You might also like

- El Teck Magnetic Advacnes Planning DocumentDocument4 pagesEl Teck Magnetic Advacnes Planning DocumentStephanie Ng100% (1)

- Wall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto CurrenciesDocument139 pagesWall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto Currenciesboo100% (5)

- Capital Budgeting Idea For Netflix Inc.Document26 pagesCapital Budgeting Idea For Netflix Inc.PraNo ratings yet

- Months: Sales Purchases Wages ExpensesDocument2 pagesMonths: Sales Purchases Wages Expensespranay639No ratings yet

- RWSchedule 1378198005086Document4 pagesRWSchedule 1378198005086nsaid_31No ratings yet

- Assigment 6 - Managerial Finance Capital BudgetingDocument5 pagesAssigment 6 - Managerial Finance Capital BudgetingNasir ShaheenNo ratings yet

- Summer Internship Project On Stock BrokingDocument109 pagesSummer Internship Project On Stock BrokingArun Kumar Naik86% (7)

- Mas Preweek Handouts - Rodel RoqueDocument10 pagesMas Preweek Handouts - Rodel RoqueElaine Joyce GarciaNo ratings yet

- Budget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Document7 pagesBudget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Suraj KumarNo ratings yet

- FAR Handout Borrowing CostsDocument4 pagesFAR Handout Borrowing CostsBAROTEA Cressia Mhay G.No ratings yet

- Chapter # 7 Exercise & ProblemsDocument4 pagesChapter # 7 Exercise & ProblemsZia Uddin0% (1)

- Finance Questions 3Document2 pagesFinance Questions 3asma raeesNo ratings yet

- Accounting GroupDocument17 pagesAccounting GroupNethmi JayawardhanaNo ratings yet

- Linear Regression . Feb 2020: ExampleDocument6 pagesLinear Regression . Feb 2020: Example신두No ratings yet

- EXERCISEsDocument3 pagesEXERCISEsBenjamin D. RubinNo ratings yet

- Soal Quiz 2020Document6 pagesSoal Quiz 2020Rifka NovrianiNo ratings yet

- Pas 23: Borrowing Cost Borrowing CostDocument7 pagesPas 23: Borrowing Cost Borrowing CostJustine Reine CornicoNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Cash Management: ProblemsDocument4 pagesCash Management: ProblemsPoojitha ReddyNo ratings yet

- Financial PlanDocument3 pagesFinancial Planehoxha22No ratings yet

- Final Exam - Sent StudentsDocument5 pagesFinal Exam - Sent StudentsTrần Nguyễn Tuệ MinhNo ratings yet

- Chapter 4 - Assessment 2 - Working Capital Financing PoliciesDocument3 pagesChapter 4 - Assessment 2 - Working Capital Financing PoliciesRudsan TurquezaNo ratings yet

- BU6009 Assessment 4Document3 pagesBU6009 Assessment 4Sana MohdNo ratings yet

- Requirements:: The Best Way To Learn Is To Teach. Teach A Friend To Learn, Not To CheatDocument2 pagesRequirements:: The Best Way To Learn Is To Teach. Teach A Friend To Learn, Not To CheatHoo ShiNo ratings yet

- Question On Budget A LevelDocument3 pagesQuestion On Budget A LevelMUSTHARI KHANNo ratings yet

- Contoh Latihan Kurva-S Vs Cash FlowDocument40 pagesContoh Latihan Kurva-S Vs Cash FlowHaikal KamalNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- St. Therese Montessori School of San PabloDocument3 pagesSt. Therese Montessori School of San PabloJersey Ann AlcazarNo ratings yet

- Uts Akmen 1Document2 pagesUts Akmen 1Dita EnsNo ratings yet

- C4 W1 Final AssessmentDocument14 pagesC4 W1 Final Assessmentdiktat86No ratings yet

- Cost Benefit AnalysisDocument5 pagesCost Benefit AnalysisJhay-are PogoyNo ratings yet

