You might also like

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintFrom EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintRating: 4 out of 5 stars4/5 (1)

- 12th Book Keeping Board Papers PDFDocument50 pages12th Book Keeping Board Papers PDFRam IyerNo ratings yet

- E Book - Aml-Kyc and ComplianceDocument638 pagesE Book - Aml-Kyc and ComplianceGanesh Ramaiyer100% (1)

- Banking and Negotiable Instrument Notes2009-2010 Second SemesterDocument35 pagesBanking and Negotiable Instrument Notes2009-2010 Second SemesterRow- Da- Vitzky75% (4)

- Banco de Oro vs. Equitable Banking Corp., 157 SCRA 188Document16 pagesBanco de Oro vs. Equitable Banking Corp., 157 SCRA 188FD BalitaNo ratings yet

- Supreme Court Reports Annotated Voulme 157Document30 pagesSupreme Court Reports Annotated Voulme 157Tess TibayanNo ratings yet

- G.R. No. 74917 - Banco de Oro v. Equitable Banking CorpDocument13 pagesG.R. No. 74917 - Banco de Oro v. Equitable Banking CorpAj SobrevegaNo ratings yet

- 1988-Banco de Oro v. Equitable Banking Corp.Document11 pages1988-Banco de Oro v. Equitable Banking Corp.Kathleen MartinNo ratings yet

- BDO V Equitable Banking Corp. G.R. No.L-74917Document6 pagesBDO V Equitable Banking Corp. G.R. No.L-74917John Basil ManuelNo ratings yet

- BDO vs. Equitable Banking CorporationDocument7 pagesBDO vs. Equitable Banking Corporationmia_2109No ratings yet

- BDO V EBCDocument17 pagesBDO V EBCHanny LinNo ratings yet

- Case Midterm Law 3Document9 pagesCase Midterm Law 3Raña Marie Macaranas BobadillaNo ratings yet

- BPI v. CADocument23 pagesBPI v. CApistekayawaNo ratings yet

- BDO V EquitableDocument13 pagesBDO V EquitableMp CasNo ratings yet

- Banco de Oro Savings and Mortgage Bank VDocument4 pagesBanco de Oro Savings and Mortgage Bank VKDNo ratings yet

- BDO Vs EBCDocument1 pageBDO Vs EBCmargaserranoNo ratings yet

- Bank of America vs. Phil Racing Club 594 SCRA 301Document11 pagesBank of America vs. Phil Racing Club 594 SCRA 301easa^belleNo ratings yet

- Republic of The PhilippinesprintDocument23 pagesRepublic of The PhilippinesprintAldrinCruiseNo ratings yet

- BDO Savings V EBCDocument2 pagesBDO Savings V EBCcejotarresNo ratings yet

- 129179-1992-Bank of The Philippine Islands v. Court Of20210424-12-F7qjuzDocument26 pages129179-1992-Bank of The Philippine Islands v. Court Of20210424-12-F7qjuzLydia Marie Inocencio-MirabelNo ratings yet

- PNB Vs National City Bank of New YorkDocument14 pagesPNB Vs National City Bank of New YorkEphraimEnriquez25% (4)

- NIL DigestsDocument7 pagesNIL DigestsaugustofficialsNo ratings yet

- Banco de Oro Savings v. Equitable Banking Corp.Document10 pagesBanco de Oro Savings v. Equitable Banking Corp.Phulagyn CañedoNo ratings yet

- Division (Grno. L-74917, Jan 20, 1988) Banco de Oro Savings V. Equitable Banking CorporationDocument12 pagesDivision (Grno. L-74917, Jan 20, 1988) Banco de Oro Savings V. Equitable Banking CorporationSocNo ratings yet

- Nego Cases 15-17 (Digested)Document3 pagesNego Cases 15-17 (Digested)Supply ICPONo ratings yet

