You might also like

- Research Paper On Indian InvestmentsDocument5 pagesResearch Paper On Indian Investmentssree24034354No ratings yet

- CHAPTER ONE KudziDocument7 pagesCHAPTER ONE KudziRodwellNo ratings yet

- Jul 30 Bbva Us Eco WatchDocument2 pagesJul 30 Bbva Us Eco WatchMiir ViirNo ratings yet

- Ifo Business Climate Index RisesDocument4 pagesIfo Business Climate Index RisesValter SilveiraNo ratings yet

- Covid 19 and Monetary Policy Speech by Michael SaundersDocument16 pagesCovid 19 and Monetary Policy Speech by Michael SaundersHao WangNo ratings yet

- Economic Highlights: Leading Index Eased in February, Pointing To A More Moderate Economic Growth in 2H 2010 - 23/04/2010Document2 pagesEconomic Highlights: Leading Index Eased in February, Pointing To A More Moderate Economic Growth in 2H 2010 - 23/04/2010Rhb InvestNo ratings yet

- Greenwood - Scharfstein - 2013 - The Growth of FinanceDocument26 pagesGreenwood - Scharfstein - 2013 - The Growth of FinanceBárbara AliagaNo ratings yet

- Lecture 4 Equities - 18.01.2023Document49 pagesLecture 4 Equities - 18.01.2023Saurabh PathakNo ratings yet

- CITATION HTT /L 1033Document55 pagesCITATION HTT /L 1033Miskatul ArafatNo ratings yet

- CL4 D Distributional Effects of Monetary Policy 2021Document47 pagesCL4 D Distributional Effects of Monetary Policy 2021Diana Calderon QuiquiaNo ratings yet

- IIF Argentina's Sudden StopDocument2 pagesIIF Argentina's Sudden StopCronista.comNo ratings yet

- Economic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Document2 pagesEconomic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Rhb InvestNo ratings yet

- BMN 506 - Week 3Document30 pagesBMN 506 - Week 3Shubham SrivastavaNo ratings yet

- Ku 2023 09 PM Geschaeftsklima enDocument4 pagesKu 2023 09 PM Geschaeftsklima enRafael BorgesNo ratings yet

- History of The Gaps ModelDocument9 pagesHistory of The Gaps ModelDarsa GopalakrishnanNo ratings yet

- Confidence As A Measure of Economic SuccessDocument1 pageConfidence As A Measure of Economic SuccessKathryn AshcroftNo ratings yet

- A Better Investment Climate and Foreign Direct Investment: Uri Dadush, Director, Development Prospects Group andDocument20 pagesA Better Investment Climate and Foreign Direct Investment: Uri Dadush, Director, Development Prospects Group andminhtuanngoNo ratings yet

- Trends in Foreign Direct Investment InflowsDocument7 pagesTrends in Foreign Direct Investment InflowsAnnamalai KarthickNo ratings yet

- Draft: Not For Quotation. Comments WelcomeDocument36 pagesDraft: Not For Quotation. Comments Welcomemichelle-aimee-e-puche-9108No ratings yet

- Mankiw8e Chap18Document31 pagesMankiw8e Chap18Sardar AftabNo ratings yet

- Aleman HaDocument4 pagesAleman Harborgesdossantos37No ratings yet

- Alas John Paul Facon Raul Augustus Macrobite1Document3 pagesAlas John Paul Facon Raul Augustus Macrobite1Raul Augustus D. FACONNo ratings yet

- Group of Seven: Meetings of G-7 Finance Ministers and Central Bank Governors February 5 6, 2010 Iqaluit, CanadaDocument21 pagesGroup of Seven: Meetings of G-7 Finance Ministers and Central Bank Governors February 5 6, 2010 Iqaluit, Canadarakesh s gNo ratings yet

- Ecuador: Where From, Where To: EconomicsDocument17 pagesEcuador: Where From, Where To: EconomicsIván GonzálezNo ratings yet

- Valuation - Final NotesDocument62 pagesValuation - Final NotesPooja GuptaNo ratings yet

