You might also like

- Methods for Applied Macroeconomic ResearchFrom EverandMethods for Applied Macroeconomic ResearchRating: 3.5 out of 5 stars3.5/5 (3)

- 1 s2.0 S1057521922002897 MainDocument23 pages1 s2.0 S1057521922002897 MainkiranjuwNo ratings yet

- Stock Returns, Quantile Autocorrelation, and Volatility ForecastingDocument50 pagesStock Returns, Quantile Autocorrelation, and Volatility ForecastingShaan Yeat Amin RatulNo ratings yet

- Macroeconomic Factors and Equity Prices: An Empirical Investigation by Using ARDL ApproachDocument18 pagesMacroeconomic Factors and Equity Prices: An Empirical Investigation by Using ARDL ApproachNasir JamalNo ratings yet

- Essay On Exchange Rates and in Ation: February 2020Document20 pagesEssay On Exchange Rates and in Ation: February 2020LaraibNo ratings yet

- A New Approach To Forecasting Exchange Rates: Ylan@biz - Uwa.edu - AuDocument24 pagesA New Approach To Forecasting Exchange Rates: Ylan@biz - Uwa.edu - AueeNo ratings yet

- Emerging Markets Review: Paresh Kumar Narayan, Susan Sunila Sharma, Dinh Hoang Bach Phan, Guangqiang Liu TDocument16 pagesEmerging Markets Review: Paresh Kumar Narayan, Susan Sunila Sharma, Dinh Hoang Bach Phan, Guangqiang Liu TDessy ParamitaNo ratings yet

- Research Article: Forecasting Stock Market Volatility: A Combination ApproachDocument9 pagesResearch Article: Forecasting Stock Market Volatility: A Combination ApproachShri Krishna BhatiNo ratings yet

- Forecasting Exchange Rate Volatility: The Superior Performance of Conditional Combinations of Time Series and Option Implied ForecastsDocument35 pagesForecasting Exchange Rate Volatility: The Superior Performance of Conditional Combinations of Time Series and Option Implied ForecastsramNo ratings yet

- In Which Exchange Rate Models Do Forecasters Trust?: David Hauner, Jaewoo Lee, and Hajime TakizawaDocument18 pagesIn Which Exchange Rate Models Do Forecasters Trust?: David Hauner, Jaewoo Lee, and Hajime TakizawadlavinutzzaNo ratings yet

- Gupta 2014Document12 pagesGupta 2014Alisson AndradeNo ratings yet

- Dynamic Estimation of Volatility Risk Premia and Investor Risk Aversion From Option-Implied and Realized VolatilitiesDocument38 pagesDynamic Estimation of Volatility Risk Premia and Investor Risk Aversion From Option-Implied and Realized VolatilitiesFrançois VoisardNo ratings yet

- International Journal of ForecastingDocument18 pagesInternational Journal of ForecastingKumar ManojNo ratings yet

- Forecasting Exchange Rates Using General Regression Neural NetworksDocument35 pagesForecasting Exchange Rates Using General Regression Neural NetworksAvikant BhardwajNo ratings yet

- Arbitrage Pricing Theory and Its Relevance in Modelling MarketDocument36 pagesArbitrage Pricing Theory and Its Relevance in Modelling MarketHamza AlmostafaNo ratings yet

- Forecasting Intraday Volatility and Value-At-Risk With High-Frequency Data 2013Document29 pagesForecasting Intraday Volatility and Value-At-Risk With High-Frequency Data 2013Tamás TornyiNo ratings yet

- 7366 14252 1 SMDocument19 pages7366 14252 1 SMMaria AlexandraNo ratings yet

- Using Volatility To Improve Momentum StrategiesDocument10 pagesUsing Volatility To Improve Momentum Strategiespderby1No ratings yet

- Macroeconomic Forces and Stock Prices:Evidence From The Bangladesh Stock MarketDocument55 pagesMacroeconomic Forces and Stock Prices:Evidence From The Bangladesh Stock MarketSayed Farrukh AhmedNo ratings yet

- Forecasting Daily and Monthly Exchange Rates With Machine Learning TechniquesDocument32 pagesForecasting Daily and Monthly Exchange Rates With Machine Learning TechniquesOsiayaNo ratings yet

- SSRN Id2609814Document37 pagesSSRN Id2609814if05041736No ratings yet

- Yield CurveDocument8 pagesYield Curveluli_kbreraNo ratings yet

- SSRN Id1957697Document21 pagesSSRN Id1957697pbustamantef98No ratings yet

- Money and Output Viewed Through A Rolling WindowDocument17 pagesMoney and Output Viewed Through A Rolling WindowpostscriptNo ratings yet

