You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Swps Aws b2.1 X XXXDocument6 pagesSwps Aws b2.1 X XXXJose David Perez Torrico0% (1)

- Application Letter - Ayu Surya WerdaniDocument2 pagesApplication Letter - Ayu Surya WerdaniSuswoyo NingratNo ratings yet

- HidrometalurgiaDocument12 pagesHidrometalurgiaPedro Yedra100% (1)

- Gpa Research BrochureDocument28 pagesGpa Research Brochuresyukur10% (1)

- 26df1000 426164 1Document41 pages26df1000 426164 1Adela DumitraşcuNo ratings yet

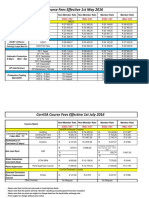

- Corrisa Course Fees Effective 1 May 2016Document2 pagesCorrisa Course Fees Effective 1 May 2016Prakash RajNo ratings yet

- Chapter 6 Section 2 OutlineDocument4 pagesChapter 6 Section 2 Outlineapi-263455056No ratings yet

- E01 PDFDocument28 pagesE01 PDFCarlos Orley Gil AmayaNo ratings yet

- LEC M4 Post Task 2 Organic ChemistryDocument3 pagesLEC M4 Post Task 2 Organic Chemistryhenry bernardNo ratings yet

- Adobe Scan 16 Nov 2022Document16 pagesAdobe Scan 16 Nov 2022Shaik mohammed NizamuddinNo ratings yet

- Melane Zintle Prac 1Document3 pagesMelane Zintle Prac 1Zintle MelaneNo ratings yet

- CPF Upgrade - PFD: Pkg-01 - Inlet Manifold SkidDocument15 pagesCPF Upgrade - PFD: Pkg-01 - Inlet Manifold SkidIbrahim DewaliNo ratings yet

- Unit 2 May19 Till Jan21Document306 pagesUnit 2 May19 Till Jan21Wael TareqNo ratings yet

- Enthalpy StoichiometryDocument1 pageEnthalpy StoichiometrykjjkimkmkNo ratings yet

- M. Naranjo Et Al. (2011) - CO2 - Capture - and - Sequestration - in - The - Cement - IndustDocument8 pagesM. Naranjo Et Al. (2011) - CO2 - Capture - and - Sequestration - in - The - Cement - IndustDavinder pal SinghNo ratings yet

- ATR Haldor TopsoeDocument12 pagesATR Haldor Topsoepraveenk_13100% (1)

- Fire Safetyquestion Paper CIE-3Document2 pagesFire Safetyquestion Paper CIE-3mohan hsNo ratings yet

- Separating MixturesDocument17 pagesSeparating MixturesLexelyn Pagara RivaNo ratings yet

- Boiler Efficiency CalculationsDocument65 pagesBoiler Efficiency CalculationssizmaruNo ratings yet

- Wobbe Index General Information Rev.1Document4 pagesWobbe Index General Information Rev.1Walid FattahNo ratings yet

- Ejercicios Resueltos InglesDocument4 pagesEjercicios Resueltos InglesAmparo OssaNo ratings yet

- ES DistillationDocument35 pagesES Distillationjoiesupremo100% (1)

- Cambridge Secondary Two Science: Chapter 8: MixturesDocument28 pagesCambridge Secondary Two Science: Chapter 8: MixturesarenestarNo ratings yet

- Enzymes PPT NotesDocument41 pagesEnzymes PPT NotesANWESHA BALNo ratings yet

- Process Design - EnggcyclopediaDocument6 pagesProcess Design - EnggcyclopediamshadabkNo ratings yet

- ISOTERM (Autosaved) (Autosaved) 1Document64 pagesISOTERM (Autosaved) (Autosaved) 1Fadhilatul AdhaNo ratings yet

- Sublimation:: Methods of Purification OF Organic CompoundsDocument11 pagesSublimation:: Methods of Purification OF Organic CompoundsAvi KedarrNo ratings yet

- 〈1228.3〉 Depyrogenation by FiltrationDocument4 pages〈1228.3〉 Depyrogenation by Filtrationmehrdarou.qaNo ratings yet

- Stage Separation of Gas-CondensateDocument2 pagesStage Separation of Gas-CondensateRifka AisyahNo ratings yet

- Quofumitat: (12) United States PatentDocument12 pagesQuofumitat: (12) United States PatentAnonymous tIwg2AyNo ratings yet