- Reading Lesson 7Document5 pagesReading Lesson 7AnshumanNo ratings yet

- Chris Lynch: Chief Financial OfficerDocument17 pagesChris Lynch: Chief Financial OfficerHector Felix Gonzalez RamirezNo ratings yet

- 3.1 SwinnenDocument34 pages3.1 SwinnenPankaj DograNo ratings yet

- WTO Trade Statistics and Outlook October 2018Document6 pagesWTO Trade Statistics and Outlook October 2018Coleman NeeNo ratings yet

- Suominen Nordea 10012023Document4 pagesSuominen Nordea 10012023Wilhelm StjernvallNo ratings yet

- CM20 Topic 1 Revenue Recognition 2022 (BB Students)Document72 pagesCM20 Topic 1 Revenue Recognition 2022 (BB Students)victor.hamelleNo ratings yet

- The Private Sector Financial Balance As A Predictor of Financial CrisesDocument12 pagesThe Private Sector Financial Balance As A Predictor of Financial CrisesIsaac GoldNo ratings yet

- Economic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Document2 pagesEconomic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Rhb InvestNo ratings yet

- Economic Highlights :leading Index Slowed Down in April, Pointing To A More Moderate Economic Growth in 2H 2010-21/06/2010Document2 pagesEconomic Highlights :leading Index Slowed Down in April, Pointing To A More Moderate Economic Growth in 2H 2010-21/06/2010Rhb InvestNo ratings yet

- Chap14 Stabilization PolicyDocument38 pagesChap14 Stabilization PolicyKharisma ArtaNo ratings yet

- Stabilization PolicyDocument71 pagesStabilization PolicyJamalNo ratings yet

- Chap 18Document32 pagesChap 18Queen CatastropheNo ratings yet

- Economic Highlights - Business Conditions and Consumer Sentiment - 16/7/2010Document2 pagesEconomic Highlights - Business Conditions and Consumer Sentiment - 16/7/2010Rhb InvestNo ratings yet

- Fundamentals of Transfer Pricing & Associated EnterpriseDocument18 pagesFundamentals of Transfer Pricing & Associated Enterprisemaria felicianaNo ratings yet

- Chapter 5 - Macroeconomic Policy DebatesDocument37 pagesChapter 5 - Macroeconomic Policy DebatesbashatigabuNo ratings yet

- CHN Jun 10 RevDocument3 pagesCHN Jun 10 RevqtipxNo ratings yet

- For Student 15Document15 pagesFor Student 15sunil kumarNo ratings yet

- Travel - Tourism Pacific AllianceDocument20 pagesTravel - Tourism Pacific AllianceSebastian CriolloNo ratings yet

- Sudden Stops, Financial Crises, and Leverage: Financial Emerging Constraint Metry Shocks. The and Access Makes ObservedDocument34 pagesSudden Stops, Financial Crises, and Leverage: Financial Emerging Constraint Metry Shocks. The and Access Makes ObservedFernando FCNo ratings yet

- Esi 2019 05 enDocument21 pagesEsi 2019 05 enValter SilveiraNo ratings yet

- Lebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020Document17 pagesLebanon's Economy An Analysis and Some Recommendations: Esther Baroudy & Hady Farah 20 January 2020terryhadyNo ratings yet

- ECON F312: Money, Banking and Financial Markets I Semester 2020-21Document23 pagesECON F312: Money, Banking and Financial Markets I Semester 2020-21AKSHIT JAINNo ratings yet

- Economic Highlights: Leading Index Eased in January, Points To A More Moderate Economic Growth in 2H 2010 - 22/03/2010Document2 pagesEconomic Highlights: Leading Index Eased in January, Points To A More Moderate Economic Growth in 2H 2010 - 22/03/2010Rhb InvestNo ratings yet

- Fluidra Strategic Plan 2018Document101 pagesFluidra Strategic Plan 2018FluidraNo ratings yet

- Investing in EquityDocument45 pagesInvesting in Equitysuvarna27No ratings yet

- 1 - Introductions To EconomicsDocument37 pages1 - Introductions To EconomicsDy ANo ratings yet

- Press Release: WTO Lowers Trade Forecast As Tensions Unsettle Global EconomyDocument7 pagesPress Release: WTO Lowers Trade Forecast As Tensions Unsettle Global EconomyValter SilveiraNo ratings yet

