You might also like

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Book 1Document13 pagesBook 1Sabab MunifNo ratings yet

- Af Cost Averaging WorksheetDocument150 pagesAf Cost Averaging WorksheetPanduNo ratings yet

- Bond Pricing and Yield SolutionDocument3 pagesBond Pricing and Yield SolutionC.E.O AnnieNo ratings yet

- Bond Pricing and Yield Solution: Strictly ConfidentialDocument3 pagesBond Pricing and Yield Solution: Strictly ConfidentialvusalaNo ratings yet

- Exploratory Factor AnalysisDocument2 pagesExploratory Factor AnalysisJose Achicahuala MamaniNo ratings yet

- Lab Report E.coliDocument9 pagesLab Report E.colihasanulfiqryNo ratings yet

- ROAD Cross SectonDocument12 pagesROAD Cross SectonBIRAJ THAPANo ratings yet

- Monserrat2D Activity6 AE9Document5 pagesMonserrat2D Activity6 AE9Jerome MonserratNo ratings yet

- Chapter 5Document66 pagesChapter 5ytsfrknNo ratings yet

- Persamaan HortonDocument4 pagesPersamaan HortonNaufal HafizNo ratings yet

- Astron PaperDocument9 pagesAstron PaperKamil RazaNo ratings yet

- Longkutoy, Sherina Tasya. Paralel (B)Document4 pagesLongkutoy, Sherina Tasya. Paralel (B)sherinaNo ratings yet

- Prob 0.05 Stock 1 Stock 2 Weights Mean Critical Value Mean 10 Mean 5 0 - 1.644854 SD 5 SD 2 SD Correlation - 0.3 1Document4 pagesProb 0.05 Stock 1 Stock 2 Weights Mean Critical Value Mean 10 Mean 5 0 - 1.644854 SD 5 SD 2 SD Correlation - 0.3 1Aditi BhiteNo ratings yet

- Fall 2015 EMBA Strategy Final Exam QuestionsDocument3 pagesFall 2015 EMBA Strategy Final Exam Questions03.wizenedwasterNo ratings yet

- WeibullplottingpaperDocument2 pagesWeibullplottingpapernunoNo ratings yet

- PropertiesDocument5 pagesPropertiesskumarsrNo ratings yet

- Account ExcelDocument5 pagesAccount ExcelDennis Korir0% (1)

- Significant Digits PracticeDocument1 pageSignificant Digits PracticemarleighNo ratings yet

- Sales (Yi) Income (Xi) : Model Unstandardized Coefficients Standardized Coefficients T Sig. Collinearity StatisticsDocument1 pageSales (Yi) Income (Xi) : Model Unstandardized Coefficients Standardized Coefficients T Sig. Collinearity StatisticsMaria SariNo ratings yet

- Polaroid 1996 CalculationDocument8 pagesPolaroid 1996 CalculationDev AnandNo ratings yet

- 3.2 FCFE Exercise PartDocument4 pages3.2 FCFE Exercise PartHTNo ratings yet

- Cailin Chen Question 9: (10 Points)Document5 pagesCailin Chen Question 9: (10 Points)Manuel BoahenNo ratings yet

- Business Valuation Model - Illustrative Case Study - All Approaches - BSA 3-1Document40 pagesBusiness Valuation Model - Illustrative Case Study - All Approaches - BSA 3-1Christen HerceNo ratings yet

- Hollow SquareDocument2 pagesHollow SquareDoreen PohNo ratings yet

- Risk Return ProblemsDocument5 pagesRisk Return ProblemsRanganathchowdaryNo ratings yet

- Creating A Story On Employee Data SheetDocument8 pagesCreating A Story On Employee Data SheetNgumbau MasilaNo ratings yet

- Case 1Document23 pagesCase 1Emad RashidNo ratings yet

- Week 5 - Tutorial SolutionsDocument5 pagesWeek 5 - Tutorial SolutionsDivya chandNo ratings yet

- Name Syed Faizan Ahmed Hashmi Erp Id 11891 Paper Variation BDocument57 pagesName Syed Faizan Ahmed Hashmi Erp Id 11891 Paper Variation BAhsen JunaidNo ratings yet

- HW5 Output AnalysisDocument5 pagesHW5 Output AnalysisMathabah OmerNo ratings yet

- Desarrollo Excell Examen Segundo Parcial de Estadistica 1 Cindy Martinez 20-0082Document7 pagesDesarrollo Excell Examen Segundo Parcial de Estadistica 1 Cindy Martinez 20-0082Cindy MartinezNo ratings yet

