You might also like

- PC-16 TEST PAPER II: 75 QUESTIONS ON CIVIL ACCOUNTSDocument19 pagesPC-16 TEST PAPER II: 75 QUESTIONS ON CIVIL ACCOUNTSManoj SainiNo ratings yet

- TP Vii PDFDocument17 pagesTP Vii PDFshekarj100% (3)

- Pwa MCQDocument7 pagesPwa MCQSureshNo ratings yet

- CPWA CODE 101-150 (Guide Part 4) PDFDocument15 pagesCPWA CODE 101-150 (Guide Part 4) PDFshekarj80% (5)

- PC 16 - Practice Set 2Document14 pagesPC 16 - Practice Set 2Sumit Dahiya100% (1)

- PC-16 MCQ Rahi CPWA AllChaptersDocument150 pagesPC-16 MCQ Rahi CPWA AllChaptersVirendra Ramteke100% (1)

- Revenue Receipts ChapterDocument6 pagesRevenue Receipts ChapterVivek RatanNo ratings yet

- CPWA Code MCQDocument43 pagesCPWA Code MCQSamrat Mukherjee100% (3)

- Multiple Choices Questions Chapter 22: Accounts of The Divisional OfficeDocument23 pagesMultiple Choices Questions Chapter 22: Accounts of The Divisional OfficeVivek Ratan100% (2)

- CPWA CODE 51-100 (Guide Part 3) PDFDocument15 pagesCPWA CODE 51-100 (Guide Part 3) PDFshekarj67% (3)

- Forest Accounts MCQDocument12 pagesForest Accounts MCQAJAY DIMRINo ratings yet

- Civil Accounts Manual, (Chapter 4) : (A) Ministry of FinanceDocument6 pagesCivil Accounts Manual, (Chapter 4) : (A) Ministry of FinanceManohar SharmaNo ratings yet

- CPWA CODE 1-50 (Guide Part 2) PDFDocument15 pagesCPWA CODE 1-50 (Guide Part 2) PDFshekarj88% (16)

- MCQ EWO CPWA Code Q 01 50 Merged 20210331153535Document58 pagesMCQ EWO CPWA Code Q 01 50 Merged 20210331153535Sanjitkumar SarkarNo ratings yet

- PC 16 - MCQ - Rahi - CPWA - Appendix - AnsDocument4 pagesPC 16 - MCQ - Rahi - CPWA - Appendix - AnsVirendra Ramteke100% (1)

- MCQ - CPWD CHAPTER 5 - CashDocument9 pagesMCQ - CPWD CHAPTER 5 - CashBeauty Queen100% (1)

- Transfer Entry ChapterDocument4 pagesTransfer Entry ChapterBeauty Queen100% (2)

- Uniform Format of Accounts - SummaryDocument8 pagesUniform Format of Accounts - SummaryGotta Patti House100% (1)

- PC 8 - Practice Set 1Document11 pagesPC 8 - Practice Set 1RAM KUMARNo ratings yet

- PC 8 - Receipt and Payment 1983Document20 pagesPC 8 - Receipt and Payment 1983ARAVIND K100% (4)

- Receipt - Payment Rules - Point WiseDocument11 pagesReceipt - Payment Rules - Point WiseRAKESHNo ratings yet

- CAM Chapter 1Document9 pagesCAM Chapter 1Manohar SharmaNo ratings yet

- CPWA Code BriefDocument301 pagesCPWA Code BriefSamrat MukherjeeNo ratings yet

- PC8 Answer: Capsule 16: Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)Document2 pagesPC8 Answer: Capsule 16: Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)bibhorji Rusiya100% (1)

- MSO A & E Chapter 8 & 9 (Guide Part 1) PDFDocument21 pagesMSO A & E Chapter 8 & 9 (Guide Part 1) PDFshekarj100% (8)

- Government Accounting & Financial RulesDocument9 pagesGovernment Accounting & Financial RulesSouvik DattaNo ratings yet

- 16.forest Accounts MCQ - AdditionalDocument5 pages16.forest Accounts MCQ - AdditionalSatya PrakashNo ratings yet

- Government Accounting Rules, 1990 (2019-Edition) : Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)Document16 pagesGovernment Accounting Rules, 1990 (2019-Edition) : Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)ARAVIND K100% (2)

