You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Profit or Loss From Business: Schedule C (Form 1040) 09Document2 pagesProfit or Loss From Business: Schedule C (Form 1040) 09Braeylnn bookerNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- YesukoDocument1 pageYesukoraviNo ratings yet

- Pay Slip: Salary Slip - APR 2018 (Noida)Document1 pagePay Slip: Salary Slip - APR 2018 (Noida)rahul tyagiNo ratings yet

- GST NotesDocument14 pagesGST NotesPremajohnNo ratings yet

- Bar Examination Questions in TaxationDocument27 pagesBar Examination Questions in TaxationKevin Chrysler MarcoNo ratings yet

- Methods of DepreciationDocument12 pagesMethods of Depreciationamun din100% (1)

- EinDocument1 pageEinruovzuffNo ratings yet

- Philippine Amusement and Gaming Corporation (PAGCOR) vs. Commissioner of Internal Revenue, 846 SCRA 340, November 22, 2017Document27 pagesPhilippine Amusement and Gaming Corporation (PAGCOR) vs. Commissioner of Internal Revenue, 846 SCRA 340, November 22, 2017Christopher IgnacioNo ratings yet

- Republic Vs PatanaoDocument1 pageRepublic Vs PatanaoAnonymous XsaqDYDNo ratings yet

- PKF WWTG 2020 2021 OnlineDocument1,207 pagesPKF WWTG 2020 2021 OnlineHussain MunshiNo ratings yet

- Cir Vs Pineda 21 Scra 105Document4 pagesCir Vs Pineda 21 Scra 105Atty JV AbuelNo ratings yet

- Computation - Vijay SharmaDocument2 pagesComputation - Vijay Sharmaankit sharmaNo ratings yet

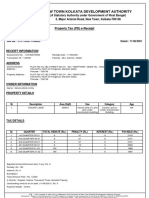

- New Town Kolkata Development Authority: Property Tax (PD) E-ReceiptDocument2 pagesNew Town Kolkata Development Authority: Property Tax (PD) E-ReceiptSSK DEVELOPERSNo ratings yet

- AY2022-23 REACHMEE PRIVATE LIMITED-AALCR1757K-ComputationDocument3 pagesAY2022-23 REACHMEE PRIVATE LIMITED-AALCR1757K-ComputationGST BACANo ratings yet

- CONSTITUTION OF INDIA Article 269A - Levy and Collection of Goods and Services Tax in Course of Inter-State Trade or CommerceDocument1 pageCONSTITUTION OF INDIA Article 269A - Levy and Collection of Goods and Services Tax in Course of Inter-State Trade or CommerceAniruddh SinghaNo ratings yet

- Tax Calculator (Salaried Person) : Monthly SalaryDocument5 pagesTax Calculator (Salaried Person) : Monthly SalarySheeraz Ahmed MemonNo ratings yet

- Tax Invoice: Vridavaneshvari Date: 16-Sep-2021 Inv. No.: 1812733199Document1 pageTax Invoice: Vridavaneshvari Date: 16-Sep-2021 Inv. No.: 1812733199Swetha WariNo ratings yet

- Gging TagDocument14 pagesGging TagCaroline DonaldsonNo ratings yet

- 227 Tax AnalysisDocument25 pages227 Tax AnalysisBurton PhillipsNo ratings yet

- Residentia, Income FRM House Prpty Practiced QnsDocument6 pagesResidentia, Income FRM House Prpty Practiced Qnsavinu9932No ratings yet

- ING Bank v. CIR (2015)Document50 pagesING Bank v. CIR (2015)Rain CoNo ratings yet

- Respuesta de La Comisión Europea A La Consulta de España Sobre El IVA de Las MascarillasDocument2 pagesRespuesta de La Comisión Europea A La Consulta de España Sobre El IVA de Las MascarillasMaldita.esNo ratings yet

- p5101 - 2019-10-00 1Document53 pagesp5101 - 2019-10-00 1api-495108136No ratings yet

- Module 4 Lesson 10 Taxation Read... in Phil. His.Document5 pagesModule 4 Lesson 10 Taxation Read... in Phil. His.John Mark Candeluna EreniaNo ratings yet

- New Jersey Tax Guide: Buying or Selling A Home in New JerseyDocument9 pagesNew Jersey Tax Guide: Buying or Selling A Home in New Jerseynour abdallaNo ratings yet

- Chapter 2 ExerciseDocument5 pagesChapter 2 Exercisegirlyn abadillaNo ratings yet

- Simple GST Invoice For Single Rate of Goods and ServicesDocument8 pagesSimple GST Invoice For Single Rate of Goods and ServicesKM computer & online workNo ratings yet

- CH 10 CsolDocument47 pagesCH 10 Csolxuzhu5No ratings yet

- Item PicDocument4 pagesItem PicMukesh MakadiaNo ratings yet

- How Much Is The Distributable Income of The GPP?Document2 pagesHow Much Is The Distributable Income of The GPP?Katrina Dela CruzNo ratings yet