You might also like

- Co Operative Housing SocietyDocument29 pagesCo Operative Housing Societyvenkynaidu100% (1)

- Co-Operative Housing SocietyDocument29 pagesCo-Operative Housing SocietyVish Patilvs67% (3)

- Project On Co Operative Society India PDFDocument42 pagesProject On Co Operative Society India PDFRig VedNo ratings yet

- Final Account of C0-Oprative SocietyDocument22 pagesFinal Account of C0-Oprative SocietyKomalNo ratings yet

- Visit To A Co Operative SocietyDocument15 pagesVisit To A Co Operative SocietySOHEL BANGI75% (4)

- A STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Document29 pagesA STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Pankaj Rathod67% (3)

- Financial AccountingDocument36 pagesFinancial Accountingkhanafsha100% (1)

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- Cooperative Society M.com 2Document27 pagesCooperative Society M.com 2Shankari MaharajanNo ratings yet

- Introduction To Project Report:: Shiva Credit Co-Operative Society LimitedDocument83 pagesIntroduction To Project Report:: Shiva Credit Co-Operative Society Limitedpmcmbharat264No ratings yet

- Project ReportDocument7 pagesProject ReportTushar Mathur100% (1)

- Neelam ReportDocument86 pagesNeelam Reportrjjain07100% (2)

- The Ayali Kalan Co-Operative Agricultural Multipurpose Society LimitedDocument51 pagesThe Ayali Kalan Co-Operative Agricultural Multipurpose Society LimitedRamandeep Grewal100% (1)

- Cooperative SocietyDocument4 pagesCooperative SocietyPanav MohindraNo ratings yet

- Banking Regulation ActDocument19 pagesBanking Regulation Actgattani.swatiNo ratings yet

- Black Book ProjectDocument64 pagesBlack Book ProjectMaanav Vasant100% (1)

- A Study On The Urban Cooperative Banks Success and Growth in Vellore DistrictDocument4 pagesA Study On The Urban Cooperative Banks Success and Growth in Vellore DistrictSrikara AcharyaNo ratings yet

- Credit Rating Agency in IndiaDocument81 pagesCredit Rating Agency in IndiaMaaz Kazi100% (1)

- Income From Other SourcesDocument7 pagesIncome From Other Sourcesshankarinadar100% (1)

- Ty Baf Sem Vi All Sample Question PaperDocument35 pagesTy Baf Sem Vi All Sample Question Paperjainam shahNo ratings yet

- Co OperativeDocument220 pagesCo OperativeMeenukutty MeenuNo ratings yet

- Sebi ProjectDocument70 pagesSebi Projectjaygujrati100% (2)

- SAPM Practice ProblemsDocument4 pagesSAPM Practice ProblemsMithun SagarNo ratings yet

- Kisan Credit Card ProjectDocument56 pagesKisan Credit Card Projectbhaskar sarma100% (1)

- An Analysis of Mergers & Acquisitions in The Indian Banking IndustryDocument48 pagesAn Analysis of Mergers & Acquisitions in The Indian Banking Industrydebasri_chatterjeeNo ratings yet

- Credit Rating in India - A Case For AccountabilityDocument66 pagesCredit Rating in India - A Case For AccountabilityArun Mishra100% (3)

- Effect of Taxation On Small BusinessDocument37 pagesEffect of Taxation On Small BusinessBhanu pratap singh100% (1)

- Buyback of SharesDocument70 pagesBuyback of SharesIshu TiwariNo ratings yet

- Funding of Mergers & TakeoversDocument31 pagesFunding of Mergers & TakeoversMohit MohanNo ratings yet

- Role of SidbiDocument51 pagesRole of SidbiDIVYA DUBEY93% (15)

- Project Report - Merger, Amalgamation, TakeoverDocument18 pagesProject Report - Merger, Amalgamation, TakeoverRohan kedia0% (1)

- Finance Project Report TopicsDocument4 pagesFinance Project Report TopicsLufang FengNo ratings yet

