You might also like

- BCG Sample Test - C - Key - UpdDocument1 pageBCG Sample Test - C - Key - Updсимона златковаNo ratings yet

- Course Notes Part IDocument61 pagesCourse Notes Part IWayne TanNo ratings yet

- Darden Case Book 2012Document195 pagesDarden Case Book 2012Rohith Girish100% (3)

- Basics of Probability in Philosophy ClassDocument11 pagesBasics of Probability in Philosophy Classharoon290No ratings yet

- Carrier (ULCC) Business Model in The U.S. Airline Industry. Retrieved FromDocument3 pagesCarrier (ULCC) Business Model in The U.S. Airline Industry. Retrieved Fromсимона златковаNo ratings yet

- 018FA620Document50 pages018FA620симона златковаNo ratings yet

- Zlatkova ExamDocument2 pagesZlatkova Examсимона златковаNo ratings yet

- Original PDFDocument20 pagesOriginal PDFjairamNo ratings yet

- Competing With DragonsDocument1 pageCompeting With Dragonsсимона златковаNo ratings yet

- Columbia Casebook 2006Document89 pagesColumbia Casebook 2006simplythecase100% (4)

- FM - Exercises Answers 2019Document15 pagesFM - Exercises Answers 2019симона златковаNo ratings yet

- Insuralpha activity matrix analysisDocument5 pagesInsuralpha activity matrix analysisсимона златкова100% (1)

- NYU Stern Casebook 2017Document198 pagesNYU Stern Casebook 2017Esojzerep100% (3)

- Answer Sheet PDFDocument1 pageAnswer Sheet PDFсимона златковаNo ratings yet

- Binaryresponsemf IMPDocument11 pagesBinaryresponsemf IMPсимона златковаNo ratings yet

- Predicted Probabilities and Marginal Effects After (Ordered) Logit/probit Using Margins in StataDocument13 pagesPredicted Probabilities and Marginal Effects After (Ordered) Logit/probit Using Margins in Statajuchama4256No ratings yet

- Economics 210 Handout # 6 The Probit, Logit, Tobit and Linear Probability ModelsDocument6 pagesEconomics 210 Handout # 6 The Probit, Logit, Tobit and Linear Probability Modelsсимона златковаNo ratings yet

- Presentation Script PDFDocument2 pagesPresentation Script PDFсимона златковаNo ratings yet

- ECO311 StataDocument111 pagesECO311 Stataсимона златкова100% (1)

- 231syllabus 21jan19Document3 pages231syllabus 21jan19симона златковаNo ratings yet

- Alan Thomlison's Analysis of William Blake's Life and Early WorksDocument8 pagesAlan Thomlison's Analysis of William Blake's Life and Early Worksсимона златковаNo ratings yet

- Class Exercise Simpleregression Ceo-SalaryDocument1 pageClass Exercise Simpleregression Ceo-Salaryсимона златковаNo ratings yet

- 2SLS MrozDocument2 pages2SLS Mrozсимона златковаNo ratings yet

- Pepsi CoDocument4 pagesPepsi Coсимона златковаNo ratings yet

- IV Regression: Notes and Key ConceptsDocument11 pagesIV Regression: Notes and Key Conceptsсимона златковаNo ratings yet

- 18.03.eco311 Hw1 3Document8 pages18.03.eco311 Hw1 3симона златковаNo ratings yet

- Oklahoma Gas Company To Explore Oil Wells in TexasDocument3 pagesOklahoma Gas Company To Explore Oil Wells in Texasсимона златковаNo ratings yet

- Midterm Output 2015 Eco311Document6 pagesMidterm Output 2015 Eco311симона златковаNo ratings yet

- 2SLS MrozDocument2 pages2SLS Mrozсимона златковаNo ratings yet

- Sargan and Durbin-WuDocument5 pagesSargan and Durbin-Wuсимона златковаNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- A Project Report On Direct TaxDocument52 pagesA Project Report On Direct Taxrani26oct72% (18)

- Tugas Latihan Chapter 10 Dan 11Document2 pagesTugas Latihan Chapter 10 Dan 11Arnalistan EkaNo ratings yet