- Negotiable Instrument (Discharge of Instrument)Document15 pagesNegotiable Instrument (Discharge of Instrument)Sara Andrea Santiago100% (1)

- 4) Bank-of-America-NT-SA-vs.-Associated-Citizens-BankDocument14 pages4) Bank-of-America-NT-SA-vs.-Associated-Citizens-BankShien TumalaNo ratings yet

- G.R. No. 150228 BANK OF AMERICA NT & SA Vs PHILIPPINE RACING CLUBDocument10 pagesG.R. No. 150228 BANK OF AMERICA NT & SA Vs PHILIPPINE RACING CLUBJessie AncogNo ratings yet

- 43 - Wong v. CaDocument9 pages43 - Wong v. CaVia Rhidda ImperialNo ratings yet

- Bank of America NT & Sa, G.R. No. 150228Document5 pagesBank of America NT & Sa, G.R. No. 150228Rongee Larry Perez AboyNo ratings yet

- Bank of America Vs Philippine Racing Club 594 Scra 301Document7 pagesBank of America Vs Philippine Racing Club 594 Scra 301tintin murilloNo ratings yet

- G.R. No. 150228 Bank of America NT & Sa Vs Philippine Racing ClubDocument10 pagesG.R. No. 150228 Bank of America NT & Sa Vs Philippine Racing ClubJessie AncogNo ratings yet

- Metropolitan Bank and Trust Company vs. Junnel's Marketing CorporationDocument32 pagesMetropolitan Bank and Trust Company vs. Junnel's Marketing CorporationMiss JNo ratings yet

- Banco de Oro V Equitable Banking CorpDocument2 pagesBanco de Oro V Equitable Banking CorpJenNo ratings yet

- 06 Jai-Alai V BPIDocument12 pages06 Jai-Alai V BPIRaymond ChengNo ratings yet

- Bank of America NT & SA vs. Philippine Racing ClubDocument8 pagesBank of America NT & SA vs. Philippine Racing ClubKanshimNo ratings yet

- Bank of America vs. Associated Citizens BankDocument4 pagesBank of America vs. Associated Citizens BankGeenea VidalNo ratings yet

- 2form and Interpretation of NilDocument6 pages2form and Interpretation of NilRamos GabeNo ratings yet

- Jai Alai Vs BPI Facts: (2) Republic Vs Ebrada: NEGO Forgery Cases APR118Document11 pagesJai Alai Vs BPI Facts: (2) Republic Vs Ebrada: NEGO Forgery Cases APR118AlvinRelox100% (1)

- Philippine Commercial International Bank vs. BalmacedaDocument24 pagesPhilippine Commercial International Bank vs. BalmacedaShien TumalaNo ratings yet

- Wong v. Court of Appeals, G.R. No. 117857, February 02, 2001Document10 pagesWong v. Court of Appeals, G.R. No. 117857, February 02, 2001Krister VallenteNo ratings yet

- Cebu International Finance Corp. vs. CADocument10 pagesCebu International Finance Corp. vs. CASweet Zel Grace PorrasNo ratings yet

- BANCO DE ORO V EquitableDocument6 pagesBANCO DE ORO V Equitablejolly verbatimNo ratings yet

- G.R. No. 74917 PDFDocument7 pagesG.R. No. 74917 PDFtrixieNo ratings yet

- Jai-Alai Corporation of The Philippines, Petitioner, vs. Bank of The Philippine Island, RespondentDocument126 pagesJai-Alai Corporation of The Philippines, Petitioner, vs. Bank of The Philippine Island, RespondentisangpantasNo ratings yet

- Bank of America vs. Philippine Racing Club, G.R. No. 150228, July 20, 2009Document13 pagesBank of America vs. Philippine Racing Club, G.R. No. 150228, July 20, 2009Chris ValenzuelaNo ratings yet

- Bank of America Vs Philippine Racing ClubDocument3 pagesBank of America Vs Philippine Racing ClubAbigail BozeNo ratings yet

