You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Waterflow Switch VSR - Potter ElectricDocument8 pagesWaterflow Switch VSR - Potter ElectricXioNo ratings yet

- (A) Introduction Ct01-LMDocument12 pages(A) Introduction Ct01-LMMohammed Anis FortasNo ratings yet

- APUSH SynthesisDocument1 pageAPUSH SynthesisthaticeskatergirlNo ratings yet

- Market BagDocument2 pagesMarket Bagpipistrila79No ratings yet

- Lecture 1Document45 pagesLecture 1rishita agarwalNo ratings yet

- Assignment # 1 STUDENT ID: mc090201864 MKT 501 (Marketing Management) SolutionDocument2 pagesAssignment # 1 STUDENT ID: mc090201864 MKT 501 (Marketing Management) SolutionImranNo ratings yet

- Consent LetterDocument3 pagesConsent LetterKishor KvNo ratings yet

- Lecture 1 - Intro and SolidWorks PCBDocument17 pagesLecture 1 - Intro and SolidWorks PCBmyturtle gameNo ratings yet

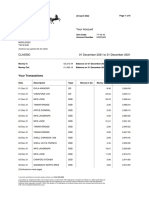

- Your AccountDocument6 pagesYour AccountJean FurtadoNo ratings yet

- Trends Networks and Critical Thinking - Q3 Module5Document8 pagesTrends Networks and Critical Thinking - Q3 Module5FrancineNo ratings yet

- Cramer's RuleDocument33 pagesCramer's RuleRauf BalochNo ratings yet

- MJ'S Collect ION: Acknowledgement ReceiptDocument2 pagesMJ'S Collect ION: Acknowledgement ReceiptMichael JAvonilloNo ratings yet

- Business Plan Cover PageDocument3 pagesBusiness Plan Cover PageBrille Adrian FernandoNo ratings yet

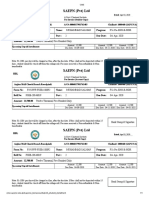

- SAEPN (PVT) LTD: Fee Invoice (Student Copy)Document1 pageSAEPN (PVT) LTD: Fee Invoice (Student Copy)waseemNo ratings yet

- Examen Final Semana 8 INGLES 1 1 INTENTODocument13 pagesExamen Final Semana 8 INGLES 1 1 INTENTOClaudia100% (1)

- Index NumbersDocument7 pagesIndex NumbersAllauddinaghaNo ratings yet

- 15 G Form (Pre-Filled)Document3 pages15 G Form (Pre-Filled)Ravi JammulaNo ratings yet

- Homework Chap 25Document2 pagesHomework Chap 25An leeNo ratings yet

- INB 372: Introduction To International Business: Country Report On: South SudanDocument33 pagesINB 372: Introduction To International Business: Country Report On: South SudanFahim HossainNo ratings yet

- Rights of Unpaid Seller Against The GoodsDocument16 pagesRights of Unpaid Seller Against The GoodsDharma TejaNo ratings yet

- Adjustment Codes.....Document2 pagesAdjustment Codes.....M RAFI US SAMADNo ratings yet

- Mahindra Codename Crown-Opp Doc - Hussain SemariDocument4 pagesMahindra Codename Crown-Opp Doc - Hussain Semarik.mouni14No ratings yet

- Proof of CashDocument22 pagesProof of CashYen RabotasoNo ratings yet

- Bmat Quizzes W1 10Document30 pagesBmat Quizzes W1 10Johndonrobert VargasNo ratings yet

- Annex 1-6-Cooperative Productive Society Fowa EnglishDocument3 pagesAnnex 1-6-Cooperative Productive Society Fowa EnglishWikileaks2024No ratings yet

- Practical Manual On Farm Management Production and Resource EconomicsDocument60 pagesPractical Manual On Farm Management Production and Resource Economicssaurabh r33% (3)

- Business Economics Sem 6Document14 pagesBusiness Economics Sem 6Rayyan PatelNo ratings yet

- SST 9th PEOPLE AS RESOURCE PRACTICE WORKSHEET SEPTEMBERDocument8 pagesSST 9th PEOPLE AS RESOURCE PRACTICE WORKSHEET SEPTEMBERPlay like pro.No ratings yet

- Jyske Bank Jun 24 FX Spot OnDocument29 pagesJyske Bank Jun 24 FX Spot OnMiir ViirNo ratings yet

- Detailed Advertisement English Nov22Document6 pagesDetailed Advertisement English Nov22VijayNo ratings yet