- MSO Chapter 8 & 9 ObjDocument22 pagesMSO Chapter 8 & 9 ObjsantaNo ratings yet

- GFR FormsDocument2 pagesGFR FormsSaurav GhoshNo ratings yet

- Multiple Choice Questions (Appendix To CPWA Code) Appendix 2Document23 pagesMultiple Choice Questions (Appendix To CPWA Code) Appendix 2Virendra Ramteke100% (1)

- MCQ - CPWD CHAPTER 9 - Works AccountsDocument41 pagesMCQ - CPWD CHAPTER 9 - Works AccountsBeauty Queen75% (4)

- DPC ActDocument16 pagesDPC ActSaurav GhoshNo ratings yet

- Preared by Krishnamraju (O/O Cda Secunderabad) : Cag DPC Act-1971Document6 pagesPreared by Krishnamraju (O/O Cda Secunderabad) : Cag DPC Act-1971Booth Tuckers100% (1)

- DEFENCE Account CODE PDFDocument12 pagesDEFENCE Account CODE PDFkhaja1988No ratings yet

- MCQ CPWA Code Chapter-10Document14 pagesMCQ CPWA Code Chapter-10Biswajit JenaNo ratings yet

- Government Accounting Rules SummaryDocument9 pagesGovernment Accounting Rules SummaryRAKESH100% (3)

- Government Employee Pay RulesDocument3 pagesGovernment Employee Pay RulesNRKNo ratings yet

- CIVIL Accounts Manual (Chapter 3) : (B) by Pay and Accounts Office of The Ministry/Dept. After Proper Pre-CheckDocument4 pagesCIVIL Accounts Manual (Chapter 3) : (B) by Pay and Accounts Office of The Ministry/Dept. After Proper Pre-CheckManohar SharmaNo ratings yet

- CH8 TransferEntriesDocument20 pagesCH8 TransferEntriesshekarj100% (1)

- Objective QuestionsDocument11 pagesObjective Questionsshekarj50% (2)

- Ncert Books PDF: General Financial Rules 2017 CHAPTER 12: MISCELLANEOUS SubjectsDocument5 pagesNcert Books PDF: General Financial Rules 2017 CHAPTER 12: MISCELLANEOUS SubjectsRISHABH TOMAR100% (1)

- Enquiry Regarding Token Numbers of Outstanding Pre-Check BillsDocument3 pagesEnquiry Regarding Token Numbers of Outstanding Pre-Check BillsARAVIND K100% (1)

- Multiple Choice Questions On Government Accounts Test Paper (Negative Marking @1/4 For Each Wrong Answer) Time Allowed: 1 Hour Max Marks 50Document4 pagesMultiple Choice Questions On Government Accounts Test Paper (Negative Marking @1/4 For Each Wrong Answer) Time Allowed: 1 Hour Max Marks 50IlhamNo ratings yet

- Defence Audit CodeDocument5 pagesDefence Audit Codekinnark100% (2)

- CCS (CCA) Rules 1965 20.1Document127 pagesCCS (CCA) Rules 1965 20.1mbanlj33% (3)

- CPWA CODE 151-200 (Guide Part 5) PDFDocument13 pagesCPWA CODE 151-200 (Guide Part 5) PDFshekarj0% (1)

- MCQ - PC 21 - Civil Accounts Manual (CAM)Document13 pagesMCQ - PC 21 - Civil Accounts Manual (CAM)DEVI SINGH MEENANo ratings yet

- IT Audit Manual-Volume. I: B. II and IIIDocument32 pagesIT Audit Manual-Volume. I: B. II and IIIsreekanth50% (2)

- GAR 1990 Practice TestDocument15 pagesGAR 1990 Practice TestDGACE DDO100% (5)

- CPWD Accountants CodeDocument273 pagesCPWD Accountants CodeVishalagNo ratings yet

- Receipts and Payment Rules 1983 Notes For Sas ExamDocument7 pagesReceipts and Payment Rules 1983 Notes For Sas ExamSamrat Mukherjee33% (3)

- General Financial Rules 2017Document62 pagesGeneral Financial Rules 2017ADITYA GAHLAUT0% (1)

- Test Paper No: Vi (Forest Accounts) : Total QuestionsDocument13 pagesTest Paper No: Vi (Forest Accounts) : Total QuestionsManoj SainiNo ratings yet