- Group Assignment CompletedDocument68 pagesGroup Assignment CompletedHengyi LimNo ratings yet

- Probability of Financial DistressDocument34 pagesProbability of Financial DistressFaye AlonzoNo ratings yet

- Exchange Rate Models Are Not As Bad As You Think: 8 J P A R CDocument61 pagesExchange Rate Models Are Not As Bad As You Think: 8 J P A R Cpmm1989No ratings yet

- Pacific-Basin Finance Journal: Zhifeng Dai, Huan Zhu TDocument18 pagesPacific-Basin Finance Journal: Zhifeng Dai, Huan Zhu TFTU.CS2 Trần Quang ĐiệpNo ratings yet

- JandooPaper PDFDocument23 pagesJandooPaper PDFPreethee GonpotNo ratings yet

- Journal of Economics and Management: Katarzyna NiewińskaDocument17 pagesJournal of Economics and Management: Katarzyna NiewińskaUmer ArifNo ratings yet

- 1 PDFDocument14 pages1 PDFAnum AhmedNo ratings yet

- Journal of Money and Finance 4Document27 pagesJournal of Money and Finance 4emilianocarpaNo ratings yet

- JIMF Yin Li PDFDocument19 pagesJIMF Yin Li PDFMutiara Hikma MahendradattaNo ratings yet

- Shaikh, A. S., Et Al (2017)Document25 pagesShaikh, A. S., Et Al (2017)Irza RayhanNo ratings yet

- Reaction Paper - Exchange Rates Forecasting Using Variable Length MA-NARXDocument1 pageReaction Paper - Exchange Rates Forecasting Using Variable Length MA-NARXJesa CamilanNo ratings yet

- Stock+market+returns+predictability ChaoDocument31 pagesStock+market+returns+predictability Chaoalexa_sherpyNo ratings yet

- Project Report On Forecasting of Crude Prices: Submitted To Prepared byDocument16 pagesProject Report On Forecasting of Crude Prices: Submitted To Prepared byKashyap BhattNo ratings yet

- 12 IV April 2024Document10 pages12 IV April 2024education and entertainment edutainmentNo ratings yet

- 5-Gorenc Veluscek QF 2016 Prediction of Stock Price Movement Based On Daily High PricesDocument35 pages5-Gorenc Veluscek QF 2016 Prediction of Stock Price Movement Based On Daily High PricesDiego ManzurNo ratings yet

- ECO412 Project - Forecasting Exchange Rates Through Machine Learning and Econometric ModelsDocument17 pagesECO412 Project - Forecasting Exchange Rates Through Machine Learning and Econometric ModelsShobhit SachanNo ratings yet

- Panopoulou Fama FrenchDocument25 pagesPanopoulou Fama FrenchPablo Aróstegui GarcíaNo ratings yet

- 10.1016/j.jempfin.2015.03.004: Journal of Empirical FinanceDocument60 pages10.1016/j.jempfin.2015.03.004: Journal of Empirical FinanceasoesNo ratings yet

- Artificial Neural Networks An Alternative To RegressionDocument30 pagesArtificial Neural Networks An Alternative To RegressionMubangaNo ratings yet

- P S M R C F: Redicting Tock Arket Eturns by Ombining OrecastsDocument30 pagesP S M R C F: Redicting Tock Arket Eturns by Ombining Orecastsmichaelguan326No ratings yet

- Tom Tat Luan An - Tieng AnhDocument24 pagesTom Tat Luan An - Tieng AnhThịnh Trần DuyNo ratings yet

- Rob Tall ManDocument15 pagesRob Tall ManrunawayyyNo ratings yet

- Applied-Modelling Exchange-Alayande, S. Ayinla - PH.DDocument8 pagesApplied-Modelling Exchange-Alayande, S. Ayinla - PH.DImpact JournalsNo ratings yet

- Relevant Cash Flows Journal - 1 TitleDocument6 pagesRelevant Cash Flows Journal - 1 TitleMonishaNo ratings yet

- 10 1080@1540496X 2020 1850440Document11 pages10 1080@1540496X 2020 1850440Irina AlexandraNo ratings yet

- Impact of Macroeconomic Variables On Stock Market: A Review of LiteratureDocument31 pagesImpact of Macroeconomic Variables On Stock Market: A Review of LiteratureBA20-042 DambaruNo ratings yet

- 1 s2.0 S1059056022000685 MainDocument16 pages1 s2.0 S1059056022000685 MainEngr. Naveed MazharNo ratings yet

- Reinvestigating Sources of Movements in Real Exchange RateDocument11 pagesReinvestigating Sources of Movements in Real Exchange RateAlexander DeckerNo ratings yet