- HDFC Bank Research Presentation April 2020Document41 pagesHDFC Bank Research Presentation April 2020MohitNo ratings yet

- Global Economic Prospects Jun2020 PressHighlights Chp4Document3 pagesGlobal Economic Prospects Jun2020 PressHighlights Chp4CristianMilciadesNo ratings yet

- Situation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesDocument34 pagesSituation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesuserabhishekNo ratings yet

- 06Document34 pages06anhnguyen.31231021095No ratings yet

- Mbafm18405dce 36 1709042135Document28 pagesMbafm18405dce 36 1709042135homedecor129No ratings yet

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Man Is A Werewolf To Man Capital and The PDFDocument20 pagesMan Is A Werewolf To Man Capital and The PDFNia FromeNo ratings yet

- 5660 65 3 PDFDocument20 pages5660 65 3 PDFdoguNo ratings yet

- The Big Bangs of IR The Myths That Your PDFDocument24 pagesThe Big Bangs of IR The Myths That Your PDFdoguNo ratings yet

- Jui 2018 60 121 133 PDFDocument14 pagesJui 2018 60 121 133 PDFdoguNo ratings yet

- Theories of Imperialism RevisitedDocument41 pagesTheories of Imperialism RevisiteddoguNo ratings yet

- Money As Money: Suzanne de Brunhoff's Marxist Monetary TheoryDocument22 pagesMoney As Money: Suzanne de Brunhoff's Marxist Monetary TheorydoguNo ratings yet

- 2016 How To Remedy Eurocentrism in IR T PDFDocument1 page2016 How To Remedy Eurocentrism in IR T PDFdoguNo ratings yet

- Notes On The Equivalence Between Ontology and Mathematics Burhanuddin BakiDocument10 pagesNotes On The Equivalence Between Ontology and Mathematics Burhanuddin BakidoguNo ratings yet

- 15 Wage Bargaining Under The New European Economic Governance EN Web VersionDocument419 pages15 Wage Bargaining Under The New European Economic Governance EN Web VersiondoguNo ratings yet

- dp14 21Document32 pagesdp14 21doguNo ratings yet

- 16+myant+et+al +Unemployment,+internal+devaluation+Web+version+finalDocument258 pages16+myant+et+al +Unemployment,+internal+devaluation+Web+version+finaldoguNo ratings yet

- 35 Percent EsDocument2 pages35 Percent EsdoguNo ratings yet

- Euroscepticism in Small Eu Member States Read in EnglishDocument160 pagesEuroscepticism in Small Eu Member States Read in EnglishdoguNo ratings yet

- The Road To Euro enDocument24 pagesThe Road To Euro endoguNo ratings yet

- Arab Spring Turkish Summer The Trajector PDFDocument14 pagesArab Spring Turkish Summer The Trajector PDFdoguNo ratings yet

- Resolution FoundationDocument40 pagesResolution FoundationdoguNo ratings yet

- White Paper On The Future of Europe en PDFDocument32 pagesWhite Paper On The Future of Europe en PDFȘerban AnghelNo ratings yet

- MUEGGE Financial Regulation in The European Union: A Research AgendaDocument16 pagesMUEGGE Financial Regulation in The European Union: A Research AgendadoguNo ratings yet

- How Neuroscience Can Inform EconomicsDocument57 pagesHow Neuroscience Can Inform EconomicsdoguNo ratings yet

- Online-Pub Eurozone FailureDocument71 pagesOnline-Pub Eurozone FailurePetros ArvanitisNo ratings yet

- 2016 Thinking Postcolonially About TheDocument8 pages2016 Thinking Postcolonially About ThedoguNo ratings yet

- Democracy Does Not Cause Growth The Importance of Endogeneity ArgumentsDocument64 pagesDemocracy Does Not Cause Growth The Importance of Endogeneity ArgumentsdoguNo ratings yet

- 2010 1 Zaf CrouchDocument22 pages2010 1 Zaf CrouchdoguNo ratings yet

- Achieving Operational Excellence and Customer Intimacy: Enterprise ApplicationsDocument2 pagesAchieving Operational Excellence and Customer Intimacy: Enterprise Applicationsranvirsingh76No ratings yet