- ACC 311 Final Project II Student WorkbookDocument21 pagesACC 311 Final Project II Student Workbookdsaaaaaaa100% (1)

- Inflation Forecast For AugustDocument3 pagesInflation Forecast For Augustrebekkah28341No ratings yet

- Executive Summary: Philippines Construction CompanyDocument7 pagesExecutive Summary: Philippines Construction CompanyVon Ulysses CastilloNo ratings yet

- DLP Fs Analysis Concepts and FormatDocument14 pagesDLP Fs Analysis Concepts and FormatDia Did L. RadNo ratings yet

- Questions FolderDocument20 pagesQuestions FolderfaraNo ratings yet

- Cash Management QuestionsDocument5 pagesCash Management QuestionsManasi Jamsandekar100% (1)

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- MP2 Dividend CalculatorDocument12 pagesMP2 Dividend CalculatorJel IbarbiaNo ratings yet

- Manage Finances 2Document7 pagesManage Finances 2Ashish JaatNo ratings yet

- Chapter 22. Mini Case For Other Topics in Working Capital Management Part I. Click On The Part II Tab For The Second Part To This CaseDocument7 pagesChapter 22. Mini Case For Other Topics in Working Capital Management Part I. Click On The Part II Tab For The Second Part To This CaseSafuan HalimNo ratings yet

- Final Exam - Sent StudentsDocument6 pagesFinal Exam - Sent StudentsYến Hoàng HảiNo ratings yet

- Emergency Response Master Budget FormatDocument51 pagesEmergency Response Master Budget FormatNaveed UllahNo ratings yet

- FADocument3 pagesFAYukta GoelNo ratings yet

- Tutorial 1 Questions - Budgeting - Part 1Document7 pagesTutorial 1 Questions - Budgeting - Part 1elainelxy2508No ratings yet

- Management Accounting ExamDocument3 pagesManagement Accounting ExamKeb LimpocoNo ratings yet

- Chapter 25 - Borrowing CostsDocument35 pagesChapter 25 - Borrowing Costsmhel moyetNo ratings yet

- Quiz Audit of ReceivablesDocument4 pagesQuiz Audit of ReceivableswesNo ratings yet

- User Januari Management Produksi Engineering Plant Logistik LC/TC BE IT SHE Finance HR GS IER MCD FinanceDocument96 pagesUser Januari Management Produksi Engineering Plant Logistik LC/TC BE IT SHE Finance HR GS IER MCD FinanceSutrisno Harianto SimanjuntakNo ratings yet

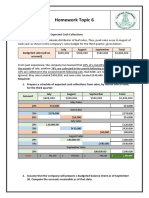

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- 71bepartment of QI:bucation: Epublic of Tbe BilippinesDocument27 pages71bepartment of QI:bucation: Epublic of Tbe BilippinesDarwin AbesNo ratings yet

- Data Section: Statistics and Linear RegressionDocument4 pagesData Section: Statistics and Linear RegressionAngelica FestejoNo ratings yet

- Chapter 7 - Cash BudgetDocument23 pagesChapter 7 - Cash BudgetMostafa KaghaNo ratings yet

- Sample POA SBADocument21 pagesSample POA SBAMia LockNo ratings yet

- Regression and Time SeriesDocument6 pagesRegression and Time Series신두No ratings yet

- FCF Ch10 Excel Master StudentDocument32 pagesFCF Ch10 Excel Master StudentTosa EndrawanNo ratings yet

- This Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)Document8 pagesThis Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)NCT100% (1)

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Financial Plan Free Excel Template by BrainHive Business Planning 1Document11 pagesFinancial Plan Free Excel Template by BrainHive Business Planning 1Balakrishna GopinathNo ratings yet

- FMDQ Markets Monthly ReportDocument9 pagesFMDQ Markets Monthly ReportJohnNo ratings yet

- 05A Examples of Profit ComputationDocument5 pages05A Examples of Profit ComputationPrashant VishwakarmaNo ratings yet

