You might also like

- 21 Intangible AssetsDocument6 pages21 Intangible AssetsAdrian MallariNo ratings yet

- P1 QuestionsDocument11 pagesP1 QuestionsjustjadeNo ratings yet

- Quiz - IntangiblesDocument1 pageQuiz - IntangiblesAna Mae HernandezNo ratings yet

- Preweek Practical Accounting 1Document24 pagesPreweek Practical Accounting 1alellieNo ratings yet

- Practical Accounting 1Document8 pagesPractical Accounting 1Mina Bianca AutencioNo ratings yet

- Advanced Financial Accounting 1Document12 pagesAdvanced Financial Accounting 1Gemine Ailna Panganiban NuevoNo ratings yet

- Preweek ReviewDocument31 pagesPreweek ReviewLeah Hope CedroNo ratings yet

- Accounting ReviewerDocument22 pagesAccounting ReviewerAira TantoyNo ratings yet

- Act 20-Ap 04 PpeDocument7 pagesAct 20-Ap 04 PpeJomar VillenaNo ratings yet

- Acctg 100C 06 PDFDocument2 pagesAcctg 100C 06 PDFQuid DamityNo ratings yet

- Multiple Choices - Quiz - Chapter 1-To-3Document21 pagesMultiple Choices - Quiz - Chapter 1-To-3Ella SingcaNo ratings yet

- Ps B ABC and JitDocument4 pagesPs B ABC and JitMedalla NikkoNo ratings yet

- WileyPlus PPEDocument9 pagesWileyPlus PPEKaiWenNgNo ratings yet

- Pampanga Practical Accounting 2 PreweekDocument22 pagesPampanga Practical Accounting 2 PreweekYaj CruzadaNo ratings yet

- Derivatives 2Document4 pagesDerivatives 2Jenelyn Ubanan100% (1)

- Chapter 8 AssignmentDocument3 pagesChapter 8 AssignmentThermen DarenNo ratings yet

- Interim Financial ReportingDocument4 pagesInterim Financial ReportingMia CruzNo ratings yet

- Financial Accounting and Reporting PartDocument6 pagesFinancial Accounting and Reporting PartLalaine De JesusNo ratings yet

- 02 Cash and Cash Equivalents PDFDocument19 pages02 Cash and Cash Equivalents PDFReyn Saplad PeralesNo ratings yet

- CH 24 Quiz ADocument12 pagesCH 24 Quiz AAaron Carter KennedyNo ratings yet

- TOA Quizzer 1 - Intro To PFRSDocument6 pagesTOA Quizzer 1 - Intro To PFRSmarkNo ratings yet

- REVIEWer Take Home QuizDocument3 pagesREVIEWer Take Home QuizNeirish fainsan0% (1)

- FAR.3405 PPE-Acquisition and Subsequent ExpendituresDocument6 pagesFAR.3405 PPE-Acquisition and Subsequent ExpendituresMonica GarciaNo ratings yet

- 6902 - Investment Property and Other InvestmentDocument3 pages6902 - Investment Property and Other InvestmentAljur SalamedaNo ratings yet

- DLSU REVDEVT - TOA Revised Reviewer - Answer Key PDFDocument16 pagesDLSU REVDEVT - TOA Revised Reviewer - Answer Key PDFabbyNo ratings yet

- Final Exam Advance Accounting WADocument5 pagesFinal Exam Advance Accounting WAShawn OrganoNo ratings yet

- Accounting For Labor 3Document13 pagesAccounting For Labor 3Charles Reginald K. HwangNo ratings yet

- Hakdog PDFDocument18 pagesHakdog PDFJay Mark AbellarNo ratings yet

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREDocument12 pagesACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaNo ratings yet

- All in CupDocument11 pagesAll in CupRosemarie Qui0% (1)

