You might also like

- Following the Trend: Diversified Managed Futures TradingFrom EverandFollowing the Trend: Diversified Managed Futures TradingRating: 3.5 out of 5 stars3.5/5 (2)

- Steering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandSteering & Steering Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- What Is The Economic Outlook For OECD Countries?: An Interim AssessmentDocument17 pagesWhat Is The Economic Outlook For OECD Countries?: An Interim AssessmentJohn RotheNo ratings yet

- Economic Developments and Investment Environment in TurkeyDocument30 pagesEconomic Developments and Investment Environment in TurkeyPolat ArıNo ratings yet

- Esi 2019 05 enDocument21 pagesEsi 2019 05 enValter SilveiraNo ratings yet

- Deroose Dubrovnik Euro Crisis Are We Out of The WoodsDocument15 pagesDeroose Dubrovnik Euro Crisis Are We Out of The Woods1234567890albertoNo ratings yet

- Industry Outlook March2011Document4 pagesIndustry Outlook March2011iminvisibleNo ratings yet

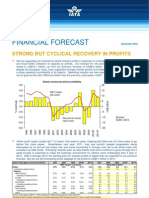

- Financial Forecast: Strong But Cyclical Recovery in ProfitsDocument4 pagesFinancial Forecast: Strong But Cyclical Recovery in ProfitsDaniel WongNo ratings yet

- The Australian Economy and Financial Markets: July 2019Document33 pagesThe Australian Economy and Financial Markets: July 2019Amita SinghNo ratings yet

- MSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Document3 pagesMSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Leophil RascoNo ratings yet

- Indian Economy Update-Feb 2009Document3 pagesIndian Economy Update-Feb 2009Mayank SharmaNo ratings yet

- Monthly Economic Bulletin: January 2011Document15 pagesMonthly Economic Bulletin: January 2011lrochekellyNo ratings yet

- Foreign Trade Developments in 1997 and 1998: ECB Monthly Bulletin - July 1999Document2 pagesForeign Trade Developments in 1997 and 1998: ECB Monthly Bulletin - July 1999aldhibahNo ratings yet

- Paul Kasriel: Great Depression, Just The FactsDocument7 pagesPaul Kasriel: Great Depression, Just The Factshblodget100% (3)

- Pepsi Quaterly Earnings 2020Document22 pagesPepsi Quaterly Earnings 2020Dulshan ErangaNo ratings yet

- Mosaic Global PerspectivesDocument14 pagesMosaic Global PerspectivesKevin A. Lenox, CFANo ratings yet

- Module 3: Poverty, Inequality and DevelopmentDocument52 pagesModule 3: Poverty, Inequality and DevelopmentChoco ButternutNo ratings yet

- Esi 2019 07 enDocument27 pagesEsi 2019 07 enValter SilveiraNo ratings yet

- Emerson 2012 PresentationDocument128 pagesEmerson 2012 PresentationCapgoods1No ratings yet

- KBSL - Consensus Budget ExpectationDocument44 pagesKBSL - Consensus Budget ExpectationRahulNo ratings yet

- Subtopic 2 - Moving AverageDocument21 pagesSubtopic 2 - Moving AverageKim VincereNo ratings yet

- Final Porfolio PaperDocument15 pagesFinal Porfolio PaperDeep DualNo ratings yet

- An SB DP VB CHB 2008 2009 2010 2011 2012: Trendul Erorilor Soldului BugetarDocument6 pagesAn SB DP VB CHB 2008 2009 2010 2011 2012: Trendul Erorilor Soldului BugetarSimona MoldoveanuNo ratings yet

- LBO - UncompletedDocument10 pagesLBO - UncompletedRachel TangNo ratings yet

- Oxford Economics Global Economic Outlook On The Cusp of ADocument10 pagesOxford Economics Global Economic Outlook On The Cusp of ABrainNo ratings yet

- T I S O: HE Berian Trategy BserverDocument15 pagesT I S O: HE Berian Trategy Bservercarloscfm9No ratings yet

- CH 15Document51 pagesCH 15jjupark2004No ratings yet

- The Balance of Payments: Speech Given by DR Martin WealeDocument14 pagesThe Balance of Payments: Speech Given by DR Martin WealeImamjafar SiddiqNo ratings yet

