You might also like

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- Insurance-Digests Complete PDFDocument67 pagesInsurance-Digests Complete PDFDesire RufinNo ratings yet

- Gulf Resorts Inc Vs Philippine Charter Insurance CorporationDocument1 pageGulf Resorts Inc Vs Philippine Charter Insurance CorporationKim Laurente-Alib100% (2)

- Gulf Resorts Inc Vs Philippine Charter Insurance CorporationDocument2 pagesGulf Resorts Inc Vs Philippine Charter Insurance Corporationanon_360675804No ratings yet

- Commercial Law - DAXXDocument730 pagesCommercial Law - DAXXSheron BiaseNo ratings yet

- Gulf Resorts, Inc. V. Philippine Charter Insurance Corporation GR NO 156167, MAY 16, 2005 FactsDocument9 pagesGulf Resorts, Inc. V. Philippine Charter Insurance Corporation GR NO 156167, MAY 16, 2005 Factsmartina lopezNo ratings yet

- 2nd Half Cases-Rulings OnlyDocument39 pages2nd Half Cases-Rulings OnlyalyssamaesanaNo ratings yet

- MODULE 14 Insurance Law EDITEDDocument25 pagesMODULE 14 Insurance Law EDITEDJocelyn GarnadoNo ratings yet

- Gulf Resorts V Phil Charter DigestDocument2 pagesGulf Resorts V Phil Charter Digestdivine venturaNo ratings yet

- Gulf Resorts, Inc., vs. Philippine Charter Insurance CorporationDocument8 pagesGulf Resorts, Inc., vs. Philippine Charter Insurance CorporationRegina AsejoNo ratings yet

- Insurance LawDocument3 pagesInsurance LawSonu MehthaNo ratings yet

- 2 Insurance MidDocument5 pages2 Insurance MidacNo ratings yet

- Assignment No. 8 Insurance To Other Insurance ClauseDocument39 pagesAssignment No. 8 Insurance To Other Insurance ClauseDarlene GanubNo ratings yet

- InsuranceDocument8 pagesInsuranceRegina AsejoNo ratings yet

- E. Insurance Code 1. Gulf Resorts V Phil. Charter InsuranceDocument2 pagesE. Insurance Code 1. Gulf Resorts V Phil. Charter InsuranceJazem AnsamaNo ratings yet

- Insurance NotesDocument13 pagesInsurance NotesIrish Claire FornesteNo ratings yet

- 2018 Insurance Law Notes (Rondez)Document48 pages2018 Insurance Law Notes (Rondez)Troy GonzalesNo ratings yet

- Insurance Law - Reviewer by AIcaoAnotado 2022Document48 pagesInsurance Law - Reviewer by AIcaoAnotado 2022Alena Icao-AnotadoNo ratings yet

- Intro Notes Contract of InsuranceDocument5 pagesIntro Notes Contract of InsuranceEnrique Legaspi IVNo ratings yet

- 2010 Purple Notes - InsuranceDocument40 pages2010 Purple Notes - Insurancejames_bond6233100% (1)

- Commercial Law 2021Document385 pagesCommercial Law 2021Roberto Galano Jr.0% (1)

- Lecture Notes On Insurance: What Laws Govern InsuranceDocument63 pagesLecture Notes On Insurance: What Laws Govern InsuranceAnonymous UbeKTjH3UJNo ratings yet

- InsuranceDocument96 pagesInsuranceLaw MlquNo ratings yet

- Life InsuranceDocument5 pagesLife InsuranceDany100% (1)

- Insurance Digest CompilationDocument45 pagesInsurance Digest CompilationJeffrey FuentesNo ratings yet

- Insurance Law I. Introduction CaseDocument7 pagesInsurance Law I. Introduction CaseSheena Jean Krystle LabaoNo ratings yet

- InsuranceDocument115 pagesInsuranceChris InocencioNo ratings yet

- History of Insurance in The Philippines Spanish EraDocument35 pagesHistory of Insurance in The Philippines Spanish EraLaurene Ashley S QuirosNo ratings yet

- Insurance Law-Insurance ContractDocument14 pagesInsurance Law-Insurance ContractDavid Fong100% (4)