- 10 HSBC V National Steel PDFDocument33 pages10 HSBC V National Steel PDFVincent Rey BernardoNo ratings yet

- HSBC vs. National SteelDocument29 pagesHSBC vs. National SteelAaron CariñoNo ratings yet

- Negotiable Instruments Case DigestDocument54 pagesNegotiable Instruments Case DigestHoward DinumlaNo ratings yet

- Bank of America vs. Associated Citizens BankDocument6 pagesBank of America vs. Associated Citizens BanknathNo ratings yet

- Jai-Alai Corp v. BPIDocument10 pagesJai-Alai Corp v. BPIGia DimayugaNo ratings yet

- Banco de Oro-V - Equitable - Assignment Vs NegotiationDocument11 pagesBanco de Oro-V - Equitable - Assignment Vs NegotiationStefanie RochaNo ratings yet

- Banco de Oro vs. Equitable Banking Corp. 157 SCRA 188, Jan. 20, 1988Document1 pageBanco de Oro vs. Equitable Banking Corp. 157 SCRA 188, Jan. 20, 1988David Lawrenz SamonteNo ratings yet

- New Pacific Timber & Supply Co., Inc vs. Seneris GR No. L-41764 December19, 1980. Concepcion JR., JDocument3 pagesNew Pacific Timber & Supply Co., Inc vs. Seneris GR No. L-41764 December19, 1980. Concepcion JR., JJadenNo ratings yet

- Bdo V Equitable BankingDocument2 pagesBdo V Equitable Bankingבנדר-עלי אימאם טינגאו בתולהNo ratings yet

- 5 ForgeryDocument57 pages5 ForgerySteven OrtizNo ratings yet

- 2 Tibajia Jr. v. Court of AppealsDocument4 pages2 Tibajia Jr. v. Court of AppealsRoseanne MateoNo ratings yet

- Stat Con DigestDocument7 pagesStat Con DigestAnonymous fL9dwyfekNo ratings yet

- 8Document80 pages8Hannah Khamil MirandaNo ratings yet

- Republic Bank Vs CADocument2 pagesRepublic Bank Vs CAboomonyouNo ratings yet

- 123709-1999-Cebu International Finance Corp. v. Court ofDocument10 pages123709-1999-Cebu International Finance Corp. v. Court ofKrizel BianoNo ratings yet

- California Supreme Court Petition: S173448 – Denied Without OpinionFrom EverandCalifornia Supreme Court Petition: S173448 – Denied Without OpinionRating: 4 out of 5 stars4/5 (1)

- Query of Atty. Karen M. Silverio-Buffe, Formewr Clerk of Court-Br. 81, Romblon, Romblon - On The Prohibition From Engaging in The Private Practice of LawDocument19 pagesQuery of Atty. Karen M. Silverio-Buffe, Formewr Clerk of Court-Br. 81, Romblon, Romblon - On The Prohibition From Engaging in The Private Practice of LawFD BalitaNo ratings yet

- People vs. de Luna, Et AlDocument10 pagesPeople vs. de Luna, Et AlFD BalitaNo ratings yet

- Juridical Capacity V Capacity To ActDocument1 pageJuridical Capacity V Capacity To ActFD BalitaNo ratings yet

- Figueroa vs. Barranco, Jr.Document6 pagesFigueroa vs. Barranco, Jr.FD BalitaNo ratings yet

- Noe-Lacsamana vs. BusmenteDocument7 pagesNoe-Lacsamana vs. BusmenteFD BalitaNo ratings yet

- 5.maquiling vs. Commission On Elections, 696 SCRA 420, G.R. No. 195649 April 16, 2013Document75 pages5.maquiling vs. Commission On Elections, 696 SCRA 420, G.R. No. 195649 April 16, 2013ismaelnogoyNo ratings yet