- Date Vertical Movement Date Horizontal Displacement Horizontal Load (N) Expansion SettlementDocument9 pagesDate Vertical Movement Date Horizontal Displacement Horizontal Load (N) Expansion SettlementRisyda UmmamiNo ratings yet

- Assessing Sustainability - Project Appraisal Via Cost Benefit AnalysisDocument12 pagesAssessing Sustainability - Project Appraisal Via Cost Benefit AnalysisTrần ThiNo ratings yet

- Libro 1Document4 pagesLibro 1KevinarturonsNo ratings yet

- Libro 1Document4 pagesLibro 1KevinarturonsNo ratings yet

- File To Detect Misalignment - k9 Santa Rosa II 3608Document33 pagesFile To Detect Misalignment - k9 Santa Rosa II 3608Jose RattiaNo ratings yet

- Errata ListDocument19 pagesErrata ListBabymetal LoNo ratings yet

- Proyek A: Kemungkinan I: Harga Produk Per Satuan Turun 10%Document6 pagesProyek A: Kemungkinan I: Harga Produk Per Satuan Turun 10%Anggriani ElfridaNo ratings yet

- Proyek A: Kemungkinan I: Harga Produk Per Satuan Turun 10%Document6 pagesProyek A: Kemungkinan I: Harga Produk Per Satuan Turun 10%Anggriani ElfridaNo ratings yet

- Un1105 Lec 5 - The Consumption DecisionDocument40 pagesUn1105 Lec 5 - The Consumption DecisionarilovesmusicNo ratings yet

- Chapter 6: Beta Estimation and The Cost of EquityDocument2 pagesChapter 6: Beta Estimation and The Cost of EquityMukul KadyanNo ratings yet

- Day 8-AssignmentDocument48 pagesDay 8-AssignmentSiddharthNo ratings yet

- Walt DisneyDocument40 pagesWalt DisneyRahil VermaNo ratings yet

- Chart TitleDocument5 pagesChart TitlenameNo ratings yet

- 5 - Extracted - EMB Series 50-Extracto PG - 119-153Document1 page5 - Extracted - EMB Series 50-Extracto PG - 119-153heinz billNo ratings yet

- Spot Rate CurveDocument15 pagesSpot Rate CurveEduardo FélixNo ratings yet

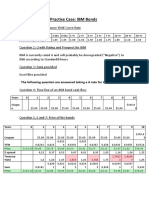

- Practise Case - IBM BondsDocument2 pagesPractise Case - IBM BondsJohnNo ratings yet

- Formulae and Discount Tables: Professional Level Examination Financial ManagementDocument2 pagesFormulae and Discount Tables: Professional Level Examination Financial ManagementClaudine CjNo ratings yet

- Problem 4-27 HW8 Page 1 Out of 4: Figure 1 CDF For The Standard Normal Random VariableDocument4 pagesProblem 4-27 HW8 Page 1 Out of 4: Figure 1 CDF For The Standard Normal Random VariableAlejandro ArvizuNo ratings yet

- Financial Ratios Analysis: BY: Rabia Qazi Chand ShabbirDocument27 pagesFinancial Ratios Analysis: BY: Rabia Qazi Chand ShabbirDuaNo ratings yet

- UNC UNF BSW BSF Screw Thread ChartDocument4 pagesUNC UNF BSW BSF Screw Thread ChartDave Slope100% (1)

- Table No.1 Particles Size Dia For Silt Factor: Site: BH - No.: Depth: 1.5 MTDocument1 pageTable No.1 Particles Size Dia For Silt Factor: Site: BH - No.: Depth: 1.5 MTvinoraamNo ratings yet

- Financial Management-1 Project ReportDocument6 pagesFinancial Management-1 Project ReportNakulesh VijayvargiyaNo ratings yet

- Case-2 Airline Profitability AnalysisDocument4 pagesCase-2 Airline Profitability AnalysisHaseeb Razzaq MinhasNo ratings yet

- Section B - C - Computer ApplicationDocument6 pagesSection B - C - Computer ApplicationMaas1No ratings yet

- US Bond Auction StatisticsDocument23 pagesUS Bond Auction StatisticschibondkingNo ratings yet

- 1 Review and Applications of Basic Mathematics: Exercise 1.1Document9 pages1 Review and Applications of Basic Mathematics: Exercise 1.1ivonneNo ratings yet

- Unit 6. Work and Kinetic EnergyDocument2 pagesUnit 6. Work and Kinetic EnergyRussel Jane BaccayNo ratings yet

