You might also like

- F8AA SQB Conts - j08Document6 pagesF8AA SQB Conts - j08FamilyLife MinistriesheartofourexistenceNo ratings yet

- F8AA (IntRQB-As d08Document168 pagesF8AA (IntRQB-As d08FamilyLife MinistriesheartofourexistenceNo ratings yet

- Operations Management: Date: May 19, 2014Document16 pagesOperations Management: Date: May 19, 2014FamilyLife MinistriesheartofourexistenceNo ratings yet

- Audit and Assurance (International) : F8AA-MT1A-X08-A Answers & Marking SchemeDocument10 pagesAudit and Assurance (International) : F8AA-MT1A-X08-A Answers & Marking SchemeFamilyLife MinistriesheartofourexistenceNo ratings yet

- Insert Policy Title Here: (PURDUE UNIVERSITY POLICY TEMPLATE: All Sections Are Mandatory UnlessDocument3 pagesInsert Policy Title Here: (PURDUE UNIVERSITY POLICY TEMPLATE: All Sections Are Mandatory UnlessFamilyLife MinistriesheartofourexistenceNo ratings yet

- 2015 Ritc Team Registration FormDocument1 page2015 Ritc Team Registration FormFamilyLife MinistriesheartofourexistenceNo ratings yet

- VerbalDocument1 pageVerbalFamilyLife MinistriesheartofourexistenceNo ratings yet

- (146790355) Final - AssignmentDocument6 pages(146790355) Final - AssignmentFamilyLife MinistriesheartofourexistenceNo ratings yet

- PP Basic Rules UnderstandsdDocument28 pagesPP Basic Rules UnderstandsdFamilyLife MinistriesheartofourexistenceNo ratings yet

- Oa Sbadoc!Document14 pagesOa Sbadoc!FamilyLife Ministriesheartofourexistence0% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- This Problem Continues The Daniels Consulting Situation From Problem p4 40 PDFDocument1 pageThis Problem Continues The Daniels Consulting Situation From Problem p4 40 PDFAhsan KhanNo ratings yet

- How Has This Company Returned Cash To Its Owners? Has It Paid Dividends or Bought Back Stock?Document3 pagesHow Has This Company Returned Cash To Its Owners? Has It Paid Dividends or Bought Back Stock?Mackaingar WalkerNo ratings yet

- Cma Inter Model Question Paper 3Document17 pagesCma Inter Model Question Paper 3dibakar100% (2)

- Preparation of Adjusting EntriesDocument25 pagesPreparation of Adjusting EntriesMemey C.100% (1)

- 2015 Itr1 PR9Document9 pages2015 Itr1 PR9Soumyaranjan SwainNo ratings yet

- F3 FFA Revision Mock B Answers D17Document12 pagesF3 FFA Revision Mock B Answers D17MAGIC TITANNo ratings yet

- Q4 Applied Entrepreneurship WK 5Document4 pagesQ4 Applied Entrepreneurship WK 5brylla monteroNo ratings yet

- Simple Cash Flow Template: Company Name Manager NameDocument7 pagesSimple Cash Flow Template: Company Name Manager NamehamisayubuNo ratings yet

- Management AccountingDocument8 pagesManagement AccountingSeddrinth DracoNo ratings yet

- BMO Balanced ETF Portfolio - Advisor: Reasons To Invest in The Fund Fund DetailsDocument2 pagesBMO Balanced ETF Portfolio - Advisor: Reasons To Invest in The Fund Fund DetailsJasonJin93No ratings yet

- Alchemy of A Pyraimd Scheme: Transmutating Business Opportunity Into A Negative Sum Wealth TransferDocument33 pagesAlchemy of A Pyraimd Scheme: Transmutating Business Opportunity Into A Negative Sum Wealth TransferThompson BurtonNo ratings yet

- Quiz - Business TaxesDocument4 pagesQuiz - Business TaxesFery Ann C. BravoNo ratings yet

- Mark Scheme (Results) : January 2019Document33 pagesMark Scheme (Results) : January 2019raiyan rahmanNo ratings yet

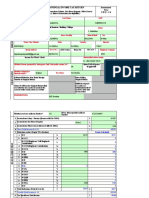

- Revenue and Expense Recognition, Income Statement Preparation, Procedure and Presentation of Income StatementDocument11 pagesRevenue and Expense Recognition, Income Statement Preparation, Procedure and Presentation of Income StatementAbigail Elsa Samita Sitakar 1902113687No ratings yet

- GBH1002 - Assignment 1 Instruction - SU21Document2 pagesGBH1002 - Assignment 1 Instruction - SU21Thảo Vân CaoNo ratings yet

- Business Plan PDFDocument25 pagesBusiness Plan PDFAbdul Waheed50% (2)

- Fin. Anal Rafael 3Document4 pagesFin. Anal Rafael 3MarjonNo ratings yet

- SettlementReportDocument1 pageSettlementReportBhanuranjan S BNo ratings yet

- Chapter 2 - Financial StatementsDocument4 pagesChapter 2 - Financial StatementsMASSO CALINTAANNo ratings yet

- Questions For EquityDocument11 pagesQuestions For EquityRãViï DrAxlerNo ratings yet

- Group Project 2 - Published Account DEC2019 FAR270 - SSDocument6 pagesGroup Project 2 - Published Account DEC2019 FAR270 - SSHaru BiruNo ratings yet

- Answer: CDocument4 pagesAnswer: CwendychenNo ratings yet

- Doctrine: An Alien Actually Present in The Philippines Who Is Not A Mere Transient or Sojourner IsDocument12 pagesDoctrine: An Alien Actually Present in The Philippines Who Is Not A Mere Transient or Sojourner IsGui EshNo ratings yet

- Comprehensive Exam ADocument12 pagesComprehensive Exam Ajdiaz_646247100% (2)

- Causes and Consequences of LBODocument25 pagesCauses and Consequences of LBODead EyeNo ratings yet

- 4.3. Profitability RatioDocument5 pages4.3. Profitability RatioKashmi VishnayaNo ratings yet

- 11 IGF Insights Tax Competition MiningDocument14 pages11 IGF Insights Tax Competition MiningErnesto CordovaNo ratings yet

- Unit 2: The Role and Importance of Financial ManagementDocument19 pagesUnit 2: The Role and Importance of Financial ManagementEsirael BekeleNo ratings yet

- PBRX Financial Report Dec 2018 (Audited)Document84 pagesPBRX Financial Report Dec 2018 (Audited)ronaldi lioeNo ratings yet

- W8 - AS5 - Statement of CashFlowsDocument1 pageW8 - AS5 - Statement of CashFlowsJere Mae MarananNo ratings yet