- Final ProjectDocument24 pagesFinal ProjectMohamed ElabassyNo ratings yet

- Soal Teori:: Petunjuk: Kerjakan SOAL TEORI Dan SOAL PRAKTIKA Pada Kolom Jawaban Yang Tersedia !!Document6 pagesSoal Teori:: Petunjuk: Kerjakan SOAL TEORI Dan SOAL PRAKTIKA Pada Kolom Jawaban Yang Tersedia !!irma purnama ningrumNo ratings yet

- AUDCLASS Midterm-ExamDocument7 pagesAUDCLASS Midterm-ExamBeverly MindoroNo ratings yet

- 10 Quiz 1Document1 page10 Quiz 1Lovise DevanNo ratings yet

- Middle East and North Africa Data Book, September 2014From EverandMiddle East and North Africa Data Book, September 2014No ratings yet

- VIIIDocument1 pageVIIIFareha RiazNo ratings yet

- Factories ActDocument1 pageFactories ActFareha RiazNo ratings yet

- Acts Relating To Prisons and Prisoners Rule1Document1 pageActs Relating To Prisons and Prisoners Rule1Fareha RiazNo ratings yet

- Financial ControlDocument1 pageFinancial ControlFareha RiazNo ratings yet

- The Court For A Warrant For His Custody Pending TrialDocument1 pageThe Court For A Warrant For His Custody Pending TrialFareha RiazNo ratings yet

- Job Description of MInes DepartmentDocument3 pagesJob Description of MInes DepartmentFareha RiazNo ratings yet

- Chapter - XV: Fund ElementDocument223 pagesChapter - XV: Fund ElementFareha RiazNo ratings yet

- Section 14: Substantially Financed From Union or State RevenuesDocument5 pagesSection 14: Substantially Financed From Union or State RevenuesFareha RiazNo ratings yet

- Wage TypeDocument4 pagesWage TypeFareha RiazNo ratings yet

- HR CodesDocument51 pagesHR CodesFareha RiazNo ratings yet

- IMSP 06 6-2-1 Part Running Bill PaymentsDocument6 pagesIMSP 06 6-2-1 Part Running Bill PaymentsFareha RiazNo ratings yet

- Stores Part 2Document3 pagesStores Part 2Fareha RiazNo ratings yet

- 2011LHC4023Document6 pages2011LHC4023Fareha RiazNo ratings yet

- GFR CH 2 PDFDocument6 pagesGFR CH 2 PDFFareha RiazNo ratings yet

- GFR ch-4Document14 pagesGFR ch-4Fareha RiazNo ratings yet

- 1000 Islamiat MCQs About Basic InformationDocument11 pages1000 Islamiat MCQs About Basic InformationAyaz Ali100% (1)

- Chapter - 6 Rules Relating To Classification of Losses in Government AccountsDocument2 pagesChapter - 6 Rules Relating To Classification of Losses in Government AccountsFareha RiazNo ratings yet

- 1000 Islamiat MCQs About Basic InformationDocument11 pages1000 Islamiat MCQs About Basic InformationAyaz Ali100% (1)

- GFR CH 2Document6 pagesGFR CH 2Fareha RiazNo ratings yet

- Chapter - 6 Rules Relating To Classification of Losses in Government AccountsDocument2 pagesChapter - 6 Rules Relating To Classification of Losses in Government AccountsFareha RiazNo ratings yet

- Section 14: Substantially Financed From Union or State RevenuesDocument5 pagesSection 14: Substantially Financed From Union or State RevenuesFareha RiazNo ratings yet

- Attempt All Questions From PART-I and Any Two From PART-IIDocument20 pagesAttempt All Questions From PART-I and Any Two From PART-IIFareha RiazNo ratings yet

- Chapter - 6 Rules Relating To Classification of Losses in Government AccountsDocument2 pagesChapter - 6 Rules Relating To Classification of Losses in Government AccountsFareha RiazNo ratings yet

