You might also like

- Exercise 1 5Document1 pageExercise 1 5lheamaecayabyab4No ratings yet

- Answer To Sample Question 2Document3 pagesAnswer To Sample Question 2Farid AbbasovNo ratings yet

- P 5 - Assigned Tasks Afar302aDocument7 pagesP 5 - Assigned Tasks Afar302aLyn CosNo ratings yet

- FAR Chapter 4Document5 pagesFAR Chapter 4Celine Therese BuNo ratings yet

- Chapter 11 17Document62 pagesChapter 11 17Melissa Cabigat Abdul KarimNo ratings yet

- Questions12-18 SolvedDocument9 pagesQuestions12-18 SolvedDaxhing RajaNo ratings yet

- HOMEWORK 1 (No. 14)Document7 pagesHOMEWORK 1 (No. 14)Joana TrinidadNo ratings yet

- Konsolidasi A. Alokasi Harga: Nama: Muhammad Fadhil NIM: 023152000055 Matkul: Pelaporan KorporatDocument7 pagesKonsolidasi A. Alokasi Harga: Nama: Muhammad Fadhil NIM: 023152000055 Matkul: Pelaporan KorporatMuhammad FadhilNo ratings yet

- My Company Unadjusted Trial Balance December 31, 2018 Debit CreditDocument9 pagesMy Company Unadjusted Trial Balance December 31, 2018 Debit CreditRey Joyce AbuelNo ratings yet

- Inventories and Related Expenses: Multiple Choice - TheoryDocument14 pagesInventories and Related Expenses: Multiple Choice - TheoryMadielyn Santarin MirandaNo ratings yet

- Statement of Profit or Loss For The Year Ended 31 December 2016Document2 pagesStatement of Profit or Loss For The Year Ended 31 December 2016Plawan GhimireNo ratings yet

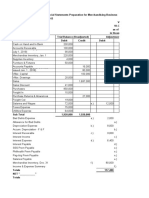

- DB6 - Worksheet & FS Prep For Merchandising BusinessDocument4 pagesDB6 - Worksheet & FS Prep For Merchandising BusinessArrianeNo ratings yet

- Activity Review StatementDocument5 pagesActivity Review Statementangel ciiiNo ratings yet

- Chapter 17 Answer Key-1Document4 pagesChapter 17 Answer Key-1NCTNo ratings yet

- Mahusay, Bsa 315, Module 1-CaseletsDocument9 pagesMahusay, Bsa 315, Module 1-CaseletsJeth MahusayNo ratings yet

- Transactions - Year 2015Document23 pagesTransactions - Year 2015raeq109No ratings yet

- Jawaban TugasDocument23 pagesJawaban TugasRusnawati Nur AminahNo ratings yet

- CONSO FS Cost MethodDocument21 pagesCONSO FS Cost MethodMaurice AgbayaniNo ratings yet

- Acc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)Document1 pageAcc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)nicole bancoroNo ratings yet

- AC 1104 Ans C-1 2022Document7 pagesAC 1104 Ans C-1 2022Charles LaspiñasNo ratings yet

- Sample ProblemDocument4 pagesSample ProblemENIDNo ratings yet

- Acctg Problem 7Document4 pagesAcctg Problem 7Salvie Perez Utana57% (14)

- Allan & WallyDocument10 pagesAllan & WallyLaura OliviaNo ratings yet

- Accounting For Partnership Formation Activity 2 - Sole Proprietors Form A Partnership Gab BusinessDocument3 pagesAccounting For Partnership Formation Activity 2 - Sole Proprietors Form A Partnership Gab BusinessChinee CastilloNo ratings yet

- Problem 2: Income StatementDocument1 pageProblem 2: Income StatementazisridwansyahNo ratings yet

- 16 UNIT III LiquidationDocument20 pages16 UNIT III LiquidationLeslie Mae Vargas ZafeNo ratings yet

- Entry Made Correct/Should Be EntryDocument15 pagesEntry Made Correct/Should Be EntryLove FreddyNo ratings yet

- BADVAC2X Review (Partnership Formation-Dissolution) - P1Document15 pagesBADVAC2X Review (Partnership Formation-Dissolution) - P1Reymark SadoyNo ratings yet

- 17 - Accounting For Incomplete Records (Single Entry)Document7 pages17 - Accounting For Incomplete Records (Single Entry)KAMAL POKHRELNo ratings yet

- PDF Far Quiz 2 Final W Answers - CompressDocument3 pagesPDF Far Quiz 2 Final W Answers - CompressdasdsadsadasdasdNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationunknown PersonNo ratings yet