- The Israeli EconomyDocument39 pagesThe Israeli EconomyAqib JavedNo ratings yet

- CS23Document17 pagesCS234xeroaccNo ratings yet

- ForecastingDocument48 pagesForecastingBeatriz QuiambaoNo ratings yet

- Situation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesDocument34 pagesSituation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesuserabhishekNo ratings yet

- FMCG PDFDocument9 pagesFMCG PDFAmit GuptaNo ratings yet

- PNG Large Offshore Gas FieldDocument36 pagesPNG Large Offshore Gas FieldserahsalmonminakNo ratings yet

- Sampa Video Inc Case StudyDocument26 pagesSampa Video Inc Case StudyMegha BepariNo ratings yet

- Assignment 4Document69 pagesAssignment 4amy ackerNo ratings yet

- 50 AAPL Buyside PitchbookDocument22 pages50 AAPL Buyside PitchbookAkshay ShaikhNo ratings yet

- Certificate of Verification Vickers: Force CalibrationDocument4 pagesCertificate of Verification Vickers: Force CalibrationNader DallejNo ratings yet

- Confronting Economic SlowdownDocument26 pagesConfronting Economic Slowdownepra100% (1)

- Capital Structure of Malabar Gold and DiamondsDocument1 pageCapital Structure of Malabar Gold and Diamondsayesha khanumNo ratings yet

- Chap14 Stabilization PolicyDocument38 pagesChap14 Stabilization PolicyKharisma ArtaNo ratings yet

- Westpac Federal Budget ReportDocument8 pagesWestpac Federal Budget ReportTim MooreNo ratings yet

- Macroeconomic Analysis For DenmarkDocument8 pagesMacroeconomic Analysis For DenmarkBozinoskaSNo ratings yet

- CFP SDL UK Buffettology Fund: Factsheet - March 2020Document2 pagesCFP SDL UK Buffettology Fund: Factsheet - March 2020sky22blueNo ratings yet

- Airline Profitability ChallengeDocument19 pagesAirline Profitability ChallengebeowlNo ratings yet

- Dong Energy Q4 - 2011 - Presentation - March - 2012Document34 pagesDong Energy Q4 - 2011 - Presentation - March - 2012Justyna LipskaNo ratings yet

- BASF Chemicals ConferenceDocument49 pagesBASF Chemicals ConferenceValeria ShakarovaNo ratings yet

- India: Steady Private and Public Consumption GrowthDocument4 pagesIndia: Steady Private and Public Consumption GrowthRohan AtrawalkarNo ratings yet

- Presentation To Investors and Analysts: Outlook 2010e-2012p: December 2, 2010Document20 pagesPresentation To Investors and Analysts: Outlook 2010e-2012p: December 2, 2010KruasanNo ratings yet

- SME Idea ReOrangeDocument11 pagesSME Idea ReOrangeabeershujaat22No ratings yet

- Problem 5 (15 Points) : A A A ADocument5 pagesProblem 5 (15 Points) : A A A AOrangeNo ratings yet

- Havells Initiating Coverage 27 Apr 2011Document23 pagesHavells Initiating Coverage 27 Apr 2011ananth999No ratings yet

- Indian Capital Goods IndustryDocument19 pagesIndian Capital Goods IndustryanilkunjuNo ratings yet

- High Probability Trading Slide - Kathy Lien (Part 1)Document57 pagesHigh Probability Trading Slide - Kathy Lien (Part 1)IsabelNogales100% (2)

- Chapter 7 Prospective Analysis: Valuation Theory and ConceptsDocument7 pagesChapter 7 Prospective Analysis: Valuation Theory and ConceptsWalm KetyNo ratings yet

- MS - Counterpoint Global Insights ROIC and Intangible AssetsDocument13 pagesMS - Counterpoint Global Insights ROIC and Intangible AssetsLuanNo ratings yet

- MindChamps - Annual ReportDocument15 pagesMindChamps - Annual ReportChristian?97No ratings yet

- Butterfly Trades in FuturesDocument9 pagesButterfly Trades in Futuresjalajsingh1987No ratings yet

- Wheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandWheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Essay Parliament Peet Menon Dec10-179Document10 pagesEssay Parliament Peet Menon Dec10-1791234567890albertoNo ratings yet

- Quaderni e 14 External1 2Document76 pagesQuaderni e 14 External1 21234567890albertoNo ratings yet