- Test 1Document8 pagesTest 1Shivam SinghNo ratings yet

- 25022022 Ga Ep Module II Ns Dec21Document86 pages25022022 Ga Ep Module II Ns Dec21j2533015No ratings yet

- Cpwa MCQDocument11 pagesCpwa MCQSamrat Mukherjee100% (4)

- NOTE: All The References To Sections Mentioned in Part-A and Part-C of The Question PaperDocument8 pagesNOTE: All The References To Sections Mentioned in Part-A and Part-C of The Question Papersheena2saNo ratings yet

- 65 - COMMERCE - FINANCIAL ACCOUNTING - 653 - (13-12-2019 07 - 47 - 17 - 372 AM) Mahesh4Document9 pages65 - COMMERCE - FINANCIAL ACCOUNTING - 653 - (13-12-2019 07 - 47 - 17 - 372 AM) Mahesh4Mahesh KharatNo ratings yet

- It - (Theory) Nov., 2007Document15 pagesIt - (Theory) Nov., 2007Jitendra VernekarNo ratings yet

- 2.auditing Standards For Sas PC 22Document33 pages2.auditing Standards For Sas PC 22shekarj100% (1)

- CPWD Accountants CodeDocument273 pagesCPWD Accountants CodeVishalagNo ratings yet

- 6 EngDocument154 pages6 Engbhaskar0% (1)

- CPWA CODE 51-100 (Guide Part 3) PDFDocument15 pagesCPWA CODE 51-100 (Guide Part 3) PDFshekarj67% (3)

- Book of Forms CPWADocument168 pagesBook of Forms CPWAkhan_sadi0% (2)

- New ServiceDocument1 pageNew ServiceshekarjNo ratings yet

- CPWA CODE 151-200 (Guide Part 5) PDFDocument13 pagesCPWA CODE 151-200 (Guide Part 5) PDFshekarj0% (1)

- Answer Key - Test Paper Vii: Questio Nno Correct Answer ReferenceDocument2 pagesAnswer Key - Test Paper Vii: Questio Nno Correct Answer ReferenceshekarjNo ratings yet

- MSO A & E Chapter 8 & 9 (Guide Part 1) PDFDocument21 pagesMSO A & E Chapter 8 & 9 (Guide Part 1) PDFshekarj100% (8)

- CPWD DistinDocument9 pagesCPWD DistinshekarjNo ratings yet

- CPWA CODE 1-50 (Guide Part 2) PDFDocument15 pagesCPWA CODE 1-50 (Guide Part 2) PDFshekarj88% (16)

- Notes On CPWD PDFDocument70 pagesNotes On CPWD PDFshekarj92% (26)

- Roshan Notes On CPWADocument89 pagesRoshan Notes On CPWAshekarj100% (9)

- CPWD EssayDocument71 pagesCPWD Essayshekarj50% (2)

- Forms & NoDocument5 pagesForms & Noshekarj100% (4)

- CH8 TransferEntriesDocument20 pagesCH8 TransferEntriesshekarj100% (1)

- CPWD ShortDocument10 pagesCPWD Shortshekarj33% (3)

- Office Six Calbro House Tuam Road Galway Tel: 091 756229 Web: WWW - Asthmacare.ieDocument47 pagesOffice Six Calbro House Tuam Road Galway Tel: 091 756229 Web: WWW - Asthmacare.ieshekarjNo ratings yet

- Objective QuestionsDocument11 pagesObjective Questionsshekarj50% (2)

- GapAna Gap Trading StrategyDocument440 pagesGapAna Gap Trading Strategyshekarj67% (3)

- Summary judgment on pleadingsDocument3 pagesSummary judgment on pleadingsVloudy Mia Serrano PangilinanNo ratings yet

- Intern Non-Disclosure Agreement: Article I: Scope of AgreementDocument5 pagesIntern Non-Disclosure Agreement: Article I: Scope of Agreementfeel free userNo ratings yet

- Rules of Origin Are Used To Determine TheDocument4 pagesRules of Origin Are Used To Determine TheLeema AlasaadNo ratings yet

- Soriano vs. PeopleDocument3 pagesSoriano vs. Peoplek santosNo ratings yet

- Public Policy and The Arts 2009 SyllabusDocument11 pagesPublic Policy and The Arts 2009 SyllabusMichael RushtonNo ratings yet

