You might also like

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- FA AnalysisDocument22 pagesFA Analysisharendra choudharyNo ratings yet

- Project Report (ABBOTT)Document29 pagesProject Report (ABBOTT)MohsIn IQbalNo ratings yet

- Credit Memo For Gas Authority of IndiaDocument15 pagesCredit Memo For Gas Authority of IndiaKrina ShahNo ratings yet

- ITC Financial AnalysisDocument21 pagesITC Financial AnalysisDeepak ChandekarNo ratings yet

- Due Diligence Report AnoopDocument12 pagesDue Diligence Report AnoopAnoop KumarNo ratings yet

- Common Size Analysis CIPLA & Dr. Reddy's LabDocument11 pagesCommon Size Analysis CIPLA & Dr. Reddy's Labhahire0% (1)

- Equity Research Is The Study of A Business and ItsDocument32 pagesEquity Research Is The Study of A Business and ItsSanju JageNo ratings yet

- Unitedhealth Care Income Statement & Balance Sheet & PE RatioDocument8 pagesUnitedhealth Care Income Statement & Balance Sheet & PE RatioEhab elhashmyNo ratings yet

- Vertical Analysis of Balance SheetDocument4 pagesVertical Analysis of Balance SheetMinionsNo ratings yet

- Fra Wipro AnalysisDocument17 pagesFra Wipro AnalysisApoorv SrivastavaNo ratings yet

- FA of ItcDocument18 pagesFA of ItcSriya GuptaNo ratings yet

- ACCG305-Auditing and Assurance Services Case Study AssignmentDocument8 pagesACCG305-Auditing and Assurance Services Case Study AssignmentZee ZaidiNo ratings yet

- AFS Ch-11Document26 pagesAFS Ch-11saqlain aliNo ratings yet

- Financial-Analysis-Procter&Gamble-vs-Reckitt BenckiserDocument5 pagesFinancial-Analysis-Procter&Gamble-vs-Reckitt BenckiserPatOcampoNo ratings yet

- MentormindDocument23 pagesMentormindSonia GraceNo ratings yet

- Profit and Loss Account: Balance SheetDocument6 pagesProfit and Loss Account: Balance SheetJunaid SaleemNo ratings yet

- Group 1 - FRA Assignment - HUL - Term1Document8 pagesGroup 1 - FRA Assignment - HUL - Term1satyam pandeyNo ratings yet

- Financial Statement Analysis FIN3111Document9 pagesFinancial Statement Analysis FIN3111Zile MoazzamNo ratings yet

- Financial & Managerial Accounting Decision Makers: Analyzing and Interpreting Financial StatementsDocument65 pagesFinancial & Managerial Accounting Decision Makers: Analyzing and Interpreting Financial StatementsEric GuoNo ratings yet

- Jollibee Foods Corp - Comparative AnalysisDocument15 pagesJollibee Foods Corp - Comparative AnalysisJ. Kylene C. Lumusad100% (1)

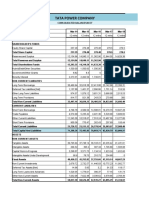

- Tata Power CoDocument28 pagesTata Power CoAnujaNo ratings yet

- Income Statement Company A Percent Company B Percent RevenueDocument4 pagesIncome Statement Company A Percent Company B Percent RevenueLina Levvenia RatanamNo ratings yet

- Rohit Pandey-15E-064 - FSA - EnduranceDocument6 pagesRohit Pandey-15E-064 - FSA - EnduranceROHIT PANDEYNo ratings yet

- Bacolod, Adinrane P. Bsba Finman IiiDocument25 pagesBacolod, Adinrane P. Bsba Finman IiichenlyNo ratings yet

- Project Solution 1 - SampleDocument11 pagesProject Solution 1 - SampleNguyễn Diệu LinhNo ratings yet

- VERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Document8 pagesVERTICAL ANALYSIS OF INCOME STATEMENT of Toyota 2022-2021Touqeer HussainNo ratings yet

- Financial Planning & ForecastingDocument23 pagesFinancial Planning & ForecastingRanjan SingNo ratings yet

- Financial Statement Analysis of TataDocument32 pagesFinancial Statement Analysis of TataVISHNU SATHEESHNo ratings yet

- ValuationDocument18 pagesValuationsanket patilNo ratings yet

- Lincoln Electric Itw - Cost Management ProjectDocument7 pagesLincoln Electric Itw - Cost Management Projectapi-451188446No ratings yet

- Financial Statement Analysis On BEXIMCO and SQUAREDocument33 pagesFinancial Statement Analysis On BEXIMCO and SQUAREYolowii XanaNo ratings yet