- MODULE 2 JOINT ARRANGEMENTS ASSIGNMENT AAC2 Mar 2023 - Copy-1Document3 pagesMODULE 2 JOINT ARRANGEMENTS ASSIGNMENT AAC2 Mar 2023 - Copy-1Lorifel Antonette Laoreno TejeroNo ratings yet

- Date Januar y Accounts Title Description P R Debts CreditDocument3 pagesDate Januar y Accounts Title Description P R Debts CreditMariel Samonte VillanuevaNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- AccountingDocument4 pagesAccountingAnne AlagNo ratings yet

- Partnership Formation ProblemDocument14 pagesPartnership Formation ProblemAinne TanNo ratings yet

- Module 7Document9 pagesModule 7Jacqueline OrtegaNo ratings yet

- Perpetual Answer KeyDocument11 pagesPerpetual Answer KeyRichelle Janine Dela CruzNo ratings yet

- AssignmentDocument5 pagesAssignmentJJ JaumNo ratings yet

- Partnership Liquidation - Grp1Document2 pagesPartnership Liquidation - Grp1Andrea BreisNo ratings yet

- Silid Act 6 - BALDERASDocument2 pagesSilid Act 6 - BALDERASJustine Marie BalderasNo ratings yet

- Vending Machines SolutionDocument6 pagesVending Machines SolutionizquierdofacturaNo ratings yet

- PDF-Afar CompressDocument128 pagesPDF-Afar CompressCharisse VisteNo ratings yet

- Afar Partnership LiquidationDocument42 pagesAfar Partnership LiquidationKrizia Mae Uzielle PeneroNo ratings yet

- A 1. FormationDocument3 pagesA 1. Formationmartinfaith958No ratings yet

- Intacc Quiz 1Document6 pagesIntacc Quiz 1Rhea YugaNo ratings yet

- Mahusay, Bsa 315 - Module 2-CaseletsDocument10 pagesMahusay, Bsa 315 - Module 2-CaseletsJeth MahusayNo ratings yet

- Account For Home Office and Branch Transactions. ProblemDocument2 pagesAccount For Home Office and Branch Transactions. ProblemDevine Grace A. MaghinayNo ratings yet

- Fund Flow Statement NumericalsDocument9 pagesFund Flow Statement Numericalsjaydeep kriplaniNo ratings yet

- Module 3 - Solutions #2 (2022)Document11 pagesModule 3 - Solutions #2 (2022)Mergierose DalgoNo ratings yet

- Christine Sousa BagsDocument8 pagesChristine Sousa BagsKaila Clarisse Cortez100% (5)

- Merger Problems & SolutionsDocument8 pagesMerger Problems & Solutionsmisonim.eNo ratings yet

- Assignment in Financial Accounting: Jane B. Evangelista Bsba-2BDocument4 pagesAssignment in Financial Accounting: Jane B. Evangelista Bsba-2BJane Barcelona Evangelista0% (1)

- Accn 101 Assignment Group WorkDocument8 pagesAccn 101 Assignment Group WorkkumbiraidavidNo ratings yet

- Ae 100 Section L Navarro, LainaDocument14 pagesAe 100 Section L Navarro, LainaLaina Recel NavarroNo ratings yet

- 158 716 Answtest2bDocument18 pages158 716 Answtest2blisa lheneNo ratings yet

- T1 - ABFA1153 (Extra)Document1 pageT1 - ABFA1153 (Extra)LOO YU HUANGNo ratings yet

- Multiple Choice ProblemsDocument5 pagesMultiple Choice ProblemsHannahbea LindoNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- HarleydavidsonDocument4 pagesHarleydavidsonminmenmNo ratings yet

- September 5, 2018: MAPFE INSULAR Insurance CorporationDocument3 pagesSeptember 5, 2018: MAPFE INSULAR Insurance CorporationminmenmNo ratings yet

- September 5, 2018: MAPFE INSULAR Insurance CorporationDocument3 pagesSeptember 5, 2018: MAPFE INSULAR Insurance CorporationminmenmNo ratings yet

- WP AR RDelaRuedaDocument1 pageWP AR RDelaRuedaminmenmNo ratings yet

- Thesis Survey SummaryDocument6 pagesThesis Survey SummaryminmenmNo ratings yet

- Final Demo LP Nails TuesDocument3 pagesFinal Demo LP Nails Tuesminmenm94% (16)

- IRR ContestsDocument4 pagesIRR ContestsminmenmNo ratings yet

- Saluyot As Alternative Bar SoapDocument1 pageSaluyot As Alternative Bar SoapminmenmNo ratings yet

- My Father Goes To Court2Document8 pagesMy Father Goes To Court2minmenmNo ratings yet

- Graph Exponential FunctionsDocument6 pagesGraph Exponential FunctionsminmenmNo ratings yet