- STATUTORY CONSTRUCTION LATIN MAXIMSDocument10 pagesSTATUTORY CONSTRUCTION LATIN MAXIMSIa BolosNo ratings yet

- Geriatric Nursing: Saint Louis UniversityDocument5 pagesGeriatric Nursing: Saint Louis UniversityDannielle Kathrine JoyceNo ratings yet

- 5 PNB v. Asuncion G.R. No. L 46095Document2 pages5 PNB v. Asuncion G.R. No. L 46095Najmah DirangarunNo ratings yet

- Technosoft License Agreement PDFDocument12 pagesTechnosoft License Agreement PDFRoberto TorresNo ratings yet

- People Vs Degamo April 30 2003Document2 pagesPeople Vs Degamo April 30 2003Vance CeballosNo ratings yet

- Introduction To Philippine Criminal Justice SystemDocument68 pagesIntroduction To Philippine Criminal Justice SystemLouvieBuhayNo ratings yet

- USA V Baladian Nov 29, 2021 Protective Order Re DiscoveryDocument6 pagesUSA V Baladian Nov 29, 2021 Protective Order Re DiscoveryFile 411No ratings yet

- SOP Contingent I Hiring ProcessDocument15 pagesSOP Contingent I Hiring ProcesskausarNo ratings yet

- The Nay Pyi Taw Development Law PDFDocument7 pagesThe Nay Pyi Taw Development Law PDFaung myoNo ratings yet

- Guaranteed Tobacco Arrival Condition DisputeDocument12 pagesGuaranteed Tobacco Arrival Condition DisputeFaye Cience BoholNo ratings yet

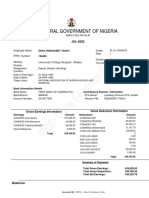

- Federal Pay Slip for Margaret Taiwo GiwaDocument1 pageFederal Pay Slip for Margaret Taiwo GiwaHalleluyah HalleluyahNo ratings yet

- Perfam Mendoza To LiyaoDocument30 pagesPerfam Mendoza To Liyaoeugenebriones27yahoo.comNo ratings yet

- Teoría Producción Por LotesDocument3 pagesTeoría Producción Por LotesGedeón PizarroNo ratings yet

- Colinares vs. PeopleDocument2 pagesColinares vs. PeopleMichelle Montenegro - AraujoNo ratings yet

- BLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Document4 pagesBLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Chasmere MagloyuanNo ratings yet

- Quasi Judicial Funtion of Administrative BodiesDocument18 pagesQuasi Judicial Funtion of Administrative BodiesSwati KritiNo ratings yet

- Comelec Nanawagan Sa Payapang Halalan 2022: Comelec Gives In: Voter Registration To Be Extended Until October 31Document1 pageComelec Nanawagan Sa Payapang Halalan 2022: Comelec Gives In: Voter Registration To Be Extended Until October 31John Paul ObleaNo ratings yet

- Is Silence Truly AcquiessenceDocument9 pagesIs Silence Truly Acquiessencebmhall65100% (1)

- 2 Sebastian vs. Morales, 445 Phil. 595Document2 pages2 Sebastian vs. Morales, 445 Phil. 595loschudentNo ratings yet

- Comfort Women Seek Official Apology from JapanDocument4 pagesComfort Women Seek Official Apology from JapanCistron ExonNo ratings yet

- United States v. Juan Carlos Huerta-Moran, Also Known As Francisco Lozano, 352 F.3d 766, 2d Cir. (2003)Document9 pagesUnited States v. Juan Carlos Huerta-Moran, Also Known As Francisco Lozano, 352 F.3d 766, 2d Cir. (2003)Scribd Government DocsNo ratings yet

- Discuss The Different Modes of Filing Patent in Foreign CountriesDocument7 pagesDiscuss The Different Modes of Filing Patent in Foreign Countrieshariom bajpaiNo ratings yet

- Po1 Recruitment Application Form: Cabannag Cherry Mae Licuben Taripan, Malibcong, Abra, Car 2820Document1 pagePo1 Recruitment Application Form: Cabannag Cherry Mae Licuben Taripan, Malibcong, Abra, Car 2820Angeline CabannagNo ratings yet

- Caridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Document1 pageCaridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Archibald Jose Tiago ManansalaNo ratings yet

- Sample Deed of Absolute Sale of SharesDocument3 pagesSample Deed of Absolute Sale of SharesGela Bea BarriosNo ratings yet