- Horizontal AnalysisDocument6 pagesHorizontal AnalysisjohhanaNo ratings yet

- Assignment For Final Assesment: Submitted By: Subitted To: Subject: Course Name: Course Code: DateDocument13 pagesAssignment For Final Assesment: Submitted By: Subitted To: Subject: Course Name: Course Code: DateNeel ManushNo ratings yet

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingDocument8 pagesNMIMS Global Access School For Continuing Education (NGA-SCE) Course: Financial AccountingMinaal KutriyaarNo ratings yet

- Financial Analysis of COKEDocument9 pagesFinancial Analysis of COKEUsmanNo ratings yet

- Examining Financial StatementsDocument6 pagesExamining Financial StatementsSandy K. AtchisonNo ratings yet

- Group 2 SBR 2 FRMDocument11 pagesGroup 2 SBR 2 FRMPooja JainNo ratings yet

- Group AssignmentDocument6 pagesGroup Assignmentmai bannNo ratings yet

- HDFC Bank Ratio AnalysisDocument14 pagesHDFC Bank Ratio Analysissunnykumar.m2325No ratings yet

- MBA104 - Almario - Parco - Online Problem Solving 3 Online Quiz Exam 2Document13 pagesMBA104 - Almario - Parco - Online Problem Solving 3 Online Quiz Exam 2nicolaus copernicusNo ratings yet

- Iqra University North Nazimabad Campus: Financial Reports and AnalysisDocument15 pagesIqra University North Nazimabad Campus: Financial Reports and Analysisharmain khalilNo ratings yet

- 1.inroduction: Working Capital Management Refers To A Company's ManagerialDocument7 pages1.inroduction: Working Capital Management Refers To A Company's Managerialmaa digitalxeroxNo ratings yet

- Institute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)Document9 pagesInstitute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)hitesh rathodNo ratings yet

- Final Group Assignment - Group 5Document29 pagesFinal Group Assignment - Group 5Nguyen Quy Tran TranNo ratings yet

- Hul Ratio AnalysisDocument14 pagesHul Ratio Analysisvviek100% (1)

- Lecture Common Size and Comparative AnalysisDocument28 pagesLecture Common Size and Comparative AnalysissumitsgagreelNo ratings yet

- A Study On Financial Analysis of Wipro LTDDocument11 pagesA Study On Financial Analysis of Wipro LTDKarthikNo ratings yet

- A. Objective or Purpose of The StudyDocument55 pagesA. Objective or Purpose of The Studymgp 1601No ratings yet

- IZw Sa RXN QZD Y1593510108564Document8 pagesIZw Sa RXN QZD Y1593510108564Dev ShahNo ratings yet

- Sapm Stock AnalysisDocument23 pagesSapm Stock AnalysisAthira K. ANo ratings yet

- Running Head: Financial Statement Analysis of Samsung 1Document19 pagesRunning Head: Financial Statement Analysis of Samsung 1Sangita GautamNo ratings yet

- Financial Overview5Document8 pagesFinancial Overview5Nishad Al Hasan SagorNo ratings yet

- Bajaj Finserv LTD: General OverviewDocument9 pagesBajaj Finserv LTD: General Overviewakanksha morghadeNo ratings yet

- Reneta LimitedDocument66 pagesReneta LimitedGold LeafNo ratings yet

- Financial Analysis Report: Luiz Mottin - Marco Albuquerque - Lara KleeneDocument20 pagesFinancial Analysis Report: Luiz Mottin - Marco Albuquerque - Lara KleeneLuiz Gustavo Mottin100% (1)

- REF: Year-End 31 December 2018 Financial Performance and Financial Position Analysis of Zambia BreweriesDocument8 pagesREF: Year-End 31 December 2018 Financial Performance and Financial Position Analysis of Zambia BreweriesMubanga kanyantaNo ratings yet

- Financial Analysis of Adani EnterprisesDocument11 pagesFinancial Analysis of Adani EnterprisesChinmay Prusty50% (2)

- WA2Document3 pagesWA2Ahmed HassaanNo ratings yet

- Scor-Estore Dot Com Business: All Numbers Below inDocument1 pageScor-Estore Dot Com Business: All Numbers Below inPriya RadhakrishnanNo ratings yet

- WAC Apollo Hospitals JahjaDocument2 pagesWAC Apollo Hospitals JahjaPriya RadhakrishnanNo ratings yet

- Assignment 4Document2 pagesAssignment 4Priya RadhakrishnanNo ratings yet

- MANAC Mid Term Answer Key 2014 PDFDocument16 pagesMANAC Mid Term Answer Key 2014 PDFPriya RadhakrishnanNo ratings yet

- ANOVA Example: Dreamland Bakery, A Famous Bakery Company in Kozhikode, Supplies Bakery Products To ManyDocument1 pageANOVA Example: Dreamland Bakery, A Famous Bakery Company in Kozhikode, Supplies Bakery Products To ManyPriya RadhakrishnanNo ratings yet

