You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Gale Force SurfingDocument18 pagesGale Force SurfingKhris Keleher50% (4)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Moral Damages (Louisiana Law Rev)Document29 pagesMoral Damages (Louisiana Law Rev)Beau MasiglatNo ratings yet

- Downloadfile 30 PDFDocument114 pagesDownloadfile 30 PDFYianniAnd Sophia0% (1)

- Emergent Payments India Private Limited Tax InvoiceDocument1 pageEmergent Payments India Private Limited Tax InvoiceSuganthan SundharamNo ratings yet

- Dawson CaseDocument8 pagesDawson CaseBeau MasiglatNo ratings yet

- Rule 52 - Pascual V FC Rural Bank BoholDocument9 pagesRule 52 - Pascual V FC Rural Bank BoholBeau MasiglatNo ratings yet

- Launchctl Unload - F /System/Library/Launchagents/Com - Apple.Bezelui - PlistDocument1 pageLaunchctl Unload - F /System/Library/Launchagents/Com - Apple.Bezelui - PlistBeau MasiglatNo ratings yet

- 05 Berger V National Collegiate Athletic AssociationDocument9 pages05 Berger V National Collegiate Athletic AssociationBeau MasiglatNo ratings yet

- A.M. No. 03-02-05-SC - Rule On Guardianship of MinorsDocument10 pagesA.M. No. 03-02-05-SC - Rule On Guardianship of MinorsBeau MasiglatNo ratings yet

- CRALaw - Labor Law Pre Week (2018)Document153 pagesCRALaw - Labor Law Pre Week (2018)freegalado100% (17)

- Zoom G2.1u English ManualDocument25 pagesZoom G2.1u English ManualKevin KerberNo ratings yet

- KBP Broadcast Code 2011Document52 pagesKBP Broadcast Code 2011Jairdan BabacNo ratings yet

- Land Titles Jason DigestsDocument68 pagesLand Titles Jason DigestsBenBulac100% (1)

- A.M. No. 08-1-16-SC - Rule On The Writ of Habeas DataDocument8 pagesA.M. No. 08-1-16-SC - Rule On The Writ of Habeas DataBeau MasiglatNo ratings yet

- You Hurt My Feelings Now Pay Up - Should Objective Evidence Be ReDocument17 pagesYou Hurt My Feelings Now Pay Up - Should Objective Evidence Be ReBeau MasiglatNo ratings yet

- J. Del Castillo - Labor LawDocument57 pagesJ. Del Castillo - Labor LawLeigh aliasNo ratings yet

- Campanilla Crim PreWeek 2018Document42 pagesCampanilla Crim PreWeek 2018Beau Masiglat100% (2)

- 03 Zinn V ParrishDocument7 pages03 Zinn V ParrishBeau MasiglatNo ratings yet

- 01 Santa Fe Independent School Dist V DoeDocument19 pages01 Santa Fe Independent School Dist V DoeBeau MasiglatNo ratings yet

- Fact and TruthDocument22 pagesFact and TruthBeau MasiglatNo ratings yet

- The Problem of Robot ConsciousnessDocument18 pagesThe Problem of Robot ConsciousnessBeau MasiglatNo ratings yet

- Emotional Robots - The Impact of Robots With Feelings and Award of Moral Damages For Their Hurt FeelingDocument29 pagesEmotional Robots - The Impact of Robots With Feelings and Award of Moral Damages For Their Hurt FeelingBeau MasiglatNo ratings yet

- 00 Citizens United V FEC Scalia ConcurringDocument9 pages00 Citizens United V FEC Scalia ConcurringBeau MasiglatNo ratings yet

- Can A Robot Be A 'Person' With Rights - , Opinion News & Top Stories - The Straits TimesDocument4 pagesCan A Robot Be A 'Person' With Rights - , Opinion News & Top Stories - The Straits TimesBeau MasiglatNo ratings yet

- Beware Emotional Robots - Giving Feelings To Artificial Beings Could Backfire, Study Suggests - Science - AAASDocument8 pagesBeware Emotional Robots - Giving Feelings To Artificial Beings Could Backfire, Study Suggests - Science - AAASBeau MasiglatNo ratings yet

- 01 Fighting Falsity - Fake News, Facebook, and The First AmendmentDocument39 pages01 Fighting Falsity - Fake News, Facebook, and The First AmendmentBeau Masiglat0% (1)

- Tagaytay Realty V Gacutan - G.R. No. 160033, July 01, 2015Document12 pagesTagaytay Realty V Gacutan - G.R. No. 160033, July 01, 2015Beau MasiglatNo ratings yet

- Rule On Electronic EvidenceDocument12 pagesRule On Electronic EvidenceBeau MasiglatNo ratings yet