- NCC: Agreement Whereby One Binds Himself Solidarily With The Principal DebtorDocument3 pagesNCC: Agreement Whereby One Binds Himself Solidarily With The Principal DebtorVeronica ChanNo ratings yet

- Insurance-Law CompressDocument4 pagesInsurance-Law Compressrieann leonNo ratings yet

- Insurance Code: 7. Personal - Each Party Having in ViewDocument26 pagesInsurance Code: 7. Personal - Each Party Having in ViewAlberto NicholsNo ratings yet

- Insurance ReviewerDocument16 pagesInsurance Reviewermanol_salaNo ratings yet

- Mhatre 30Document98 pagesMhatre 30sandeepNo ratings yet

- INSURANCE - NotesDocument18 pagesINSURANCE - NotesJulienne Aristoza100% (1)

- Insurance Notes RondezDocument75 pagesInsurance Notes RondezCire GeeNo ratings yet

- Contract of InsuranceDocument10 pagesContract of InsuranceLing EscalanteNo ratings yet

- Grts Inc. v. Philippine Charter Insurance Corp.Document3 pagesGrts Inc. v. Philippine Charter Insurance Corp.Mary Rose Aguinaldo HipolitoNo ratings yet

- Law On InsuranceDocument31 pagesLaw On InsuranceThea DagunaNo ratings yet

- Finman General Assurance Corporation vs. The Honorable Courtof Appeals 213 SCRA 493 September 2, 1992 FactsDocument4 pagesFinman General Assurance Corporation vs. The Honorable Courtof Appeals 213 SCRA 493 September 2, 1992 FactsSamantha BrownNo ratings yet

- L7 BS Law of InsuaranceDocument10 pagesL7 BS Law of InsuaranceIan MutukuNo ratings yet

- Insurance Digests 1Document11 pagesInsurance Digests 1MaryStefanieNo ratings yet

- I. GENERAL PROVISIONS (Sections 1-2) : A. Concept, Purpose and HistoryDocument38 pagesI. GENERAL PROVISIONS (Sections 1-2) : A. Concept, Purpose and HistoryBruno GalwatNo ratings yet

- Insurance ReviewerDocument37 pagesInsurance ReviewerDiane88% (8)

- Insurance Code: P.D. 612 R.A. 10607 Atty. Jobert O. Rillera, CPA, REB, READocument85 pagesInsurance Code: P.D. 612 R.A. 10607 Atty. Jobert O. Rillera, CPA, REB, REAChing ApostolNo ratings yet

- InsuranceDocument57 pagesInsuranceicesootNo ratings yet

- Notes On Insurance - Rene Callanta Insurance Code: (P.D. 1460, As Amended)Document22 pagesNotes On Insurance - Rene Callanta Insurance Code: (P.D. 1460, As Amended)Cervus Augustiniana LexNo ratings yet

- Insurance - Callanta NotesDocument22 pagesInsurance - Callanta NotesCervus Augustiniana LexNo ratings yet

- Insurable Interest: E. Elements of InsuranceDocument2 pagesInsurable Interest: E. Elements of InsuranceMa Jean Baluyo CastanedaNo ratings yet

- Insurance Digest Part 1Document17 pagesInsurance Digest Part 1claudenson18No ratings yet

- Banking and Insurance Unit III Study NotesDocument13 pagesBanking and Insurance Unit III Study NotesSekar M KPRCAS-CommerceNo ratings yet

- Unit 1 Introduction & Development of Insurance LawDocument174 pagesUnit 1 Introduction & Development of Insurance LawAnchalNo ratings yet

- My Internship Report at EFUDocument212 pagesMy Internship Report at EFUAyesha Yasin85% (13)

- Insurance Code-1Document54 pagesInsurance Code-1Gino GinoNo ratings yet

- Claim ManagementDocument58 pagesClaim ManagementSwati Mann100% (2)

- Insurance and Pre-Need1Document20 pagesInsurance and Pre-Need1girlNo ratings yet

- Law of Insurance AnswersheetDocument55 pagesLaw of Insurance Answersheetkhatriparas71No ratings yet

- Essentials of An Insurance ContractDocument7 pagesEssentials of An Insurance ContractSameer JoshiNo ratings yet

- Insurance by RianoDocument15 pagesInsurance by RianoCharm Tan-CalzadoNo ratings yet