- Idiomatic Expressions: Part-Time Job. It Seems He Has Bitten Off More Than He Can ChewDocument1 pageIdiomatic Expressions: Part-Time Job. It Seems He Has Bitten Off More Than He Can ChewminmenmNo ratings yet

- Chapter 7 Advance Accounting Volume 1 2008Document15 pagesChapter 7 Advance Accounting Volume 1 2008andrewhomil_17199886% (7)

- The Role of Sustainability in Brand Equity Value in The Financial SectorDocument19 pagesThe Role of Sustainability in Brand Equity Value in The Financial SectorPrasiddha PradhanNo ratings yet

- Coca Cola Mini CaseDocument1 pageCoca Cola Mini CaseDania Sekar WuryandariNo ratings yet

- Presentation by Arun Thukral, MD CIBILDocument14 pagesPresentation by Arun Thukral, MD CIBILsaadsaaidNo ratings yet

- Fins 2624 Quiz 1Document3 pagesFins 2624 Quiz 1sagarox7No ratings yet

- JetBlue Case StudyDocument4 pagesJetBlue Case StudyXing Liang Huang100% (1)

- SEC Advisory Re MiningDocument3 pagesSEC Advisory Re MiningBobby Olavides SebastianNo ratings yet

- Managerial AccountingDocument18 pagesManagerial Accountingirfan103158No ratings yet

- Bdo - New Sec Cert Complete With Scanned LoiDocument4 pagesBdo - New Sec Cert Complete With Scanned LoiAnonymous p4ztizCSOz80% (10)

- Plantilla de Excel Con Dashboard FinancieroDocument36 pagesPlantilla de Excel Con Dashboard FinancieroSamuel FLoresNo ratings yet

- Research PPT On Online TradingDocument10 pagesResearch PPT On Online TradingbhagyashreeNo ratings yet

- Investment Banking - Course OutlineDocument4 pagesInvestment Banking - Course OutlineVrinda GargNo ratings yet

- Financial Analysis & Modelling Using ExcelDocument2 pagesFinancial Analysis & Modelling Using Excel360 International Limited33% (3)

- IYP II - CRISIL Grading ReportDocument3 pagesIYP II - CRISIL Grading ReportRajibDebNo ratings yet

- Indraprastha Gas Limited - SWOT AnalysisDocument27 pagesIndraprastha Gas Limited - SWOT Analysissujaysarkar850% (1)

- Case MatleDocument11 pagesCase MatleKartika Putri TamaylaNo ratings yet

- CKR Ib4 Inppt 12Document38 pagesCKR Ib4 Inppt 12hunble personNo ratings yet

- Dhaka Bank Annual Report 2015Document278 pagesDhaka Bank Annual Report 2015NagibMahfuzFuad100% (1)

- FMGT 7121 Module 6 - 8th EditionDocument11 pagesFMGT 7121 Module 6 - 8th EditionhilaryNo ratings yet

- Rebuilding Business and Investment in Post-Conflict Sierra LeoneDocument23 pagesRebuilding Business and Investment in Post-Conflict Sierra LeoneInternational Finance Corporation (IFC)No ratings yet

- Tile - : Private Company ProfileDocument27 pagesTile - : Private Company ProfileVincent LuiNo ratings yet

- Shoe Company PaperDocument17 pagesShoe Company PaperxebraNo ratings yet

- Investor Presentation (Company Update)Document28 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Business and Management Dictionary and Glossary of Terminology, Words, Terms, and Definitions - Mian Terms and Unsusual Amusing Business-SpeakDocument118 pagesBusiness and Management Dictionary and Glossary of Terminology, Words, Terms, and Definitions - Mian Terms and Unsusual Amusing Business-SpeakSophia Yeiji ShinNo ratings yet

- Sole PropritorshipDocument6 pagesSole Propritorshipacharla55490% (1)

- Money MarketDocument21 pagesMoney MarketPratik ShethNo ratings yet

- Acctax1 AY 2016-2017 ProblemsDocument77 pagesAcctax1 AY 2016-2017 ProblemsRebekahNo ratings yet

- Statements of Financial Position As at 30 June 20X8 20X7Document4 pagesStatements of Financial Position As at 30 June 20X8 20X7Nguyễn Ngọc HàNo ratings yet

- Project Report ON Ratio Analysis of HCL TechnologiesDocument11 pagesProject Report ON Ratio Analysis of HCL TechnologiesVasudha NagpalNo ratings yet

- On Presston Engineering CorporationDocument21 pagesOn Presston Engineering CorporationPreethi Pavana100% (1)

- Bcel 2019Q1Document1 pageBcel 2019Q1Dương NguyễnNo ratings yet