- Toa 10 001Document7 pagesToa 10 001JohnAllenMarillaNo ratings yet

- Investment in Associate-Mytha Isabel D. SalesDocument9 pagesInvestment in Associate-Mytha Isabel D. SalesMytha Isabel SalesNo ratings yet

- Development of Financial Reporting Framework and Standard-Setting BodiesDocument3 pagesDevelopment of Financial Reporting Framework and Standard-Setting BodiesPeter BanjaoNo ratings yet

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument3 pagesDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- Tutorial 1 Chapter 7Document8 pagesTutorial 1 Chapter 7Aqila Syakirah IVNo ratings yet

- 6971 - Investment AssociateDocument2 pages6971 - Investment AssociateMarjhon TubillaNo ratings yet

- MidtermExam Fin3 (Prac)Document10 pagesMidtermExam Fin3 (Prac)Raymond PacaldoNo ratings yet

- Cost AssignmentDocument3 pagesCost AssignmentAbrha GidayNo ratings yet

- Integrated Accounting Review - AFAR T1, AY 2023-2024Document40 pagesIntegrated Accounting Review - AFAR T1, AY 2023-2024Conteza EliasNo ratings yet

- Finacct Mock Exam 1Document7 pagesFinacct Mock Exam 1Joseph Gerald M. ArcegaNo ratings yet

- Intermediate Accounting I Investment in Associate Part 2Document3 pagesIntermediate Accounting I Investment in Associate Part 2Fery AnnNo ratings yet

- AFAR - Corpo Liquidation: Home Office and Branch AccountingDocument5 pagesAFAR - Corpo Liquidation: Home Office and Branch AccountingJustine CruzNo ratings yet

- Chapter 6: Non-Current Assets Held For Sale (Ifrs 5Document2 pagesChapter 6: Non-Current Assets Held For Sale (Ifrs 5Kiana FernandezNo ratings yet

- Auditing Problems Key Answers/solutions: Problem No. 1 1.A, 2.C, 3.B, 4.B, 5.DDocument14 pagesAuditing Problems Key Answers/solutions: Problem No. 1 1.A, 2.C, 3.B, 4.B, 5.DKim Cristian MaañoNo ratings yet

- TOA MockBoardDocument16 pagesTOA MockBoardHansard Labisig100% (1)

- AcctgDocument14 pagesAcctgLara Lewis AchillesNo ratings yet

- Exercises 04 - Intangibles INTACC2 PDFDocument3 pagesExercises 04 - Intangibles INTACC2 PDFKhan TanNo ratings yet

- Cash and Cash EquivalentsDocument8 pagesCash and Cash EquivalentsmissyNo ratings yet

- Weston Corporation Has An Internal Audit Department Operating OuDocument2 pagesWeston Corporation Has An Internal Audit Department Operating OuAmit PandeyNo ratings yet

- AP 59 FinPB - 5.06Document8 pagesAP 59 FinPB - 5.06Anonymous Lih1laaxNo ratings yet

- AFAR8717 Joint Arrangement SolutionsDocument2 pagesAFAR8717 Joint Arrangement SolutionsGJames ApostolNo ratings yet

- Bastrcsx q1m Set BDocument9 pagesBastrcsx q1m Set BAdrian MontemayorNo ratings yet

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Document6 pagesPhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)Mary Jo Lariz OcliasoNo ratings yet

- Ac3a Qe Oct2014 (TQ)Document15 pagesAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- FAR.2906 - PPE-Depreciation and Derecognition.Document4 pagesFAR.2906 - PPE-Depreciation and Derecognition.John Nathan KinglyNo ratings yet

- Review Questions: Group 1Document21 pagesReview Questions: Group 1AIKO MAGUINSAWANNo ratings yet

- In June 2010 Carolyn Gardens Incurred The Following Costs OneDocument1 pageIn June 2010 Carolyn Gardens Incurred The Following Costs OneAmit PandeyNo ratings yet

- CPA - Quizbowl 2008Document10 pagesCPA - Quizbowl 2008frankreedh100% (3)

