds Want From BrandsDocument12 pagesYoutube Insights: What 18-34 Year Olds Want From BrandsDerek E. Baird100% (1)

- Review of LiteratureDocument2 pagesReview of LiteratureShams SNo ratings yet

- Advertising and AudienceDocument48 pagesAdvertising and AudienceDavid GlenNo ratings yet

- Report-Observation Hari FinishDocument10 pagesReport-Observation Hari FinishRoneyz'foldism Part IINo ratings yet

- Op-Ed PaperDocument2 pagesOp-Ed Paperapi-252908727No ratings yet

- 15 Questionnaire PDFDocument14 pages15 Questionnaire PDFvidyashree patilNo ratings yet

- Samsung Electronics: South KoreaDocument37 pagesSamsung Electronics: South KoreaRama DeviNo ratings yet

- Gordon College: Detailed Learning Module Title: Developing A Business Plan (DP) Module No. 3Document7 pagesGordon College: Detailed Learning Module Title: Developing A Business Plan (DP) Module No. 3Jiellen Mei GarciaNo ratings yet

- PCI July 2011Document72 pagesPCI July 2011Darrell TanNo ratings yet

- Consumer Theory (Summary) Uc3mDocument12 pagesConsumer Theory (Summary) Uc3mlaraNo ratings yet

- Basic Premises and Specific Relevance of Corporate Social ResponsibilityDocument2 pagesBasic Premises and Specific Relevance of Corporate Social ResponsibilitySheila Mae Guerta Lacerona71% (7)

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)

- Look Again: The Power of Noticing What Was Always ThereFrom EverandLook Again: The Power of Noticing What Was Always ThereRating: 5 out of 5 stars5/5 (3)

- The Meth Lunches: Food and Longing in an American CityFrom EverandThe Meth Lunches: Food and Longing in an American CityRating: 5 out of 5 stars5/5 (5)

- Anarchy, State, and Utopia: Second EditionFrom EverandAnarchy, State, and Utopia: Second EditionRating: 3.5 out of 5 stars3.5/5 (180)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (8)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaFrom EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNo ratings yet

- Economics 101: How the World WorksFrom EverandEconomics 101: How the World WorksRating: 4.5 out of 5 stars4.5/5 (34)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailFrom EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailRating: 4.5 out of 5 stars4.5/5 (237)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetFrom EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNo ratings yet

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsFrom EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsRating: 4.5 out of 5 stars4.5/5 (94)

- This Changes Everything: Capitalism vs. The ClimateFrom EverandThis Changes Everything: Capitalism vs. The ClimateRating: 4 out of 5 stars4/5 (349)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (228)

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistFrom EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistRating: 4.5 out of 5 stars4.5/5 (37)

- AP Microeconomics/Macroeconomics Premium, 2024: 4 Practice Tests + Comprehensive Review + Online PracticeFrom EverandAP Microeconomics/Macroeconomics Premium, 2024: 4 Practice Tests + Comprehensive Review + Online PracticeNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The New Elite: Inside the Minds of the Truly WealthyFrom EverandThe New Elite: Inside the Minds of the Truly WealthyRating: 4 out of 5 stars4/5 (10)

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsFrom EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsRating: 5 out of 5 stars5/5 (3)

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentFrom EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentRating: 4.5 out of 5 stars4.5/5 (92)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomFrom EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNo ratings yet