- Satchell - Partial Moment MomentumDocument50 pagesSatchell - Partial Moment MomentumAyhanNo ratings yet

- Forecasting Volatility of Stock Indices With ARCH ModelDocument18 pagesForecasting Volatility of Stock Indices With ARCH Modelravi_nyseNo ratings yet

- Economic Modelling: Jamel JouiniDocument14 pagesEconomic Modelling: Jamel JouinihelenaNo ratings yet

- Inflation 34Document27 pagesInflation 34Snehal singhNo ratings yet

- Adaptive Market Hypothesis Evidence From Indian Bond MarketDocument14 pagesAdaptive Market Hypothesis Evidence From Indian Bond MarketsaravanakrisNo ratings yet

- An Empirical Testing of Capital Asset Pricing Model in BangladeshDocument10 pagesAn Empirical Testing of Capital Asset Pricing Model in BangladeshRdpthNo ratings yet

- Depreciation and Carrying AmountDocument12 pagesDepreciation and Carrying AmountNouman MujahidNo ratings yet

- Dividends: Factors Affecting Dividend PolicyDocument7 pagesDividends: Factors Affecting Dividend PolicyNouman MujahidNo ratings yet

- Assignment On DepreciationDocument4 pagesAssignment On DepreciationNouman MujahidNo ratings yet

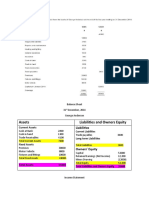

- Assets Liabilities and Owners EquityDocument9 pagesAssets Liabilities and Owners EquityNouman MujahidNo ratings yet

- Notes On Inventory ValuationDocument7 pagesNotes On Inventory ValuationNouman Mujahid100% (2)

- Breakeven Analysis: EBIT $0Document5 pagesBreakeven Analysis: EBIT $0Nouman MujahidNo ratings yet

- Notes On Working Capital ManagementDocument11 pagesNotes On Working Capital ManagementNouman MujahidNo ratings yet

- Merger: Acquiring CompanyDocument3 pagesMerger: Acquiring CompanyNouman MujahidNo ratings yet

- Quiz of DividendDocument1 pageQuiz of DividendNouman Mujahid0% (1)

- Ebit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCDocument6 pagesEbit EBIT Q P-FC-VC Q: Find EBIT Price Quantity Sales - Fixed Cost - VC Per Unit Quantity TVCNouman MujahidNo ratings yet

- Finance Interview Questions: Carey CompassDocument2 pagesFinance Interview Questions: Carey CompassNouman MujahidNo ratings yet

- Initial Cash FlowDocument3 pagesInitial Cash FlowNouman Mujahid50% (2)

- Averageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Document1 pageAverageinvestment Under Proposed /actual Plan (Total Variable Cost) / (Turnover of Accounts Receivable)Nouman MujahidNo ratings yet

- Accounts Payable ManagementDocument3 pagesAccounts Payable ManagementNouman MujahidNo ratings yet

- Beta Levered and UnleveredDocument3 pagesBeta Levered and UnleveredNouman MujahidNo ratings yet

- What Is Behavioral FinanceDocument4 pagesWhat Is Behavioral FinanceNouman MujahidNo ratings yet

- Bahvioral FinanceDocument14 pagesBahvioral FinanceNouman MujahidNo ratings yet

- Madina Medical StoreDocument29 pagesMadina Medical StoreNouman MujahidNo ratings yet

- Cross - Iyears Companbs BI Dualitman - O Roa ROE SizeDocument8 pagesCross - Iyears Companbs BI Dualitman - O Roa ROE SizeNouman MujahidNo ratings yet

- How To Write Effective Introduction of An ArticleDocument14 pagesHow To Write Effective Introduction of An ArticleNouman MujahidNo ratings yet

- Corporate Performance and Stakeholder Management: Balancing Shareholder and Customer Interests in The U.K. Privatized Water IndustryDocument14 pagesCorporate Performance and Stakeholder Management: Balancing Shareholder and Customer Interests in The U.K. Privatized Water IndustryNouman MujahidNo ratings yet

- Bundling Human Capital With Organizational Context: The Impact of International Assignment Experience On Multinational Firm Performance and Ceo PayDocument20 pagesBundling Human Capital With Organizational Context: The Impact of International Assignment Experience On Multinational Firm Performance and Ceo PayNouman MujahidNo ratings yet

- Arbitrage Pricing TheoryDocument5 pagesArbitrage Pricing TheoryNouman MujahidNo ratings yet