- Black Book ProjectDocument27 pagesBlack Book ProjectPragya SinghNo ratings yet

- Abhishek Blackbook FinalDocument95 pagesAbhishek Blackbook Final8784No ratings yet

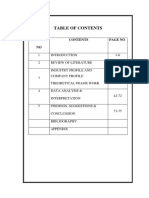

- NO Page No: 1 1-6 2 Review of Literature 7-11 Industry Profile and Company Profile Theoretical Frame Work 12-41Document89 pagesNO Page No: 1 1-6 2 Review of Literature 7-11 Industry Profile and Company Profile Theoretical Frame Work 12-41Sarin SayalNo ratings yet

- Mergers and Acquisitions in Banking IndustryDocument61 pagesMergers and Acquisitions in Banking IndustryPrateek Chawla100% (1)

- Lijjat PapadDocument6 pagesLijjat PapadNeeraj SoniNo ratings yet

- Powerpoint Presentation On FIIDocument13 pagesPowerpoint Presentation On FIIManali Rana100% (1)

- Analysis of Merger of SBIDocument5 pagesAnalysis of Merger of SBIAnuja AmiditNo ratings yet

- Project Report On Migration of People To PuneDocument20 pagesProject Report On Migration of People To PuneJamaal khanNo ratings yet

- Buyback of SharesDocument8 pagesBuyback of SharesBabitaKakkar100% (1)

- Organizational Study of The Perla Service Co-Operative Bank LTD No.c 3377Document37 pagesOrganizational Study of The Perla Service Co-Operative Bank LTD No.c 3377Fathima LibaNo ratings yet

- Evolution of Indian Financial Markets Certificates VarshaDocument7 pagesEvolution of Indian Financial Markets Certificates VarshaYukta Salvi0% (1)

- Economic Project On Banking Regulation Act 1949Document45 pagesEconomic Project On Banking Regulation Act 1949ezekielNo ratings yet

- Impact of GST On Automobile IndustryDocument3 pagesImpact of GST On Automobile Industrypvaibhav08No ratings yet

- Role of RBI in Economic Development of India PDFDocument18 pagesRole of RBI in Economic Development of India PDFTanmay Baranwal100% (7)

- Sales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingDocument67 pagesSales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingRishav Ch100% (1)

- Cooperative Credit Institutions PDFDocument96 pagesCooperative Credit Institutions PDFSumit BirlaNo ratings yet

- 7 Sbi, ProjectDocument54 pages7 Sbi, ProjecturjanagarNo ratings yet

- Project On Merger and Acquisition PDFDocument45 pagesProject On Merger and Acquisition PDFPabitraNo ratings yet

- State Co-Operative Bank LatestDocument29 pagesState Co-Operative Bank LatestAhana SenNo ratings yet

- A Projct Report On Cooperative SocietyDocument6 pagesA Projct Report On Cooperative Societymonikaagarwalitm333073% (15)

- Agricultural Finance and Project Management: Reserve Bank of IndiaDocument41 pagesAgricultural Finance and Project Management: Reserve Bank of IndiaPràßhánTh Aɭoŋɘ ɭovɘʀNo ratings yet

- Co-Op Soc.Document19 pagesCo-Op Soc.NainaNo ratings yet

- 68 Managemsnt and Leg DiscriptiveDocument10 pages68 Managemsnt and Leg DiscriptiveParames MuruganNo ratings yet

- Chapter-16 Audit of Co-Operative Societies: CA Ravi Taori Co-Op SocietyDocument8 pagesChapter-16 Audit of Co-Operative Societies: CA Ravi Taori Co-Op SocietyArpit ShuklaNo ratings yet

- The Cooperative Societies Act, 1925Document18 pagesThe Cooperative Societies Act, 1925Muzaffar IqbalNo ratings yet

- Cooperative Society V MultiDocument5 pagesCooperative Society V MultiMandira PriyaNo ratings yet

- RFBTDocument18 pagesRFBTHalsey Shih TzuNo ratings yet