- A Thousand MilesDocument6 pagesA Thousand MilesBeau MasiglatNo ratings yet

- To Track Or Not: Understanding Ateneo Law's New Electives SystemDocument2 pagesTo Track Or Not: Understanding Ateneo Law's New Electives SystemBeau MasiglatNo ratings yet

- Knapp V StateDocument4 pagesKnapp V StateBeau MasiglatNo ratings yet

- Knapp V StateDocument4 pagesKnapp V StateBeau MasiglatNo ratings yet

- Week 1 - Key Areas To Review From ACTG4710 - ACTG4720-Post On Canvas-1Document29 pagesWeek 1 - Key Areas To Review From ACTG4710 - ACTG4720-Post On Canvas-1Mike RaitsinNo ratings yet

- Calculating taxes for pediatricians in the PhilippinesDocument6 pagesCalculating taxes for pediatricians in the PhilippinesCalvin Carl D. Delos ReyesNo ratings yet

- Application For Tax Compliance Verification Certificate Non-Individual Taxpayers - EdrDocument1 pageApplication For Tax Compliance Verification Certificate Non-Individual Taxpayers - EdranabuaNo ratings yet

- Deliveroo Order Receipt 2031511209Document2 pagesDeliveroo Order Receipt 2031511209jak.g.lewisNo ratings yet

- Laundry - System Analysis and Design - (Excel Linking)Document10 pagesLaundry - System Analysis and Design - (Excel Linking)JO SANo ratings yet

- RenewalPremium 35616458Document1 pageRenewalPremium 35616458Raghavendra ChinnuNo ratings yet

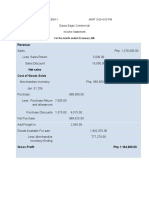

- Davao Eagle Commercial January Income StatementDocument6 pagesDavao Eagle Commercial January Income Statementablay logeneNo ratings yet

- Worksheet 14 ColumnsDocument1 pageWorksheet 14 ColumnsPrincess AudhrieNo ratings yet

- Mireillenkuansambumiss DiavuaDocument3 pagesMireillenkuansambumiss DiavuaMayamona Nkuansambu LikeNo ratings yet

- Taxation 1 ReviewerDocument5 pagesTaxation 1 ReviewerEISEN BELWIGANNo ratings yet

- PajakDocument84 pagesPajakDHEASITANo ratings yet

- Ball Corporation Job Offer LetterDocument2 pagesBall Corporation Job Offer LetterSatyabrata RautaNo ratings yet

- Solution of Governmentl CH 5Document18 pagesSolution of Governmentl CH 5Ahmad KamalNo ratings yet

- Tax Accounting ConceptsDocument17 pagesTax Accounting ConceptsKathleenAlfaroDelosoNo ratings yet

- Screenshot 2023-12-12 at 2.34.53 PMDocument1 pageScreenshot 2023-12-12 at 2.34.53 PMshashikumarsk0711No ratings yet

- 1 MondayDocument6 pages1 MondayCeline Marie Libatique AntonioNo ratings yet

- Si04253409 4 PDFDocument1 pageSi04253409 4 PDFclintNo ratings yet

- Retail BankingDocument238 pagesRetail BankingMukesh SainiNo ratings yet

- Unicredit vs. IngDocument3 pagesUnicredit vs. IngAlina AndrioaeNo ratings yet

- BIR Ruling 023-09Document5 pagesBIR Ruling 023-09Juno Geronimo100% (1)

- 1511256898711park Cubix Price Sheet 2 9 17 PDFDocument1 page1511256898711park Cubix Price Sheet 2 9 17 PDFManjunathNo ratings yet

- Super ForgingsDocument2 pagesSuper Forgingsbikkumalla shivaprasadNo ratings yet

- New Income Tax Rates for Corporations Under CREATEDocument22 pagesNew Income Tax Rates for Corporations Under CREATEJeanette LampitocNo ratings yet

- 365) - The Income Tax Rate Is 40%. Additional Expenses Are Estimated As FollowsDocument3 pages365) - The Income Tax Rate Is 40%. Additional Expenses Are Estimated As FollowsMihir HareetNo ratings yet

- Reliance Retail Limited: Sr. No. Item Name Hsn/Sac Qty Price/Unit Discount ValueDocument3 pagesReliance Retail Limited: Sr. No. Item Name Hsn/Sac Qty Price/Unit Discount ValuemukeshNo ratings yet

- 返金規定 英語版 Refund policyDocument2 pages返金規定 英語版 Refund policyDai1 AcademyNo ratings yet

- B-4 Account Computation PFC SuerteDocument3 pagesB-4 Account Computation PFC SuerteElmer AlasNo ratings yet