- European Convention On Human RightDocument34 pagesEuropean Convention On Human Right1234567890albertoNo ratings yet

- Eprs Bri (2016) 577971 enDocument8 pagesEprs Bri (2016) 577971 en1234567890albertoNo ratings yet

- UK Withdrawal From The European Union: In-Depth AnalysisDocument40 pagesUK Withdrawal From The European Union: In-Depth Analysis1234567890albertoNo ratings yet

- EN - EP Brochure Citizen VoicesDocument25 pagesEN - EP Brochure Citizen Voices1234567890albertoNo ratings yet

- Deadlines September STR 2017.07.12 enDocument2 pagesDeadlines September STR 2017.07.12 en1234567890albertoNo ratings yet

- White Paper On The Future of Europe en PDFDocument32 pagesWhite Paper On The Future of Europe en PDFȘerban AnghelNo ratings yet

- Deroose Bucharestlaunch2016crfinal PDFDocument15 pagesDeroose Bucharestlaunch2016crfinal PDF1234567890albertoNo ratings yet

- Working For You enDocument60 pagesWorking For You en1234567890albertoNo ratings yet

- EC-Guide E&RADocument100 pagesEC-Guide E&RA1234567890albertoNo ratings yet

- European ParliamentDocument8 pagesEuropean Parliament1234567890albertoNo ratings yet

- The European Parliament: Organisation and Operation: Legal BasisDocument4 pagesThe European Parliament: Organisation and Operation: Legal Basis1234567890albertoNo ratings yet

- Report TurkeyDocument102 pagesReport TurkeyBogdan AlecuNo ratings yet

- Lobby Meetings European CommissionDocument24 pagesLobby Meetings European Commission1234567890albertoNo ratings yet

- 2017 European Semester Country Report Belgium enDocument73 pages2017 European Semester Country Report Belgium en1234567890albertoNo ratings yet

- Charter en PDFDocument206 pagesCharter en PDF1234567890albertoNo ratings yet

- EUWhoiswho 10 enDocument180 pagesEUWhoiswho 10 en1234567890albertoNo ratings yet

- Use-Emblem en PDFDocument8 pagesUse-Emblem en PDF1234567890albertoNo ratings yet

- Media 36177 enDocument92 pagesMedia 36177 en1234567890albertoNo ratings yet

- Deroose Sto Two Speed Europe BruegelDocument24 pagesDeroose Sto Two Speed Europe Bruegel1234567890albertoNo ratings yet

- Partners-Guidelines en 1Document4 pagesPartners-Guidelines en 11234567890albertoNo ratings yet

- 2016 EU Referendum ReportDocument133 pages2016 EU Referendum Report1234567890albertoNo ratings yet

- Essential Principles Citizens Rights enDocument4 pagesEssential Principles Citizens Rights en1234567890albertoNo ratings yet

- Media 36177 enDocument92 pagesMedia 36177 en1234567890albertoNo ratings yet

- Reflection Paper Defence enDocument24 pagesReflection Paper Defence en1234567890albertoNo ratings yet

- Deroose Dubrovnik Convergence EaDocument20 pagesDeroose Dubrovnik Convergence Ea1234567890albertoNo ratings yet

- 2nd Report State Energy Union enDocument15 pages2nd Report State Energy Union en1234567890albertoNo ratings yet

- Financial Transaction Taxes in The European Union: Taxation PapersDocument36 pagesFinancial Transaction Taxes in The European Union: Taxation Papers1234567890albertoNo ratings yet

- Financial Transaction Taxes in The European Union: Taxation PapersDocument36 pagesFinancial Transaction Taxes in The European Union: Taxation Papers1234567890albertoNo ratings yet

- General Nature and Definition of Human RightsDocument11 pagesGeneral Nature and Definition of Human RightsDaryl Canillas PagaduanNo ratings yet

- Midterm Exam GEC 18 EthicsDocument2 pagesMidterm Exam GEC 18 Ethicslxap2023-6821-74342No ratings yet

- SK-Brgy-Official-Directory-Template-LA PaZDocument9 pagesSK-Brgy-Official-Directory-Template-LA PaZsteven orillanedaNo ratings yet

