You might also like

- BI - Fin ForecastDocument13 pagesBI - Fin Forecastdiksha_motwaniNo ratings yet

- International Banking & Finance CaseDocument7 pagesInternational Banking & Finance Casediksha_motwaniNo ratings yet

- BI - Fin ForecastDocument13 pagesBI - Fin Forecastdiksha_motwaniNo ratings yet

- Group 4 - Investment BankingDocument62 pagesGroup 4 - Investment Bankingdiksha_motwaniNo ratings yet

- Group 1Document9 pagesGroup 1diksha_motwaniNo ratings yet

- Letter of CreditDocument8 pagesLetter of Creditdiksha_motwaniNo ratings yet

- Security Documentation FinalDocument37 pagesSecurity Documentation Finaldiksha_motwaniNo ratings yet

- The Indian Contract Act 1872Document122 pagesThe Indian Contract Act 1872Ramakrishna ReddyNo ratings yet

- InvestmentsDocument58 pagesInvestmentsdiksha_motwaniNo ratings yet

- Ypothecation OF Ovable Achinery Letter OF Credit Packing CreditDocument38 pagesYpothecation OF Ovable Achinery Letter OF Credit Packing Creditdiksha_motwaniNo ratings yet

- Creditratingagencycrappt 130306035605 Phpapp02Document17 pagesCreditratingagencycrappt 130306035605 Phpapp02diksha_motwaniNo ratings yet

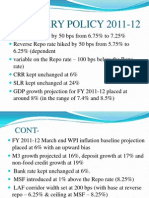

- RBI - Monetary PolicyDocument14 pagesRBI - Monetary Policydiksha_motwaniNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Katehi Grievance LetterDocument12 pagesKatehi Grievance LetterSacramento BeeNo ratings yet

- Tort of NegligenceDocument2 pagesTort of NegligenceYANZHUNo ratings yet

- Ecdis-24 01Document4 pagesEcdis-24 01Leandro PintoNo ratings yet

- Language and Linguistics Solved MCQs (Set-1)Document6 pagesLanguage and Linguistics Solved MCQs (Set-1)Rai Zia Ur RahmanNo ratings yet

- Education and Socialisim or Socialist Order in IndiaDocument30 pagesEducation and Socialisim or Socialist Order in IndiaAman RajoraNo ratings yet

- Resilient Modulus of Hot-Mix Asphalt Gap Graded With Waste Rubber Tire AdditivesDocument10 pagesResilient Modulus of Hot-Mix Asphalt Gap Graded With Waste Rubber Tire Additivesdanang abdilahNo ratings yet

- Theri GathaDocument26 pagesTheri GathaLalit MishraNo ratings yet

- RR 1116Document72 pagesRR 1116Кирилл КрыловNo ratings yet

- Buggy LabDocument5 pagesBuggy Labnarinyigit84No ratings yet

- The Essence of Man enDocument170 pagesThe Essence of Man enralforoniNo ratings yet

- Progress Test 01Document6 pagesProgress Test 01lethuha1988100% (2)

- Nervous System Regulating Activities by UnyteDocument14 pagesNervous System Regulating Activities by UnytehellozenbokNo ratings yet

- DCF Calculation of Dabur India Ltd.Document6 pagesDCF Calculation of Dabur India Ltd.Radhika ChaudhryNo ratings yet

- 21st Century Managerial and Leadership SkillsDocument19 pages21st Century Managerial and Leadership SkillsRichardRaqueno80% (5)

- Ed 2 Module 8 1Document5 pagesEd 2 Module 8 1Jimeniah Ignacio RoyoNo ratings yet

- Computation of The Compression Factor and Fugacity Coefficient of Real GasesDocument20 pagesComputation of The Compression Factor and Fugacity Coefficient of Real Gaseshamza A.laftaNo ratings yet

- Sagittarius The HeroDocument2 pagesSagittarius The HeroСтеди Транслейшънс0% (1)

- Principal Parts of Greek Verbs Appearing in James SwetnamDocument8 pagesPrincipal Parts of Greek Verbs Appearing in James Swetnammausj100% (1)

- Orgl 4361 Capstone 2 Artifact ResearchDocument12 pagesOrgl 4361 Capstone 2 Artifact Researchapi-531401638No ratings yet

- Why Teach Problem SolvingDocument4 pagesWhy Teach Problem SolvingShiela E. EladNo ratings yet

- 2018 - 14 Sept - Matlit Hymns - Exaltation Holy CrossDocument16 pages2018 - 14 Sept - Matlit Hymns - Exaltation Holy CrossMarguerite PaizisNo ratings yet

- The Law of Attraction Work For YouDocument7 pagesThe Law of Attraction Work For YouBambang PrasetyoNo ratings yet

- Introduction To Production SeparatorsDocument37 pagesIntroduction To Production Separatorsjps21No ratings yet

- The Importance of Instructional MaterialDocument3 pagesThe Importance of Instructional MaterialJheramae SegoviaNo ratings yet

- Cacao - Description, Cultivation, Pests, & Diseases - BritannicaDocument8 pagesCacao - Description, Cultivation, Pests, & Diseases - Britannicapincer-pincerNo ratings yet

- People Vs AbellaDocument32 pagesPeople Vs AbellaKanraMendozaNo ratings yet

- GRADE 8 3rd Quarter ReviewerDocument9 pagesGRADE 8 3rd Quarter ReviewerGracella BurladoNo ratings yet

- Detailed Lesson Plan in English I. ObjectivesDocument3 pagesDetailed Lesson Plan in English I. ObjectivesJenefer Tunares100% (1)

- 11.1. Complete The Sentences. Use One of These Verbs in The Past SimpleDocument4 pages11.1. Complete The Sentences. Use One of These Verbs in The Past SimpleSebastián Valencia Moreno0% (1)