- Query of Atty. Karen M. Silverio-Buffe, Formewr Clerk of Court-Br. 81, Romblon, Romblon - On The Prohibition From Engaging in The Private Practice of LawDocument19 pagesQuery of Atty. Karen M. Silverio-Buffe, Formewr Clerk of Court-Br. 81, Romblon, Romblon - On The Prohibition From Engaging in The Private Practice of LawFD BalitaNo ratings yet

- Ong Chia vs. RepublicDocument10 pagesOng Chia vs. RepublicFD BalitaNo ratings yet

- Estate of Hilario M. Ruiz vs. Court of AppealsDocument12 pagesEstate of Hilario M. Ruiz vs. Court of AppealsFD BalitaNo ratings yet

- F. Republic vs. Sandiganbayan (Fourth Division)Document110 pagesF. Republic vs. Sandiganbayan (Fourth Division)FD BalitaNo ratings yet

- G. Ligtas vs. PeopleDocument40 pagesG. Ligtas vs. PeopleFD BalitaNo ratings yet

- B. People vs. KulaisDocument27 pagesB. People vs. KulaisFD BalitaNo ratings yet

- E. People vs. BaharanDocument20 pagesE. People vs. BaharanFD BalitaNo ratings yet

- G. Ligtas vs. PeopleDocument40 pagesG. Ligtas vs. PeopleFD BalitaNo ratings yet

- E. People vs. BaharanDocument20 pagesE. People vs. BaharanFD BalitaNo ratings yet

- Aranas v. MercadoDocument28 pagesAranas v. MercadoFD BalitaNo ratings yet

- Butiong vs. PlazoDocument30 pagesButiong vs. PlazoFD BalitaNo ratings yet

- Garcia-Quiazon V BelenDocument14 pagesGarcia-Quiazon V BelenMoniqueLeeNo ratings yet

- Sabidong vs. SolasDocument13 pagesSabidong vs. SolasArjay PuyotNo ratings yet

- Suntay III vs. Cojuangco-SuntayDocument23 pagesSuntay III vs. Cojuangco-SuntayFD BalitaNo ratings yet

- 1 Union Bank of The Philippines vs. SantibañezDocument15 pages1 Union Bank of The Philippines vs. Santibañezcool_peachNo ratings yet

- SCRA Pilapil v. Heirs of M. BrionesDocument27 pagesSCRA Pilapil v. Heirs of M. Brionesgoma21No ratings yet

- Lee vs. Regional Trial Court of Quezon City, Br. 85Document23 pagesLee vs. Regional Trial Court of Quezon City, Br. 85FD BalitaNo ratings yet

- 1 San Luis Vs San Luis GR 133743Document21 pages1 San Luis Vs San Luis GR 133743blessaraynesNo ratings yet

- Silverio, Sr. vs. Silverio, JRDocument15 pagesSilverio, Sr. vs. Silverio, JRFD BalitaNo ratings yet

- 3 Agtarap Vs Agtarap GR 177099Document22 pages3 Agtarap Vs Agtarap GR 177099Anonymous hbUJnBNo ratings yet

- 3 Agtarap Vs Agtarap GR 177099Document22 pages3 Agtarap Vs Agtarap GR 177099Anonymous hbUJnBNo ratings yet

- 1 San Luis Vs San Luis GR 133743Document21 pages1 San Luis Vs San Luis GR 133743blessaraynesNo ratings yet

- Silverio, Sr. vs. Silverio, JRDocument15 pagesSilverio, Sr. vs. Silverio, JRFD BalitaNo ratings yet

- Arellano Calendar 2nd Sem 2017-2018Document1 pageArellano Calendar 2nd Sem 2017-2018FD BalitaNo ratings yet

- History of BankDocument10 pagesHistory of BankSadaf KhanNo ratings yet

- Kalon Salon Talon Malon CelonDocument13 pagesKalon Salon Talon Malon Celonਰੁਪਿੰਦਰ ਸਿੰਘNo ratings yet