- Payment of Bonus Act 1965Document11 pagesPayment of Bonus Act 1965KNOWLEDGE CREATORS100% (2)

- Soal Tugas Akm Is - ST o FP - CFDocument6 pagesSoal Tugas Akm Is - ST o FP - CFElyssa Fiqri Fauziah0% (1)

- How To Start MaltaDocument15 pagesHow To Start MaltaNicolae ChiriacNo ratings yet

- Annual Report and Accounts 2020Document382 pagesAnnual Report and Accounts 2020EvgeniyNo ratings yet

- Mj12e TB Ch13Document29 pagesMj12e TB Ch13George Edwards0% (1)

- Cambridge International AS & A Level: Accounting 9706/12Document12 pagesCambridge International AS & A Level: Accounting 9706/12Aimen AhmedNo ratings yet

- Radha Sridhar - 2 - 2019-2020Document2 pagesRadha Sridhar - 2 - 2019-2020Radha SridharNo ratings yet

- Business Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Document242 pagesBusiness Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Anurag JainNo ratings yet

- Courts (Antigua and Barbuda) Limited Tax Computation Year-End ReviewDocument377 pagesCourts (Antigua and Barbuda) Limited Tax Computation Year-End ReviewAries BautistaNo ratings yet

- Test Bank With Answers of Accounting Information System by Turner Chapter 12Document31 pagesTest Bank With Answers of Accounting Information System by Turner Chapter 12Ebook free100% (3)

- MosaerBaer PDFDocument167 pagesMosaerBaer PDFJupe JonesNo ratings yet

- Malta TINDocument4 pagesMalta TINMelvin ScorfnaNo ratings yet

- Financial ReportDocument14 pagesFinancial ReportJeannie GanNo ratings yet

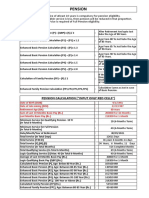

- Pension and Other Retirement BenifitsDocument8 pagesPension and Other Retirement BenifitsVikas GuptaNo ratings yet

- Latihan Soal Chapter 22Document9 pagesLatihan Soal Chapter 22JulyaniNo ratings yet

- Analyzing Financial RatiosDocument36 pagesAnalyzing Financial Ratiosanjo hosmerNo ratings yet

- Household Budget SummaryDocument6 pagesHousehold Budget SummaryBleep NewsNo ratings yet

- US Internal Revenue Service: n746Document4 pagesUS Internal Revenue Service: n746IRSNo ratings yet

- INCOME FROM LETTING OF REAL PROPERTY TAX RULINGDocument15 pagesINCOME FROM LETTING OF REAL PROPERTY TAX RULINGTengku Rizal Tengku Mat100% (1)

- Solutions To Chapter 9Document10 pagesSolutions To Chapter 9Luzz Landicho100% (1)

- Case Study - Management Control - Texas Instruments and Hewlett - PackardDocument20 pagesCase Study - Management Control - Texas Instruments and Hewlett - PackardJed Estanislao80% (10)

- Stracoma FinalssDocument53 pagesStracoma FinalssAeron Arroyo IINo ratings yet

- Capital Allowances: Zulkhairi@um - Edu. MyDocument35 pagesCapital Allowances: Zulkhairi@um - Edu. MyNero ShaNo ratings yet

- Raport Bayan Group 2018Document304 pagesRaport Bayan Group 2018Muhammad Abdul Rochim100% (1)

- Peacock Co Trial Balance Fire Loss ProblemDocument2 pagesPeacock Co Trial Balance Fire Loss ProblemmhikeedelantarNo ratings yet

- Presentation: Finance and Costing Topic: Types of Budgets & Types of AccountsDocument18 pagesPresentation: Finance and Costing Topic: Types of Budgets & Types of Accountsprasad shirodeNo ratings yet

- Finance Indus Motor 00Document15 pagesFinance Indus Motor 00laraib nadeemNo ratings yet

- Financial Report of Luminous EngineeringDocument85 pagesFinancial Report of Luminous EngineeringMazhar Arfin50% (4)