- Org 4Document34 pagesOrg 4Nouman MujahidNo ratings yet

- TESDA Online Program - Managing Your Personal FinancesDocument14 pagesTESDA Online Program - Managing Your Personal FinancesDinah Faye Redulla100% (3)

- LatinFocus Consensus Forecast - August 2019Document8 pagesLatinFocus Consensus Forecast - August 2019UyPress NoticiasNo ratings yet

- FIN 4604 Sample Questions IDocument20 pagesFIN 4604 Sample Questions IReham HegazyNo ratings yet

- Chapter 3 - Money Supply and Money DemandDocument37 pagesChapter 3 - Money Supply and Money DemandJamalNo ratings yet

- International Business Environment PDFDocument298 pagesInternational Business Environment PDFHarmeet AnandNo ratings yet

- Why Inflation Matters ?: Rohit ChauhanDocument9 pagesWhy Inflation Matters ?: Rohit ChauhanhamsNo ratings yet

- Intermediate Macroeconomics: Lecture 11: The Dynamic AS-AD Model, Part OneDocument28 pagesIntermediate Macroeconomics: Lecture 11: The Dynamic AS-AD Model, Part OneAlexRussellNo ratings yet

- Part I. Multiple Choice Questions. Circle The Best AnswersDocument4 pagesPart I. Multiple Choice Questions. Circle The Best AnswersgivemeNo ratings yet

- Outrageous Predictions 2021Document26 pagesOutrageous Predictions 2021Zerohedge100% (3)

- WSJ 2808Document30 pagesWSJ 2808NOROKNo ratings yet

- Economy of PakistanDocument31 pagesEconomy of PakistanMoater ImranNo ratings yet

- Swedish Financial SystemDocument5 pagesSwedish Financial Systemashu1403No ratings yet

- Presentation On State Bank of PakistanDocument61 pagesPresentation On State Bank of PakistanMuhammad WasifNo ratings yet

- Quiz Study Unit 9 PDFDocument2 pagesQuiz Study Unit 9 PDFVinny HungweNo ratings yet

- BA CORE 2. Venezuela Under Hugo Chávez and BeyondDocument4 pagesBA CORE 2. Venezuela Under Hugo Chávez and BeyondRiah Trisha Gabini Gapuzan IINo ratings yet

- Ar EdfhcfDocument45 pagesAr EdfhcfPrasen RajNo ratings yet

- Tutorial Letter 201/2/2017: Economics 1BDocument19 pagesTutorial Letter 201/2/2017: Economics 1BKefiloe MoatsheNo ratings yet

- Impact of Inflation On Households' Purchasing Power With Reference To Coimbatore City Mrs.R.Judith PriyaDocument13 pagesImpact of Inflation On Households' Purchasing Power With Reference To Coimbatore City Mrs.R.Judith PriyaTharchineeNo ratings yet

- EFFECT OF FISCAL POLICY STOCK MARKET PERFORMANCE (2) LatestDocument40 pagesEFFECT OF FISCAL POLICY STOCK MARKET PERFORMANCE (2) LatestMajorNo ratings yet

- Strategic Management Question-AnswersDocument97 pagesStrategic Management Question-AnswersRamalingam Chandrasekharan89% (100)

- New FI Datastream Datatypes Release 7Document3 pagesNew FI Datastream Datatypes Release 7abandegenialNo ratings yet

- 5 Q Mar 2016 P1S2Document12 pages5 Q Mar 2016 P1S2chittran313No ratings yet

- Scheme of Work Ads504 - October 2022 - February 2023 (All)Document16 pagesScheme of Work Ads504 - October 2022 - February 2023 (All)Leonard DavinsonNo ratings yet

- Spiro Spathis Marketing StrategyDocument16 pagesSpiro Spathis Marketing StrategyRawan Tamer100% (3)

- Chapter 9 Solution Manual MacroDocument5 pagesChapter 9 Solution Manual MacroMega Pop LockerNo ratings yet

- 2012 Budget PublicationDocument71 pages2012 Budget PublicationPushpa PatilNo ratings yet

- P2 Chapter 1Document0 pagesP2 Chapter 1immaculate79No ratings yet

- Socio-Economic Challenges in Pakistan: Mrs. Fahmida Aslam, Mr. Jamshed Ali BalochDocument12 pagesSocio-Economic Challenges in Pakistan: Mrs. Fahmida Aslam, Mr. Jamshed Ali BalochMuhammad AsadNo ratings yet

- The World Bank's Classification of Countries by IncomeDocument52 pagesThe World Bank's Classification of Countries by IncomePradip KadelNo ratings yet

- Eco Final ProjectDocument20 pagesEco Final ProjectvedangmishraNo ratings yet