You might also like

- Practice Quiz 5 Module 3 Financial MarketsDocument5 pagesPractice Quiz 5 Module 3 Financial MarketsMuhire KevineNo ratings yet

- Financial Model of ACCDocument13 pagesFinancial Model of ACCYash AhujaNo ratings yet

- IGC. Grain Market ReportDocument9 pagesIGC. Grain Market ReportHoa Nguyen ThaiNo ratings yet

- Market: International Grains CouncilDocument8 pagesMarket: International Grains CounciljinaeNo ratings yet

- Connecting Farmers To Markets FPO Update - July 2020Document13 pagesConnecting Farmers To Markets FPO Update - July 2020nirajmyeduNo ratings yet

- Connecting Farmers To Markets FPO Update - March 2021Document13 pagesConnecting Farmers To Markets FPO Update - March 2021nirajmyeduNo ratings yet

- 2019 Q3 Financial - Presentation - Qiii - 2018-19Document9 pages2019 Q3 Financial - Presentation - Qiii - 2018-19Anand SNo ratings yet

- Cambodia: Date: GAIN Report NumberDocument15 pagesCambodia: Date: GAIN Report NumberFaran MoonisNo ratings yet

- Progress With Sustainability For Gen-Next: JK Cement Limited JK Cement LimitedDocument59 pagesProgress With Sustainability For Gen-Next: JK Cement Limited JK Cement Limitedsunfront kapilNo ratings yet

- Strip Chart of Power Line Crossing (Maintained by Rajesh)Document3 pagesStrip Chart of Power Line Crossing (Maintained by Rajesh)Er Rajesh KumarNo ratings yet

- Tomato Paste and SauceDocument14 pagesTomato Paste and Saucekassahun meseleNo ratings yet

- Practica 1 JL ChaucaDocument9 pagesPractica 1 JL ChaucaJoseLuisChaucaNo ratings yet

- 2020 Estimate Relative Row Crop Costs Net ReturnsDocument32 pages2020 Estimate Relative Row Crop Costs Net ReturnsGeros dienosNo ratings yet

- Cement Industry: Sector UpdateDocument8 pagesCement Industry: Sector UpdateAbdullah SohailNo ratings yet

- TSMPL Tyre Performance Presentation On Oct-19 PDFDocument21 pagesTSMPL Tyre Performance Presentation On Oct-19 PDFjitendra kumarNo ratings yet

- National Mineral ScenarioDocument7 pagesNational Mineral ScenarionagarajuNo ratings yet

- PinsDocument25 pagesPinsEliasNo ratings yet

- Telecom Market of Various Countries 1Document17 pagesTelecom Market of Various Countries 1PriyadharshiniNo ratings yet

- Unaudited Financialresults 30092019Document12 pagesUnaudited Financialresults 30092019SuhasNo ratings yet

- Schedules A B C D H Nalagampalli To KNT Border PDFDocument46 pagesSchedules A B C D H Nalagampalli To KNT Border PDFsankarrao333No ratings yet

- Cotton Profile May 2019Document10 pagesCotton Profile May 2019Jahanvi KhannaNo ratings yet

- M1 Part 1 Globalization and MultinationalDocument7 pagesM1 Part 1 Globalization and MultinationalAnkit JajalNo ratings yet

- Shock Absorber (Hydraulic) FinalDocument27 pagesShock Absorber (Hydraulic) FinalRobel KefelewNo ratings yet

- Foam Board RM ReconciliationDocument1 pageFoam Board RM Reconciliationamarveer477No ratings yet

- MISC Monthly April 2018Document6 pagesMISC Monthly April 2018Samu MenendezNo ratings yet

- Maize StarchDocument28 pagesMaize Starchbirukbrook2No ratings yet

- GM - Review For SWS GZBDocument5 pagesGM - Review For SWS GZBVikasNo ratings yet

- Stock Decoder - Skipper Ltd-202402261647087215913Document1 pageStock Decoder - Skipper Ltd-202402261647087215913patelankurrhpmNo ratings yet

- Carbon BlackDocument15 pagesCarbon BlacksamsonNo ratings yet

- Indias Warehousing Sector Review 2018Document6 pagesIndias Warehousing Sector Review 2018Aritra DasNo ratings yet

- Connecting Farmers To Markets FPO Update - March 2020Document13 pagesConnecting Farmers To Markets FPO Update - March 2020nirajmyeduNo ratings yet

- Rundown Hot Stamping Maret April Mei 2022Document2 pagesRundown Hot Stamping Maret April Mei 2022Riky MPNo ratings yet