- Key Account ManagementDocument34 pagesKey Account Managementmanin1804100% (1)

- h3453 Process Svcs SapDocument2 pagesh3453 Process Svcs SaprazekrNo ratings yet

- Catalogo AlconDocument27 pagesCatalogo Alconaku170% (1)

- The Commercial Dispatch Eedition 10-2-13Document20 pagesThe Commercial Dispatch Eedition 10-2-13The DispatchNo ratings yet

- Introduction To ERPDocument24 pagesIntroduction To ERPAbdul WahabNo ratings yet

- Lecture 5 - IAS 36 Impairment of AssetsDocument19 pagesLecture 5 - IAS 36 Impairment of AssetsJeff GanyoNo ratings yet

- Final Exam Review-VrettaDocument4 pagesFinal Exam Review-VrettaAna Cláudia de Souza0% (2)

- NotificatioN PSDocument6 pagesNotificatioN PSravi_mgd6No ratings yet

- Resources and Capabilities: Their Importance How To Analyse ThemDocument34 pagesResources and Capabilities: Their Importance How To Analyse Themvishal7debnat-402755No ratings yet

- Bca 201612Document78 pagesBca 201612tugayyoungNo ratings yet

- Mcdonald'S: Market StructureDocument5 pagesMcdonald'S: Market Structurepalak32No ratings yet

- 2670 La Tierra Street, Pasadena - SOLDDocument8 pages2670 La Tierra Street, Pasadena - SOLDJohn AlleNo ratings yet

- Custom Made Jeweler - Business PlanDocument39 pagesCustom Made Jeweler - Business Planfazins85% (13)

- Labstan and TerminationDocument10 pagesLabstan and TerminationMichael Ang SauzaNo ratings yet

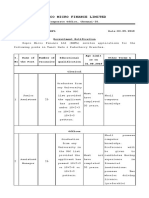

- Repco Micro Finance Limited: Corporate Office, Chennai-35Document4 pagesRepco Micro Finance Limited: Corporate Office, Chennai-35Abaraj IthanNo ratings yet

- Macroeconomic ProblemsDocument14 pagesMacroeconomic ProblemsRifat MahmudNo ratings yet

- Lopez Dee Vs SECDocument14 pagesLopez Dee Vs SECMark Ebenezer BernardoNo ratings yet

- Vistara JD For Groud Staff PDFDocument6 pagesVistara JD For Groud Staff PDFPrasad AcharyaNo ratings yet

- LABOR - Consolidated Distillers of The Far East Vs ZaragosaDocument3 pagesLABOR - Consolidated Distillers of The Far East Vs ZaragosaIshNo ratings yet

- CLOSING CASE Trade in TextilesDocument4 pagesCLOSING CASE Trade in TextilesHaseeb KhAn NiAziNo ratings yet

- Molson Brewing CompanyDocument16 pagesMolson Brewing CompanyVictoria ColakicNo ratings yet

- A Five Step Guide To Budget DevelopmentDocument15 pagesA Five Step Guide To Budget DevelopmentGhassanNo ratings yet

- Chapter 6-Asset ManagementDocument22 pagesChapter 6-Asset Managementchoijin987No ratings yet

- CSR of GoogleDocument28 pagesCSR of GooglePooja Sahani100% (1)

- List of Commercial Properties of Gurugram Zone For Auction Dated 06.08.2022Document5 pagesList of Commercial Properties of Gurugram Zone For Auction Dated 06.08.2022Yogesh MittalNo ratings yet

- Publishing and Sustaining ICT ProjectsDocument2 pagesPublishing and Sustaining ICT ProjectsMyra Dacquil Alingod100% (1)

- Ecco Strategic AnalysisDocument7 pagesEcco Strategic AnalysisLaishow Lai100% (3)

- Tender Evaluation Process NotesDocument18 pagesTender Evaluation Process NotesAlan McSweeney100% (5)

- IT Governance at INGDocument19 pagesIT Governance at INGChandan KhandelwalNo ratings yet