- Conceptual Framework and Accounting StandardsDocument11 pagesConceptual Framework and Accounting StandardsAngela TalastasNo ratings yet

- 1-Jun 3-Jun 5-Jun 6-Jun 7-Jun 10-Jun 12-Jun 13-Jun 14-Jun 15-Jun 17-Jun 18-Jun 20-Jun 25-Jun 27-Jun 30-JunDocument2 pages1-Jun 3-Jun 5-Jun 6-Jun 7-Jun 10-Jun 12-Jun 13-Jun 14-Jun 15-Jun 17-Jun 18-Jun 20-Jun 25-Jun 27-Jun 30-JunLara Lewis AchillesNo ratings yet

- NewTracksDocument1 pageNewTracksLara Lewis AchillesNo ratings yet

- Cost Concepts and CVP AnalysisDocument7 pagesCost Concepts and CVP AnalysisLara Lewis AchillesNo ratings yet

- AcctgDocument14 pagesAcctgLara Lewis AchillesNo ratings yet

- Seatwork Acctg 1Document8 pagesSeatwork Acctg 1Lara Lewis AchillesNo ratings yet

- Adjusted Cash Balance Per Bank $ 17,170Document2 pagesAdjusted Cash Balance Per Bank $ 17,170Lara Lewis AchillesNo ratings yet

- Rubric For Research PaperDocument1 pageRubric For Research PaperLara Lewis AchillesNo ratings yet

- NewTracksDocument1 pageNewTracksLara Lewis AchillesNo ratings yet

- Ceo and Chairman, Tesla NET WORTH: $20.5 BDocument13 pagesCeo and Chairman, Tesla NET WORTH: $20.5 BLara Lewis AchillesNo ratings yet

- Assignment 6Document8 pagesAssignment 6Lara Lewis AchillesNo ratings yet

- Mock CPA Board Examinations (p2)Document8 pagesMock CPA Board Examinations (p2)Lara Lewis Achilles100% (1)

- Mock CPA Board Examinations (Mas)Document8 pagesMock CPA Board Examinations (Mas)Lara Lewis Achilles100% (1)

- NCR Cup Quiz 1Document7 pagesNCR Cup Quiz 1Lara Lewis AchillesNo ratings yet

- Project SolutionDocument11 pagesProject SolutionLara Lewis AchillesNo ratings yet

- Reniexus Budget Project, 2010Document1 pageReniexus Budget Project, 2010Lara Lewis AchillesNo ratings yet

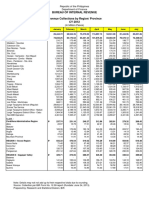

- Coll Per NSCB Region - CY 2012Document6 pagesColl Per NSCB Region - CY 2012Lara Lewis AchillesNo ratings yet

- Closing Time - SemisonicDocument1 pageClosing Time - SemisonicLara Lewis AchillesNo ratings yet

- History of Banking in IndiaDocument5 pagesHistory of Banking in IndiamylahNo ratings yet

- Axiata Group Berhad: 1HFY10 Net Profit More Than Doubles - 26/08/2010Document5 pagesAxiata Group Berhad: 1HFY10 Net Profit More Than Doubles - 26/08/2010Rhb InvestNo ratings yet

- AC Exam PDF - 2020 (Dec 1, 2019-Mar 31, 2020) by AffairsCloud-1 PDFDocument135 pagesAC Exam PDF - 2020 (Dec 1, 2019-Mar 31, 2020) by AffairsCloud-1 PDFShivam AnandNo ratings yet

- 7 - Strategic Marketing BudgetingDocument28 pages7 - Strategic Marketing BudgetingBusiness MatterNo ratings yet

- Problems 123Document52 pagesProblems 123Dharani RiteshNo ratings yet

- GPA Lecture 1 2023 PostDocument56 pagesGPA Lecture 1 2023 PostLmv 2022No ratings yet