- Requirements of Raw Materials For Steel Industry Reflections On MMDR Bill 2011Document17 pagesRequirements of Raw Materials For Steel Industry Reflections On MMDR Bill 2011donhan91No ratings yet

- Applied Maths ProjectDocument10 pagesApplied Maths ProjectDarsh KansalNo ratings yet

- Cotton Feb 2018Document10 pagesCotton Feb 2018Vernit BindalNo ratings yet

- Investor Presentation Q316 FinalDocument23 pagesInvestor Presentation Q316 FinalClary DsilvaNo ratings yet

- Operational Updates As of December 2017: Komatsu YTD Sales Volume (In Unit)Document2 pagesOperational Updates As of December 2017: Komatsu YTD Sales Volume (In Unit)siput_lembekNo ratings yet

- Rice Profile March,, 2018Document9 pagesRice Profile March,, 2018Sudeep SantraNo ratings yet

- Organic FertilizerDocument25 pagesOrganic FertilizerFirezegiNo ratings yet

- Sewing Machine AssemblyDocument26 pagesSewing Machine AssemblyRobel KefelewNo ratings yet

- Challenges of LNG & Economics of Its Use: Suresh Mathur MayDocument19 pagesChallenges of LNG & Economics of Its Use: Suresh Mathur Mayjmari DymongNo ratings yet

- Saw BladesDocument25 pagesSaw BladesEliasNo ratings yet

- Uflex Audited Consolidated Results 31st March 2019Document4 pagesUflex Audited Consolidated Results 31st March 2019markelonnNo ratings yet

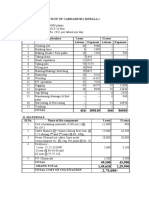

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDJinshad ChakkingalNo ratings yet

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDArafath MuhammedNo ratings yet

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDArafath MuhammedNo ratings yet

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDPavan Kumar Gundu RaoNo ratings yet

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDArafath MuhammedNo ratings yet

- Cost of Cultivation of Cardamom (Kerala) : ND RDDocument4 pagesCost of Cultivation of Cardamom (Kerala) : ND RDVsc RajNo ratings yet

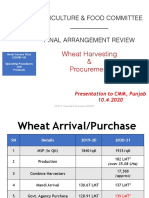

- Wheat Procurement Rabi2020Document20 pagesWheat Procurement Rabi2020RifacNo ratings yet

- Project Blue Nile - Take Home ONe TEmplate PDFDocument2 pagesProject Blue Nile - Take Home ONe TEmplate PDFYogesh PanwarNo ratings yet

- Investor Presentation 2019 PDFDocument34 pagesInvestor Presentation 2019 PDFPranabKumarGoswamiNo ratings yet

- Avilability & Pricing of GasDocument26 pagesAvilability & Pricing of GasOmkar PantNo ratings yet

- 1Q17 WebcastDocument15 pages1Q17 WebcastUsiminas_RINo ratings yet

- CIECH Financial Results Q1 23Document41 pagesCIECH Financial Results Q1 23Huifeng LeeNo ratings yet

- B A Aurangabad Girish Singh Bisht Vikash Kumar Raghvendra Singh BIHDocument4 pagesB A Aurangabad Girish Singh Bisht Vikash Kumar Raghvendra Singh BIHVikash KumarNo ratings yet

- Spark PlugsDocument24 pagesSpark PlugsRobel KefelewNo ratings yet

- 09.00 Hiroyuki Egawa Taiheiyo Cement CorporationDocument24 pages09.00 Hiroyuki Egawa Taiheiyo Cement CorporationParamananda SinghNo ratings yet

- Century Enka Limited: BUY Industry: TextilesDocument5 pagesCentury Enka Limited: BUY Industry: TextilesChanduSaiHemanthNo ratings yet

- Cement IndustryDocument6 pagesCement Industrye6l3nn100% (1)

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- The CQF Careers Guide 2023Document45 pagesThe CQF Careers Guide 2023ashaik1No ratings yet

- Family Office InsightsDocument27 pagesFamily Office Insightsashaik1No ratings yet

- Igc Grain Market Indicators: WheatDocument3 pagesIgc Grain Market Indicators: Wheatashaik1No ratings yet

- English Only International Grains Council Ocean Freight Rates For Grains On Major Selected RoutesDocument2 pagesEnglish Only International Grains Council Ocean Freight Rates For Grains On Major Selected Routesashaik1No ratings yet

- Gmi09 27Document2 pagesGmi09 27ashaik1No ratings yet

- Gmi12 27Document3 pagesGmi12 27ashaik1No ratings yet

- Orca Share Media1579045614947Document4 pagesOrca Share Media1579045614947Teresa Marie Yap CorderoNo ratings yet