- Book Chapter: Philippine Intelligence Community: A Case For TransparencyDocument24 pagesBook Chapter: Philippine Intelligence Community: A Case For TransparencyPBWGNo ratings yet

- Masters National Security Law LoonDocument8 pagesMasters National Security Law LoonPBWGNo ratings yet

- Insurance CasesDocument1 pageInsurance CasesPBWGNo ratings yet

- Ateneo de Zamboanga University: School of Management and AccountancyDocument10 pagesAteneo de Zamboanga University: School of Management and AccountancyPBWGNo ratings yet

- Revised Rules On Administrative Cases in The Civil Service RA 9165 & Its IRR and Plea Bargaining GuidelinesDocument1 pageRevised Rules On Administrative Cases in The Civil Service RA 9165 & Its IRR and Plea Bargaining GuidelinesPBWGNo ratings yet

- WhyDocument3 pagesWhyPBWGNo ratings yet

- Katarungang PambarangayDocument16 pagesKatarungang PambarangayPBWGNo ratings yet

- Property & Succession Reviewer Obligations & Contracts ReviewerDocument2 pagesProperty & Succession Reviewer Obligations & Contracts ReviewerPBWGNo ratings yet

- Ateneo de Zamboanga University Xavier University College of Law - ZamboangaDocument1 pageAteneo de Zamboanga University Xavier University College of Law - ZamboangaPBWGNo ratings yet

- 2016 AdZ Law InstructionsDocument1 page2016 AdZ Law InstructionsPBWGNo ratings yet

- Income Taxation in GeneralDocument9 pagesIncome Taxation in GeneralPBWGNo ratings yet

- 2016 AdZ Law InstructionsDocument1 page2016 AdZ Law InstructionsPBWGNo ratings yet

- MathDocument1 pageMathPBWGNo ratings yet

- Bar ExaminationsDocument68 pagesBar ExaminationsPBWGNo ratings yet

- MF Rep. V CADocument2 pagesMF Rep. V CAPBWGNo ratings yet

- NIL Review CasesDocument1 pageNIL Review CasesPBWGNo ratings yet

- Phy Bar2011Document24 pagesPhy Bar2011PBWGNo ratings yet

- CLR PIL SyllabusDocument9 pagesCLR PIL SyllabusPBWGNo ratings yet

- UNCLOS Summary TableDocument3 pagesUNCLOS Summary Tablecmv mendoza100% (3)

- Art. Xiv: Education, Science & Technology, Arts, Culture and Sports EducationDocument40 pagesArt. Xiv: Education, Science & Technology, Arts, Culture and Sports EducationPBWGNo ratings yet

- Consti AssssDocument117 pagesConsti AssssPBWGNo ratings yet

- CL1 Syllabus 2015Document48 pagesCL1 Syllabus 2015Ateneo SiyaNo ratings yet

- Article XII Til The End.Document7 pagesArticle XII Til The End.PBWGNo ratings yet

- UNCLOSDocument13 pagesUNCLOSPBWGNo ratings yet

- CL1 Syllabus 2015Document48 pagesCL1 Syllabus 2015Ateneo SiyaNo ratings yet

- Political Law 2014 Bar SyllabusDocument13 pagesPolitical Law 2014 Bar SyllabusMarge RoseteNo ratings yet

- Case AssDocument34 pagesCase AssPBWG0% (1)

- League of The Cities v. COMELEC - DigestDocument2 pagesLeague of The Cities v. COMELEC - DigestJilliane Oria100% (2)

- UNCLOSDocument13 pagesUNCLOSPBWGNo ratings yet

- HSE Policy Statement, SchlumbergerDocument1 pageHSE Policy Statement, SchlumbergerProf C.S.PurushothamanNo ratings yet

- Navarro v. SolidumDocument6 pagesNavarro v. SolidumJackelyn GremioNo ratings yet

- Decongestion of PNP Lock-Up Cells DTD August 14, 2012 PDFDocument3 pagesDecongestion of PNP Lock-Up Cells DTD August 14, 2012 PDFjoriliejoyabNo ratings yet

- Indian Council Act, 1892Document18 pagesIndian Council Act, 1892Khan PurNo ratings yet