- GFR ch1Document4 pagesGFR ch1Fareha RiazNo ratings yet

- Chapter - 8 Important General Orders Governing ClassificationDocument4 pagesChapter - 8 Important General Orders Governing ClassificationFareha RiazNo ratings yet

- Chapter - 5 Classification of Recoveries of Expenditure in Government AccountsDocument2 pagesChapter - 5 Classification of Recoveries of Expenditure in Government AccountsFareha RiazNo ratings yet

- Stores: Fictitious Stock Adjustments Are Strictly Prohibited, For E.GDocument6 pagesStores: Fictitious Stock Adjustments Are Strictly Prohibited, For E.GFareha RiazNo ratings yet

- 2017 Summer Question PaperDocument3 pages2017 Summer Question PaperFareha RiazNo ratings yet

- Chapter 7 - Miscellaneous RulesDocument2 pagesChapter 7 - Miscellaneous RulesFareha RiazNo ratings yet

- SolutionDocument4 pagesSolutionFareha RiazNo ratings yet

- SFA2 PS Script Health 01212015 (Updated)Document10 pagesSFA2 PS Script Health 01212015 (Updated)markNo ratings yet

- 2013 8 Aug Pay BillDocument118 pages2013 8 Aug Pay Billapi-276412679No ratings yet

- User Manual: Page ContentsDocument22 pagesUser Manual: Page ContentsAnonymous gvHOu4wNo ratings yet

- ThesisDocument73 pagesThesisPhâni Räj Gürâgâin100% (2)

- Allianz Insurance Lanka Ltd. - Allianz Life Insurance Lanka LTDDocument180 pagesAllianz Insurance Lanka Ltd. - Allianz Life Insurance Lanka LTDSOIL TECHNo ratings yet

- "A Study On The Financial Performance of Hindustan Unilever Limited"Document60 pages"A Study On The Financial Performance of Hindustan Unilever Limited"career pathNo ratings yet

- Measuring and Evaluating Bank PerformanceDocument45 pagesMeasuring and Evaluating Bank PerformancepavithragowthamnsNo ratings yet

- Minor Operating Department Medha Singh (127) Muskan AgarwalaDocument3 pagesMinor Operating Department Medha Singh (127) Muskan AgarwalaMedha SinghNo ratings yet

- Acc 124Document35 pagesAcc 124Ikang CabreraNo ratings yet

- Designing An Income Only Irrevocable TrustDocument15 pagesDesigning An Income Only Irrevocable TrusttaurushoNo ratings yet

- 55 - Chapter 6 Exercises With AnswersDocument4 pages55 - Chapter 6 Exercises With Answersgio gioNo ratings yet

- Jawaban C ArthaDocument2 pagesJawaban C ArthaArtha HutapeaNo ratings yet

- Adjustments Quiz 1Document6 pagesAdjustments Quiz 1Christine Mae BurgosNo ratings yet

- Hapter 15: Pearson Education, IncDocument36 pagesHapter 15: Pearson Education, Incbatraz79No ratings yet

- M02 - Cost Accounting CycleDocument6 pagesM02 - Cost Accounting Cyclefirestorm riveraNo ratings yet

- 1997 SADEQ Development and Finance in IslamDocument7 pages1997 SADEQ Development and Finance in IslamDiaz HasvinNo ratings yet

- WP - 209Document29 pagesWP - 209rajk_onlineNo ratings yet

- Transfer PricingDocument22 pagesTransfer PricingParamjit Sharma100% (19)

- China Frozen Beverages Edible Ice Market ReportDocument10 pagesChina Frozen Beverages Edible Ice Market ReportAllChinaReports.comNo ratings yet

- 0807 - Ec 1Document23 pages0807 - Ec 1haryhunter50% (2)

- DocumentDocument3 pagesDocumentMaria Kathreena Andrea AdevaNo ratings yet

- Annual Report 2015 - 16-1WEGAGBNDocument76 pagesAnnual Report 2015 - 16-1WEGAGBNmahteme0% (1)

- EconomicsDocument14 pagesEconomicsJohnNo ratings yet