- A Letter From Sir William R. Hamilton To John T. Graves, EsqDocument7 pagesA Letter From Sir William R. Hamilton To John T. Graves, EsqJoshuaHaimMamouNo ratings yet

- Diec Russias Demographic Policy After 2000 2022Document29 pagesDiec Russias Demographic Policy After 2000 2022dawdowskuNo ratings yet

- Chapter 9 &10 - Gene ExpressionDocument4 pagesChapter 9 &10 - Gene ExpressionMahmOod GhNo ratings yet

- Tradingfxhub Com Blog How To Trade Supply and Demand Using CciDocument12 pagesTradingfxhub Com Blog How To Trade Supply and Demand Using CciKrunal ParabNo ratings yet

- VC++ Splitter Windows & DLLDocument41 pagesVC++ Splitter Windows & DLLsbalajisathyaNo ratings yet

- Evolut Pro Mini Product Brochure PDFDocument8 pagesEvolut Pro Mini Product Brochure PDFBalázs PalcsikNo ratings yet

- Turb Mod NotesDocument32 pagesTurb Mod NotessamandondonNo ratings yet

- The Rime of The Ancient Mariner (Text of 1834) by - Poetry FoundationDocument19 pagesThe Rime of The Ancient Mariner (Text of 1834) by - Poetry FoundationNeil RudraNo ratings yet

- SMA Releases Online Version of Sunny Design For PV System ConfigurationDocument3 pagesSMA Releases Online Version of Sunny Design For PV System ConfigurationlakliraNo ratings yet

- Affin Bank V Zulkifli - 2006Document15 pagesAffin Bank V Zulkifli - 2006sheika_11No ratings yet

- The Foundations of Ekistics PDFDocument15 pagesThe Foundations of Ekistics PDFMd Shahroz AlamNo ratings yet

- Pyridine Reactions: University College of Pharmaceutialsciences K.U. CampusDocument16 pagesPyridine Reactions: University College of Pharmaceutialsciences K.U. CampusVã RãNo ratings yet

- An/Trc - 170 TrainingDocument264 pagesAn/Trc - 170 Trainingkapenrem2003No ratings yet

- 2 - (Accounting For Foreign Currency Transaction)Document25 pages2 - (Accounting For Foreign Currency Transaction)Stephiel SumpNo ratings yet

- Etsi en 300 019-2-2 V2.4.1 (2017-11)Document22 pagesEtsi en 300 019-2-2 V2.4.1 (2017-11)liuyx866No ratings yet

- Two Steps Individualized ACTH Therapy For West SyndromeDocument1 pageTwo Steps Individualized ACTH Therapy For West SyndromeDrAmjad MirzanaikNo ratings yet

- MCS 150 Page 1Document2 pagesMCS 150 Page 1Galina NovahovaNo ratings yet

- Coffee in 2018 The New Era of Coffee EverywhereDocument55 pagesCoffee in 2018 The New Era of Coffee Everywherec3memoNo ratings yet

- Reinforcing Steel and AccessoriesDocument4 pagesReinforcing Steel and AccessoriesTheodore TheodoropoulosNo ratings yet

- Naresh Kadyan: Voice For Animals in Rajya Sabha - Abhishek KadyanDocument28 pagesNaresh Kadyan: Voice For Animals in Rajya Sabha - Abhishek KadyanNaresh KadyanNo ratings yet

- Past Paper1Document8 pagesPast Paper1Ne''ma Khalid Said Al HinaiNo ratings yet

- Excavations OSHA 2226Document44 pagesExcavations OSHA 2226Al DubNo ratings yet

- Werewolf The Apocalypse 20th Anniversary Character SheetDocument6 pagesWerewolf The Apocalypse 20th Anniversary Character SheetKynanNo ratings yet

- Gurufocus Manual of Stocks: 20 Most Popular Gurus' StocksDocument22 pagesGurufocus Manual of Stocks: 20 Most Popular Gurus' StocksCardoso PenhaNo ratings yet

- Plessy V Ferguson DBQDocument4 pagesPlessy V Ferguson DBQapi-300429241No ratings yet

- The Municipality of Santa BarbaraDocument10 pagesThe Municipality of Santa BarbaraEmel Grace Majaducon TevesNo ratings yet

- Phase/State Transitions of Confectionery Sweeteners: Thermodynamic and Kinetic AspectsDocument16 pagesPhase/State Transitions of Confectionery Sweeteners: Thermodynamic and Kinetic AspectsAlicia MartinezNo ratings yet

- FINS1612 Capital Markets and Institutions S12016Document15 pagesFINS1612 Capital Markets and Institutions S12016fakableNo ratings yet