- DoPT Guidelines On Treatment - Regularization of Hospitalization - Quarantine Period During COVID 19 PandemicDocument2 pagesDoPT Guidelines On Treatment - Regularization of Hospitalization - Quarantine Period During COVID 19 PandemictapansNo ratings yet

- 7P's of Axis Bank - Final ReportDocument21 pages7P's of Axis Bank - Final ReportRajkumar RXzNo ratings yet

- Cfa Blank ContractDocument4 pagesCfa Blank Contractconcepcion riveraNo ratings yet

- ASME B16-48 - Edtn - 2005Document50 pagesASME B16-48 - Edtn - 2005eceavcmNo ratings yet

- 2014 Ukrainian Revolution PDFDocument37 pages2014 Ukrainian Revolution PDFjuanNo ratings yet

- LION OIL COMPANY v. NATIONAL UNION FIRE INSURANCE COMPANY OF PITTSBURGH, PA Et Al ComplaintDocument22 pagesLION OIL COMPANY v. NATIONAL UNION FIRE INSURANCE COMPANY OF PITTSBURGH, PA Et Al ComplaintACELitigationWatchNo ratings yet

- Fault (Culpa) : Accountability (121-123)Document4 pagesFault (Culpa) : Accountability (121-123)kevior2No ratings yet

- List of Books WrittenEdited by DR - Asghar Ali EngineerDocument2 pagesList of Books WrittenEdited by DR - Asghar Ali EngineerFarman AliNo ratings yet

- The Fundamental Duties of Citizens of IndiaDocument1 pageThe Fundamental Duties of Citizens of IndiaViplawNo ratings yet

- Module 4 Criminal Law 1Document7 pagesModule 4 Criminal Law 1Frans Raff LopezNo ratings yet

- 2 PNOC v. Court of Appeals, 457 SCRA 32Document37 pages2 PNOC v. Court of Appeals, 457 SCRA 32Aivy Christine ManigosNo ratings yet

- IPRA Case DigestDocument14 pagesIPRA Case DigestElden ClaireNo ratings yet

- Brokenshire College: Form C. Informed Consent Assessment FormDocument2 pagesBrokenshire College: Form C. Informed Consent Assessment Formgeng gengNo ratings yet

- Tcode GTSDocument28 pagesTcode GTSKishor BodaNo ratings yet

- 20 ObliconDocument3 pages20 ObliconQuiqui100% (2)

- Deloitte - Contingency PlanDocument5 pagesDeloitte - Contingency PlanvaleriosoldaniNo ratings yet

- Keeton AppealDocument3 pagesKeeton AppealJason SmathersNo ratings yet

- Language in India: Strength For Today and Bright Hope For TomorrowDocument24 pagesLanguage in India: Strength For Today and Bright Hope For TomorrownglindaNo ratings yet

- Lecture No. 06 - Types of Business Ethics Academic ScriptDocument8 pagesLecture No. 06 - Types of Business Ethics Academic ScriptShihab ChiyaNo ratings yet

- Program Registration Forms Sea-BasedDocument28 pagesProgram Registration Forms Sea-BasedCharina Marie CaduaNo ratings yet

- Background Check and Consent Form For Amazon IndiaDocument3 pagesBackground Check and Consent Form For Amazon Indiaanamika vermaNo ratings yet

- Ballard County, KY PVA: Parcel SummaryDocument3 pagesBallard County, KY PVA: Parcel SummaryMaureen WoodsNo ratings yet

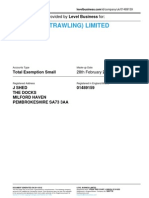

- RAWLINGS (TRAWLING) LIMITED - Company Accounts From Level BusinessDocument7 pagesRAWLINGS (TRAWLING) LIMITED - Company Accounts From Level BusinessLevel BusinessNo ratings yet

- The Analysis of Foreign PolicyDocument24 pagesThe Analysis of Foreign PolicyMikael Dominik AbadNo ratings yet

- KashmirDocument58 pagesKashmirMahamnoorNo ratings yet

- Week 13 - Local Government (Ra 7160) and DecentralizationDocument4 pagesWeek 13 - Local Government (Ra 7160) and DecentralizationElaina JoyNo ratings yet