- CH 34: International Financial ManagementDocument2 pagesCH 34: International Financial ManagementMukul KadyanNo ratings yet

- ECDIS Presentation Library 4Document16 pagesECDIS Presentation Library 4Orlando QuevedoNo ratings yet

- Transportation Engineering Unit I Part I CTLPDocument60 pagesTransportation Engineering Unit I Part I CTLPMadhu Ane NenuNo ratings yet

- CFA L1 Ethics Questions and AnswersDocument94 pagesCFA L1 Ethics Questions and AnswersMaulik PatelNo ratings yet

- Teacher Resource Disc: Betty Schrampfer Azar Stacy A. HagenDocument10 pagesTeacher Resource Disc: Betty Schrampfer Azar Stacy A. HagenRaveli pieceNo ratings yet

- WP05 - ACT 01 - Development 1909Document53 pagesWP05 - ACT 01 - Development 1909ramesh9966No ratings yet

- Windows Server 2016 Technical Preview NIC and Switch Embedded Teaming User GuideDocument61 pagesWindows Server 2016 Technical Preview NIC and Switch Embedded Teaming User GuidenetvistaNo ratings yet

- 1 s2.0 S0955221920305689 MainDocument19 pages1 s2.0 S0955221920305689 MainJoaoNo ratings yet

- Consumer PresentationDocument30 pagesConsumer PresentationShafiqur Rahman KhanNo ratings yet

- D-Dimer DZ179A Parameters On The Beckman AU680 Rev. ADocument1 pageD-Dimer DZ179A Parameters On The Beckman AU680 Rev. AAlberto MarcosNo ratings yet

- Grade 10 LP Thin LensDocument6 pagesGrade 10 LP Thin LensBrena PearlNo ratings yet

- Merchant Accounts Are Bank Accounts That Allow Your Business To Accept Card Payments From CustomersDocument43 pagesMerchant Accounts Are Bank Accounts That Allow Your Business To Accept Card Payments From CustomersRohit Kumar Baghel100% (1)

- FloodDocument9 pagesFloodapi-352767278No ratings yet

- The Division 2 - Guide To Highest Possible Weapon Damage PvE BuildDocument18 pagesThe Division 2 - Guide To Highest Possible Weapon Damage PvE BuildJjjjNo ratings yet

- Software Requirements SpecificationDocument9 pagesSoftware Requirements SpecificationSu-kEm Tech LabNo ratings yet

- Compressed Air Source BookDocument128 pagesCompressed Air Source Bookgfollert100% (1)

- Updated PDPDocument540 pagesUpdated PDPnikulaaaasNo ratings yet

- Muscular System Coloring Book: Now You Can Learn and Master The Muscular System With Ease While Having Fun - Pamphlet BooksDocument8 pagesMuscular System Coloring Book: Now You Can Learn and Master The Muscular System With Ease While Having Fun - Pamphlet BooksducareliNo ratings yet

- Local, Local Toll and Long Distance CallingDocument2 pagesLocal, Local Toll and Long Distance CallingRobert K Medina-LoughmanNo ratings yet

- Antonov 225 - The Largest - Airliner in The WorldDocument63 pagesAntonov 225 - The Largest - Airliner in The WorldFridayFunStuffNo ratings yet

- BDC Based Phase ControlDocument14 pagesBDC Based Phase ControlTiewsoh LikyntiNo ratings yet

- Yusuf Mahmood CVDocument3 pagesYusuf Mahmood CVapi-527941238No ratings yet

- Industrial Training ReportDocument19 pagesIndustrial Training ReportKapil Prajapati33% (3)

- Portfolio Sandwich Game Lesson PlanDocument2 pagesPortfolio Sandwich Game Lesson Planapi-252005239No ratings yet

- ALA - Assignment 3 2Document2 pagesALA - Assignment 3 2Ravi VedicNo ratings yet

- Anzsco SearchDocument6 pagesAnzsco SearchytytNo ratings yet

- 127 Bba-204Document3 pages127 Bba-204Ghanshyam SharmaNo ratings yet

- Lite Indicator Admin ManualDocument16 pagesLite Indicator Admin Manualprabakar070No ratings yet

- SrsDocument7 pagesSrsRahul Malhotra50% (2)

- Steinecker Boreas: Wort Stripping of The New GenerationDocument16 pagesSteinecker Boreas: Wort Stripping of The New GenerationAlejandro Javier Delgado AraujoNo ratings yet