- H C D C: OLY Ross OF Avao OllegeDocument8 pagesH C D C: OLY Ross OF Avao OllegeFretchiel Mae SusanNo ratings yet

- Presentation On Financial InstrumentsDocument20 pagesPresentation On Financial InstrumentsMehak BhallaNo ratings yet

- Seya-Industries-Result-Presentation - Q1FY201 Seya IndustriesDocument24 pagesSeya-Industries-Result-Presentation - Q1FY201 Seya Industriesabhishek kalbaliaNo ratings yet

- Strategy Session 3Document3 pagesStrategy Session 3Maria Alejandra RamirezNo ratings yet

- 2024 Republican Study Committee BudgetDocument167 pages2024 Republican Study Committee BudgetFedSmith Inc.No ratings yet

- PAD214 Introduction To Public Personnel Administration: Lesson 2 Human Resource Planning (HRP)Document15 pagesPAD214 Introduction To Public Personnel Administration: Lesson 2 Human Resource Planning (HRP)nsaid_31No ratings yet

- Causes of Industrial Backward NessDocument2 pagesCauses of Industrial Backward NessFawad Abbasi100% (1)

- Introduction To Accounting - Principles of AccountingDocument178 pagesIntroduction To Accounting - Principles of AccountingAbdulla MaseehNo ratings yet

- OM 1st SemesterDocument32 pagesOM 1st Semestermenna mokhtarNo ratings yet

- Soal PRE-TEST BASIC LEVELDocument9 pagesSoal PRE-TEST BASIC LEVELIndrianiNo ratings yet

- Credit Rating Agencies in IndiaDocument23 pagesCredit Rating Agencies in Indiaanon_315460204No ratings yet

- The Zimbabwean DollarDocument4 pagesThe Zimbabwean DollarDeepak NadarNo ratings yet

- Financial Markets AND Financial Services: Chapter-31Document7 pagesFinancial Markets AND Financial Services: Chapter-31Dipali DavdaNo ratings yet

- 1801 SilvozaDocument1 page1801 SilvozaKate Hazzle JandaNo ratings yet

- Squad3.fire NSD GPMDocument7 pagesSquad3.fire NSD GPMMac CorpuzNo ratings yet

- Coal India Limited ProjectDocument61 pagesCoal India Limited ProjectShubham KhuranaNo ratings yet

- Make in India Advantages, Disadvantages and Impact On Indian EconomyDocument8 pagesMake in India Advantages, Disadvantages and Impact On Indian EconomyAkanksha SinghNo ratings yet

- Assignment No 1Document6 pagesAssignment No 1Hassan Raza0% (1)

- BLL - Property Management BrochureDocument10 pagesBLL - Property Management BrochureAdedolapo Ademola OdunsiNo ratings yet

- Lic Final ProjectDocument80 pagesLic Final Projectshaibaaz_ibm797354100% (3)

- Taxation Law CIA 1 (B) Salary AnalysisDocument3 pagesTaxation Law CIA 1 (B) Salary Analysisawinash reddyNo ratings yet

- Lehman Brothers Holdings Inc V Jpmorgan Chase Bank Na Amended Counterclaims of Jpmorgan Chase BankDocument69 pagesLehman Brothers Holdings Inc V Jpmorgan Chase Bank Na Amended Counterclaims of Jpmorgan Chase BankForeclosure FraudNo ratings yet

- Assignment 2 Front SheetDocument12 pagesAssignment 2 Front SheetHuy DươngNo ratings yet

- Enquiry Committee On Small Scale Newspapers, 1965 - Shilpa Narani/Suvojit Bandopadhyaya - Semester 3 (Batch 2010 - 2012)Document35 pagesEnquiry Committee On Small Scale Newspapers, 1965 - Shilpa Narani/Suvojit Bandopadhyaya - Semester 3 (Batch 2010 - 2012)altlawforumNo ratings yet