- Epstein Barr Virus (EBV) PDFDocument33 pagesEpstein Barr Virus (EBV) PDFahmad mohammadNo ratings yet

- Antihypertensive Mcqs ExplainedDocument4 pagesAntihypertensive Mcqs ExplainedHawi BefekaduNo ratings yet

- Rdramirez Aota 2018 Poster For PortfolioDocument1 pageRdramirez Aota 2018 Poster For Portfolioapi-437843157No ratings yet

- 60 Substance Abuse Group Therapy ActivitiesDocument7 pages60 Substance Abuse Group Therapy ActivitiesHanes Labajos100% (1)

- WRAS MarinasDocument4 pagesWRAS MarinasAdam ReesNo ratings yet

- Meditation ScriptDocument9 pagesMeditation Scriptapi-361293242100% (1)

- Union Civil Protection Mechanism: More Effective, Efficient and Coherent Disaster ManagementDocument23 pagesUnion Civil Protection Mechanism: More Effective, Efficient and Coherent Disaster ManagementCătălin Marian IvanNo ratings yet

- Viroguard Sanitizer SDS-WatermartDocument7 pagesViroguard Sanitizer SDS-WatermartIshara VithanaNo ratings yet

- Clothier-Wright2018 Article DysfunctionalVoidingTheImportaDocument14 pagesClothier-Wright2018 Article DysfunctionalVoidingTheImportaMarcello PinheiroNo ratings yet

- Child Welfare Trauma Training Participant GuideDocument104 pagesChild Welfare Trauma Training Participant GuideAllison PalmisanoNo ratings yet

- NURS FPX 6030 Assessment 6 Final Project SubmissionDocument11 pagesNURS FPX 6030 Assessment 6 Final Project Submissionzadem5266No ratings yet

- Chapter 6 QuestionsDocument2 pagesChapter 6 QuestionsGabo DanteNo ratings yet

- Combat StressDocument94 pagesCombat StressClaudia Maria Ivan100% (1)

- Tcid 50Document10 pagesTcid 50Rohan Walking Tall100% (1)

- VE4 Sem 1 Student Packet (25 July)Document187 pagesVE4 Sem 1 Student Packet (25 July)Dwayne June GetiganNo ratings yet

- Literature Review Kangaroo Mother CareDocument7 pagesLiterature Review Kangaroo Mother CareafdtuwxrbNo ratings yet

- Ganglions Clinical Presentation - History and Physical ExaminationDocument3 pagesGanglions Clinical Presentation - History and Physical ExaminationAnonymous vOJH2hLMh6No ratings yet

- Diabetic Foot Ulcer Assessment and Management Algorithm - 0Document11 pagesDiabetic Foot Ulcer Assessment and Management Algorithm - 0Herlan BelaNo ratings yet

- Effect of A Program of Physical Activity Motivated by Lipid Parameters of Patients With Obesity and or Overweight PDFDocument6 pagesEffect of A Program of Physical Activity Motivated by Lipid Parameters of Patients With Obesity and or Overweight PDFMarlio Andres Vargas PolaniaNo ratings yet

- Local Government Financial Statistics England #23-2013Document222 pagesLocal Government Financial Statistics England #23-2013Xavier Endeudado Ariztía FischerNo ratings yet

- Nitroimidazole Wps OfficeDocument10 pagesNitroimidazole Wps OfficeCamelle DiniayNo ratings yet

- SHS 079 2021 - 12STEM C - Group9Document62 pagesSHS 079 2021 - 12STEM C - Group9NATIOLA HYTHAM XYRUS A.No ratings yet

- Hazard Scale: 0 Minimal 1 Slight 2 Moderate 3 Serious 4 Severe Chronic HazardDocument4 pagesHazard Scale: 0 Minimal 1 Slight 2 Moderate 3 Serious 4 Severe Chronic HazardNazirAhmadBashiriNo ratings yet

- UrethralstricturesDocument37 pagesUrethralstricturesNinaNo ratings yet

- SIPDocument2 pagesSIPRowena Abdula BaronaNo ratings yet

- First Year Student Orientation: University of DenverDocument3 pagesFirst Year Student Orientation: University of DenverRyan DonovanNo ratings yet

- Written Assignment Unit 2 - HS 2212Document5 pagesWritten Assignment Unit 2 - HS 2212bnvjNo ratings yet

- Brain Tumors - KY Cancer RegistryDocument45 pagesBrain Tumors - KY Cancer RegistryMohammad Galih PratamaNo ratings yet

- VedicReport10 29 202211 43 48AMDocument1 pageVedicReport10 29 202211 43 48AMAvish DussoyeNo ratings yet

- Engineering Practice - Workplace Safety and HealthDocument68 pagesEngineering Practice - Workplace Safety and HealthignatiusNo ratings yet