- A Historic Battle Was Fought On The Plains of Panipat 261 Years Ago TodayDocument2 pagesA Historic Battle Was Fought On The Plains of Panipat 261 Years Ago TodayAmay GiteNo ratings yet

- Definition of DemocracyDocument5 pagesDefinition of DemocracyaldwinNo ratings yet

- Confidential Non-Disclosure AgreementDocument1 pageConfidential Non-Disclosure AgreementTammie WalkerNo ratings yet

- SILC Working DraftDocument21 pagesSILC Working DraftBar & BenchNo ratings yet

- Lokin v. ComelecDocument4 pagesLokin v. ComelecKreezelNo ratings yet

- Republic of The Philippines Department of Justice ManilaDocument10 pagesRepublic of The Philippines Department of Justice ManilaAllen SoNo ratings yet

- Multistakeholder CooperationDocument3 pagesMultistakeholder CooperationInternetSocietyNo ratings yet

- Grass Curtain - Co-Edited by Enock Mading de GarangDocument5 pagesGrass Curtain - Co-Edited by Enock Mading de GarangJohn Majok Manyok Thuch0% (1)

- Var Case StudyDocument12 pagesVar Case Studyvarun v sNo ratings yet

- Proclamation: Special Observances: Caribbean-American Heritage Month (Proc. 8153)Document2 pagesProclamation: Special Observances: Caribbean-American Heritage Month (Proc. 8153)Justia.comNo ratings yet

- HIST 101 All SlidesDocument79 pagesHIST 101 All SlidesSomaia ShaabanNo ratings yet

- FrontpageAfrica Interviews TRANSCO CLSG GM, Sept 28Document18 pagesFrontpageAfrica Interviews TRANSCO CLSG GM, Sept 28TRANSCO CLSG100% (1)

- David Lloyd - Settler Colonialism and The State of ExceptionDocument22 pagesDavid Lloyd - Settler Colonialism and The State of ExceptionAfthab EllathNo ratings yet

- KTPP Amendment Act 2020Document4 pagesKTPP Amendment Act 2020SjNo ratings yet

- Agrarian ReformDocument36 pagesAgrarian ReformSarah Buhulon83% (6)

- Twinning Fiche - NASRI - AL 20 IPA OT 01 22 TWL - 11.10.2022-1Document30 pagesTwinning Fiche - NASRI - AL 20 IPA OT 01 22 TWL - 11.10.2022-1vaheNo ratings yet

- Implan 2023 FPMDocument11 pagesImplan 2023 FPMmench_barredo100% (1)

- Unclassified Released in FullDocument24 pagesUnclassified Released in FullglennallynNo ratings yet

- Dr. Thein Lwin Language Article (English) 15thoct11Document17 pagesDr. Thein Lwin Language Article (English) 15thoct11Bayu Smada50% (2)

- Bash The Rich: David Cameron Exposed, Multi-Cultural Myths Royal Wedding Sick Bag Summer Sizzler Phooargh!Document15 pagesBash The Rich: David Cameron Exposed, Multi-Cultural Myths Royal Wedding Sick Bag Summer Sizzler Phooargh!teaguetoddNo ratings yet

- Grade Math TleDocument256 pagesGrade Math TleSunshine GarsonNo ratings yet

- Women Empowerment in India: With Reference To Current PoliciesDocument20 pagesWomen Empowerment in India: With Reference To Current PoliciesArindam Neral100% (2)

- The War Powers Act of 1973Document7 pagesThe War Powers Act of 1973ruslan3338458No ratings yet

- With Liberty and Dividends For All: How To Save Our Middle Class When Jobs Don't Pay EnoughDocument6 pagesWith Liberty and Dividends For All: How To Save Our Middle Class When Jobs Don't Pay EnoughDwight MurpheyNo ratings yet

- Sahil Group DDocument2 pagesSahil Group DAbhishek SardhanaNo ratings yet

- CH 31 L1 - Guided ReadingDocument2 pagesCH 31 L1 - Guided ReadingEdward FosterNo ratings yet

- T8 B6 FAA HQ Bart Merkley FDR - Handwritten Interview Notes and Email From Miles Kara Re Interview Merkley and TaafeDocument8 pagesT8 B6 FAA HQ Bart Merkley FDR - Handwritten Interview Notes and Email From Miles Kara Re Interview Merkley and Taafe9/11 Document ArchiveNo ratings yet