- Phil Trust Co. V Echaus Tan SiuaDocument1 pagePhil Trust Co. V Echaus Tan SiuaLouie RaotraotNo ratings yet

- Rudra P. Pradhan Vinod Gupta School of Management, Indian Institute of Technology Kharagpur, India Rudrap@vgsom - Iitkgp.ernet - inDocument8 pagesRudra P. Pradhan Vinod Gupta School of Management, Indian Institute of Technology Kharagpur, India Rudrap@vgsom - Iitkgp.ernet - inYashwant SoniNo ratings yet

- S Me Ex Written OnlyDocument356 pagesS Me Ex Written OnlyMuhibbullah Azfa ManikNo ratings yet

- Clay McCormack IndictmentDocument13 pagesClay McCormack IndictmentThe Jackson SunNo ratings yet

- First Planters Pawnshop, Inc. v. CIRDocument14 pagesFirst Planters Pawnshop, Inc. v. CIRKrisven Mae R. ObedoNo ratings yet

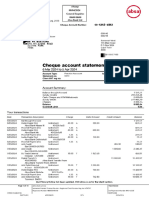

- Chase Bank Statement PDF Financial Technology Finance & Money ManagementDocument1 pageChase Bank Statement PDF Financial Technology Finance & Money Managementalexberry638464No ratings yet

- World Bank Support To Education Since 2001Document133 pagesWorld Bank Support To Education Since 2001Independent Evaluation GroupNo ratings yet

- Ific BankDocument7 pagesIfic BankMakid HasanNo ratings yet

- BFN 111 Week 7 - 8Document33 pagesBFN 111 Week 7 - 8CHIDINMA ONUORAHNo ratings yet

- NOC From Society For LAP (Share Certificate Issued) Revised-1Document1 pageNOC From Society For LAP (Share Certificate Issued) Revised-1avinash singhNo ratings yet

- MDocument19 pagesMJoannah SalamatNo ratings yet

- AI in Investment BankingDocument11 pagesAI in Investment BankingMadhura BanerjeeNo ratings yet

- Case Digest Compendium LABOR LAW IDocument16 pagesCase Digest Compendium LABOR LAW IRonn PetittNo ratings yet

- Understanding Bank Financial StatementsDocument49 pagesUnderstanding Bank Financial StatementsRajat MehtaNo ratings yet

- Capital and Risk Management Report 31 December 2011Document103 pagesCapital and Risk Management Report 31 December 2011Miki BasarovNo ratings yet

- SAP FICO-MaterialDocument137 pagesSAP FICO-MaterialPriyanka DNo ratings yet

- Macroeconomics Key GraphsDocument5 pagesMacroeconomics Key Graphsapi-243723152No ratings yet

- World Bank (IBRD & IDA)Document5 pagesWorld Bank (IBRD & IDA)prankyaquariusNo ratings yet

- Kyb 2023Document10 pagesKyb 2023RudraNo ratings yet

- RBI Directions On Foreign Banks and Acquisition and Amalgamation of BanksDocument8 pagesRBI Directions On Foreign Banks and Acquisition and Amalgamation of Banksvijayadarshini vNo ratings yet

- Manduleli Victor Bikitsha Nsualwkq ArchivedDocument10 pagesManduleli Victor Bikitsha Nsualwkq ArchivedManduleli BikitshaNo ratings yet

- Banking AwarenessDocument258 pagesBanking AwarenessDhanrajDarsenaNo ratings yet

- Savings Bank Accounts Rules & RegulationsDocument3 pagesSavings Bank Accounts Rules & Regulationsmanish sharmaNo ratings yet

- MR - Bhagyaraja Nagaraju Koppisetty: Page 1 of 2 M-87654321-1Document2 pagesMR - Bhagyaraja Nagaraju Koppisetty: Page 1 of 2 M-87654321-1Bhagyaraj KoppishettyNo ratings yet

- Rbi CircularDocument8 pagesRbi CircularadswerNo ratings yet